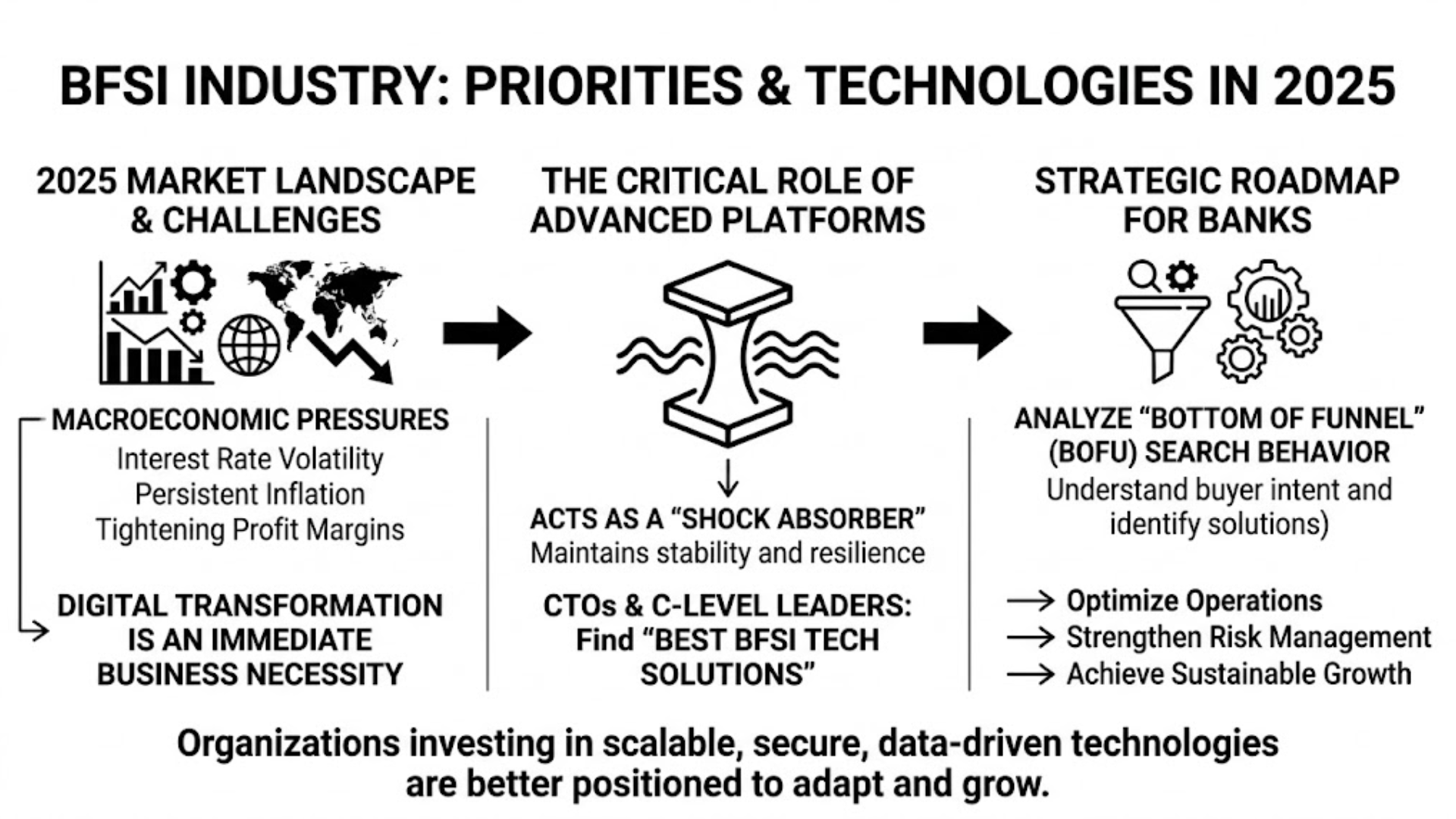

The global Banking, Financial Services, and Insurance (BFSI) industry is entering a defining transformation phase in 2025. Macroeconomic pressures, including interest rate volatility, persistent inflation, and tightening profit margins, are pushing financial institutions to rethink their technology architecture and operating models. As a result, digital transformation has shifted from a long-term initiative to an immediate business necessity.

Today, advanced platforms act as a critical “shock absorber” for the financial system, helping banks maintain stability and resilience amid market disruptions. For this reason, identifying the best BFSI tech solutions for banks 2025 has become a top priority for Chief Technology Officers (CTOs) and C-level leaders. Organizations that invest in scalable, secure, and data-driven technologies are better positioned to adapt, compete, and grow in an increasingly complex environment.

In addition, the report analyzes Bottom of Funnel (BoFU) search behavior among B2B decision-makers, offering valuable context on how buyers identify the best BFSI tech solutions for banks 2025. By combining market intelligence with strategic analysis, this study provides a clear roadmap for banks aiming to optimize operations, strengthen risk management, and achieve sustainable growth.

Macroeconomic Pressures and the Shift Toward the Best BFSI Tech Solutions for Banks 2025

Before exploring technology trends, it is essential to understand the broader economic context shaping the BFSI sector in 2025. Ongoing margin pressure, driven by inflation and interest rate fluctuations, is accelerating the need for automation and cost optimization. Recent industry data highlights this challenge. For example, Chinese banks reported modest gross loan growth of only 7–9% among top institutions, while Net Interest Margins (NIM) remained inconsistent, limiting overall profitability.

At the same time, asset quality risks are rising across key segments such as retail lending, inclusive finance, and property-related corporate portfolios. These pressures make it clear that traditional growth models based on physical expansion are no longer sustainable. Instead, banks are turning to digital platforms and intelligent systems to improve efficiency and remain competitive. This is why investing in the best BFSI tech solutions for banks 2025 is becoming a strategic necessity rather than an option.

Changing Marketing Strategies and Customer Expectations

The shift is also visible in how BFSI organizations approach marketing and customer engagement. Instead of relying on traditional channels, brands are rapidly adopting digital-first strategies.

Key trends include:

- A 16% decline in TV advertising volumes in major markets like India

- A fivefold increase in digital advertising investment

- A transition from mass “reach-buying” to performance-driven, multi-platform campaigns

Although TV still plays a role in sectors such as life insurance and mortgage loans, customer expectations have evolved. Today’s users demand seamless and highly personalized experiences. These expectations are increasingly met through neobanks and embedded finance platforms.

To stay competitive, financial institutions must continuously evaluate and adopt the best BFSI tech solutions for banks 2025, ensuring they can deliver personalized, data-driven services at scale.

IT Budget Constraints and the Need for Strategic Reallocation

Despite the urgency of innovation, many banks face structural challenges in their IT spending. A large portion of budgets is still allocated to maintaining legacy systems rather than driving transformation.

Common issues include:

- Up to 78% of IT budgets spent on “run-the-bank” activities

- Limited investment in “change-the-bank” initiatives

- Slow innovation cycles due to outdated infrastructure

To address these challenges, banking leaders should focus on:

- Simplifying operational processes and reducing system complexity

- Reallocating budgets toward innovation and digital transformation

- Strengthening data management and analytics capabilities

Ultimately, prioritizing scalable and future-ready platforms, recognized as the best BFSI tech solutions for banks 2025—will help banks optimize costs, improve agility, and achieve sustainable growth in an increasingly competitive landscape.

Artificial Intelligence (AI) and Automation: A Core Pillar of the Best BFSI Tech Solutions for Banks 2025

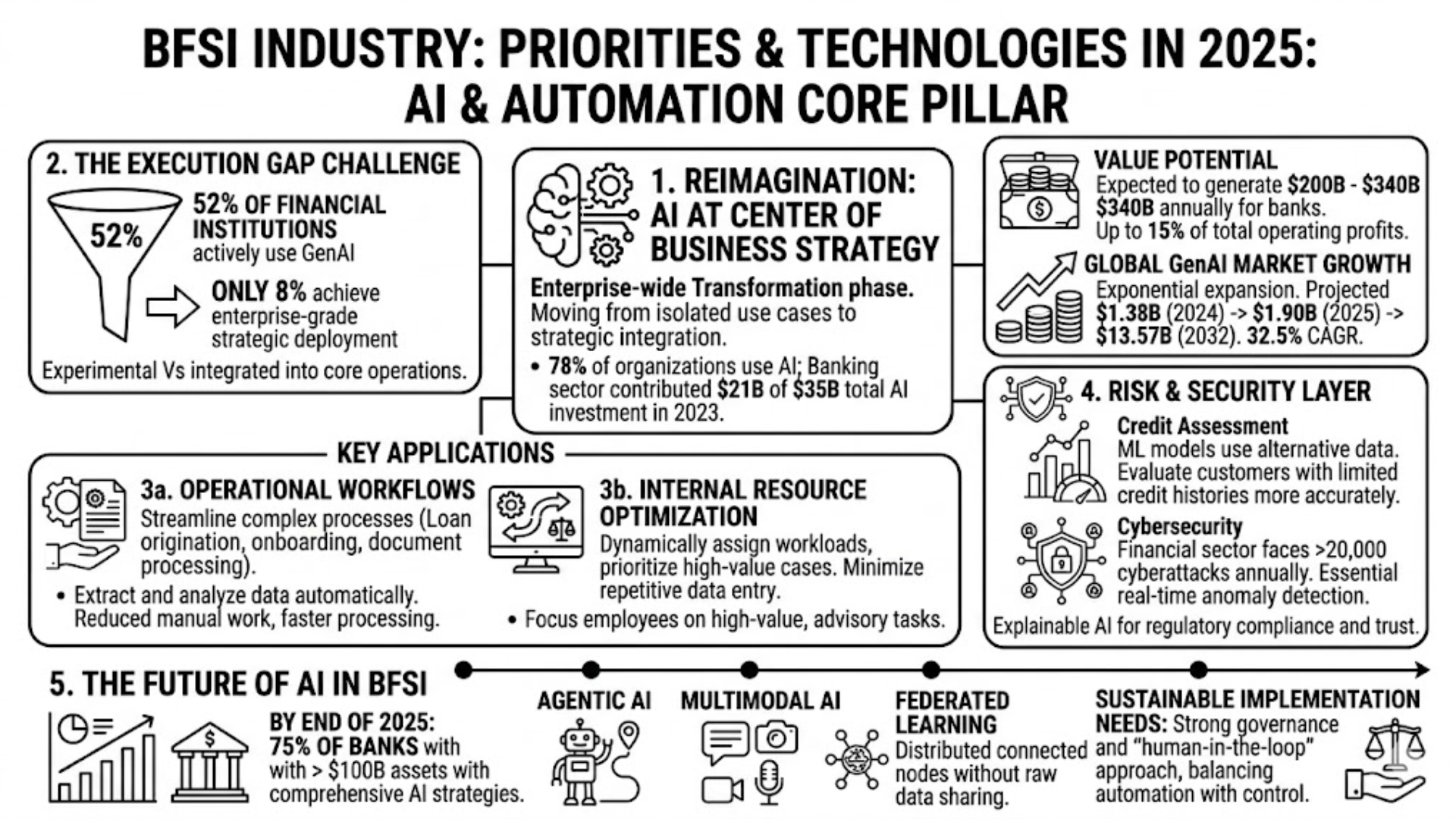

Artificial Intelligence (AI) is no longer an experimental layer in the BFSI sector. In 2025, it marks a structural turning point where banks shift from isolated use cases—such as basic chatbots or simple dashboards—toward enterprise-wide transformation. This new phase, often described as “Reimagination,” positions AI at the center of business strategy.

Adoption rates reflect this shift. Today, 78% of organizations use AI in at least one business function, while the banking sector alone contributed roughly $21 billion of the $35 billion invested in AI across financial services in 2023. More importantly, the value potential is massive. Generative AI (GenAI) is expected to generate between $200 billion and $340 billion annually for banks, accounting for up to 15% of total operating profits.

As a result, AI capabilities are becoming a defining factor when evaluating the best BFSI tech solutions for banks 2025, especially for institutions aiming to scale efficiently and compete on data-driven intelligence.

Rapid Growth with a Persistent Strategy

The global GenAI market in BFSI is expanding at an exponential pace. From a valuation of $1.38 billion in 2024, it is projected to reach $1.90 billion in 2025 and grow at a CAGR of 32.5% to $13.57 billion by 2032.

However, growth alone does not guarantee success. A clear execution gap is emerging:

- 52% of financial institutions report active use of GenAI

- Only 8% have achieved enterprise-grade, strategic deployment

This gap highlights a critical challenge. While many banks are experimenting with AI, only a small percentage are successfully integrating it into core operations. Bridging this divide is essential for organizations seeking to fully leverage the best BFSI tech solutions for banks 2025.

Key AI Applications Transforming BFSI Operations

AI development in 2025 is converging around high-impact, business-critical functions rather than generic automation.

In operational workflows, banks are deploying specialized AI models to streamline complex processes such as loan origination, customer onboarding, and document processing. These systems can extract and analyze data from financial documents, like tax returns or balance sheets and automatically populate borrower profiles. As a result, manual work is reduced, processing time is shortened, and accuracy improves significantly.

At the same time, AI is optimizing internal resource allocation. Intelligent systems can dynamically assign workloads, prioritize high-value cases, and reduce bottlenecks in underwriting processes. Tools like generative AI advisors further minimize repetitive data entry, allowing employees to focus on higher-value, advisory-driven tasks.

AI as a Strategic Layer for Risk and Security

Beyond efficiency, AI is becoming a critical component of risk management and security. In credit assessment, machine learning models outperform traditional scoring systems by analyzing alternative data sources, enabling banks to evaluate customers with limited credit histories more accurately.

In parallel, cybersecurity has become a top priority. With the financial sector experiencing over 20,000 cyberattacks in a single year, AI-powered systems are now essential for real-time anomaly detection and rapid incident response. Transparency is also gaining importance, driving the adoption of Explainable AI to meet regulatory requirements and build trust with stakeholders.

The Future of AI in BFSI: From Tools to Autonomous Systems

Looking ahead, AI adoption will deepen rapidly. By the end of 2025, an estimated 75% of banks with assets exceeding $100 billion are expected to implement comprehensive AI strategies.

Emerging technologies will define the next phase of innovation, including:

- Agentic AI capable of autonomously executing multi-step processes

- Multimodal AI that integrates text, image, and voice data

- Federated Learning, enabling secure collaboration without sharing raw data

Despite these advancements, successful implementation will depend on strong governance frameworks and a “human-in-the-loop” approach. Banks must balance automation with control, ensuring that AI-driven decisions remain transparent, ethical, and aligned with regulatory standards.

Total Cost of Ownership (TCO) Analysis: Choosing the Right Model for the Best BFSI Tech Solutions for Banks 2025

When evaluating the best BFSI tech solutions for banks 2025, one of the most critical decisions is the deployment model: Cloud, On-Premise, or Hybrid. This choice directly impacts cost efficiency, scalability, and long-term operational flexibility.

The market clearly shows a strong shift toward cloud adoption. The cloud core banking platform market is expected to reach $1.6 billion in 2025 and grow to $11.1 billion by 2035, reflecting a CAGR of 21.4%. In parallel, Gartner predicts that 90% of banking workloads will be hosted on the cloud by 2030. These numbers highlight the growing dominance of cloud infrastructure in modern banking ecosystems.

The Reality Behind Cloud Adoption: Efficiency vs. Waste

Despite its rapid growth, cloud adoption is no longer approached with blind optimism. In 2025, IT leaders are taking a more cautious and strategic view. A key concern is cost inefficiency, with approximately 21% of enterprise cloud spending, equivalent to $44.5 billion, being wasted due to poor resource management and underutilization.

This has triggered a notable “cloud repatriation” trend, where organizations move certain workloads back to On-Premise environments. This shift is particularly relevant for systems requiring:

- Ultra-low latency (e.g., real-time fraud detection)

- Strict data governance and compliance

- Stable, predictable workloads running continuously

As a result, deployment decisions are no longer based on trends but on detailed TCO analysis aligned with business needs.

5-Year TCO Comparison: Cloud vs. On-Premise

A deeper Total Cost of Ownership (TCO) analysis reveals significant differences between the two models, especially for AI-intensive workloads using GPU-powered infrastructure.

On-Premise Infrastructure requires high upfront investment (CAPEX), including servers, data center operations, power, and cooling. Over a 5-year period, total costs may reach approximately $411,000. However, this model becomes highly cost-efficient when systems operate continuously at near 100% utilization. For mission-critical workloads, such as core banking ledgers or real-time analytics, On-Premise offers superior long-term value by eliminating recurring usage fees.

Cloud Infrastructure, on the other hand, follows a pay-as-you-go model. While this provides flexibility, costs can escalate significantly under constant usage. In a scenario with 100% utilization over five years, total expenses can reach up to $854,000 more than double the On-Premise model.

However, the key advantage of cloud lies in elasticity. When workloads fluctuate and average around 30% utilization, costs decrease substantially. In such cases, annual spending may drop to approximately $109,000, making cloud a far more efficient option. Additional pricing models, such as reserved instances or spot pricing, can further optimize costs.

Why Hybrid Cloud Is Becoming the Standard

This contrast in cost structures explains the rapid adoption of Hybrid and Multi-Cloud strategies. By 2026, around 75% of banks are expected to operate in hybrid environments.

In practice, this means:

- Core systems and sensitive data remain On-Premise for control, security, and cost efficiency

- Customer-facing applications, APIs, and AI experimentation are deployed on the cloud for scalability and speed

This balanced approach allows financial institutions to optimize both performance and cost while maintaining flexibility. Ultimately, organizations that align their infrastructure strategy with workload characteristics will be better positioned to identify and implement the best BFSI tech solutions for banks 2025.

Explore how SmartDev partners with BFSI teams through a focused AI sprint to validate use cases, align stakeholders, and define a clear path forward before AI development begins.

SmartDev helps BFSI organizations clarify AI use cases and assess feasibility, enabling confident decisions and reducing risks before committing to AI development.

Learn how SmartDev accelerates AI initiatives, ensuring rapid deployment and reduced time to market.

Strengthen Your BFSI Security Testing with UsCore Banking Modernization Era: Vendor Comparison 2025

Changing user behaviors and the rise of Neobanks backed by modern technology have forced traditional institutions to rethink their aging core architectures. The global core banking software market is experiencing unprecedented growth: from a valuation of $16.79 billion in 2024, it is expected to skyrocket to $64.96 billion by 2032 (CAGR 18.6%). Notably, over 950 banks worldwide are leveraging AI-driven and cloud-native core solutions.

The overall banking and financial services application market (including core, investment management, lending, and risk management) also saw a 9.8% YoY expansion to reach $42.9 billion in 2024, and is projected to hit $55.9 billion by 2029. The top 10 largest vendors, led by Microsoft, FIS Global, SAP, and Oracle, account for 41.1% of the entire market share.

Leading Core Banking Market Share and Revenue Analysis (2024 – Early 2025)

The table below summarizes the financial positions and growth of the giants dominating the core BFSI tech market :

| Software Vendor | 2024 Revenue (Billion USD) | YoY Growth (%) | Estimated Market Share (%) |

| FIS Global | 15.40 | 4.1% | 22.8% |

| Oracle Financial Services | 7.80 | 8.3% | 11.5% |

| Fiserv | 7.40 | 4.2% | 10.7% |

| IBM Banking | 4.80 | -2.0% | 8.3% |

| Infosys Finacle | 1.94 | 9.0% | 7.8% |

| SAP Banking | 1.90 | 4.4% | 6.2% |

| Finastra | 1.70 | 3.0% | 6.9% |

| TCS BaNCS | 1.46 | 10.6% | 5.2% |

| Temenos | 1.12 | 3.7% | 15.2% |

| Sopra Banking Software | 0.66 | 5.6% | 2.8% |

Detailed Capabilities Evaluation by Vendor: Identifying the Best BFSI Tech Solutions for Banks 2025

To accurately identify the best BFSI tech solutions for banks 2025, financial institutions must go beyond surface-level comparisons and evaluate each vendor’s core capabilities, scalability, and long-term strategic fit. Below is a detailed breakdown of leading core banking providers and emerging challengers shaping the market.

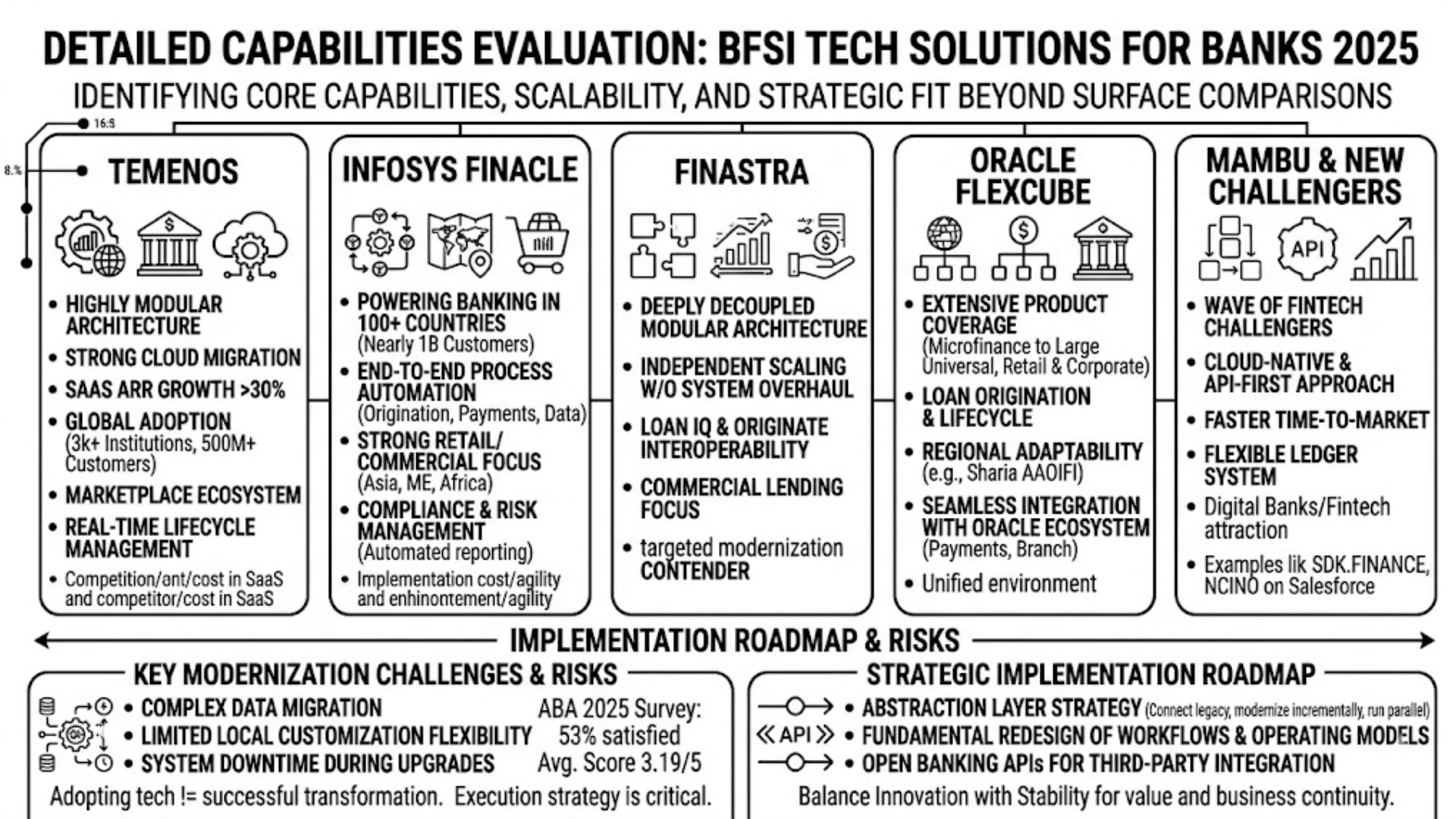

1. Temenos (T24 Core Banking)

Founded in 1993, Temenos remains one of the most widely adopted core banking platforms globally, serving over 3,000 institutions and processing transactions for more than 500 million customers daily.

Temenos stands out for its highly modular architecture and strong cloud migration capabilities. Its SaaS-driven model continues to scale rapidly, with Annual Recurring Revenue (ARR) growing over 30% year-on-year. The platform supports complex multi-entity and multi-currency operations, enabling real-time lifecycle management across deposits, lending, and treasury functions. Additionally, its marketplace-driven ecosystem allows banks to extend functionality through integrated partners.

However, Temenos faces increasing competition from cloud-native challengers. Newer platforms offer faster deployment and greater flexibility, which raises concerns for some institutions around long-term cost efficiency and data migration complexity within Temenos’ SaaS model.

2. Infosys Finacle (EdgeVerve)

Developed by Infosys and launched in 1999, Finacle powers banking operations in over 100 countries and supports nearly 1 billion end customers.

Finacle is particularly strong in retail and commercial banking, especially across Asia, the Middle East, and Africa. Its key advantage lies in end-to-end process automation, covering account origination, payments, and customer data management. The platform also excels in compliance and risk management, offering robust automated reporting aligned with global regulatory standards.

On the downside, Finacle’s architecture, originally designed for large-scale banking groups can present challenges for smaller institutions. Implementation costs may be high, and the platform can lack the agility required for rapid deployment of new digital features compared to more modern, cloud-native solutions.

3. Finastra

Finastra is widely recognized for delivering comprehensive financial software suites tailored to diverse banking needs.

Its core strength lies in a deeply decoupled modular architecture. Platforms such as Loan IQ and Originate operate independently while maintaining seamless interoperability, enabling banks to scale specific functions without overhauling entire systems. This modularity is particularly valuable in commercial lending, where Finastra offers advanced tools for managing market, credit, and operational risks throughout the loan lifecycle.

This flexibility makes Finastra a strong contender among the best BFSI tech solutions for banks 2025, especially for institutions seeking targeted modernization rather than full system replacement.

4. Oracle FLEXCUBE

Oracle FLEXCUBE is a comprehensive core banking solution designed to support institutions ranging from microfinance organizations to large universal banks.

One of its key advantages is its extensive product coverage. FLEXCUBE supports both retail and corporate banking needs, including loan origination, customer lifecycle management, post-trade processing, and real-time liquidity management. It also demonstrates strong adaptability to regional requirements, such as compliance with Sharia standards (AAOIFI), making it highly relevant in Middle Eastern markets.

Another major strength is its seamless integration with the broader Oracle ecosystem, including cloud-based solutions for payments and branch operations. This unified environment enables banks to build a cohesive, end-to-end digital infrastructure.

5. Mambu & the New Challengers (Composable Banking)

While established vendors dominate market share, a new wave of fintech challengers is redefining core banking architecture. Platforms like Mambu and SDK.finance are leading the shift toward composable banking.

Mambu, founded in 2011, pioneered a cloud-native, API-first approach built around a flexible ledger system. With over 150 clients globally, it enables significantly faster time-to-market compared to traditional monolithic systems. This makes it especially attractive for digital banks and fintech companies seeking rapid innovation.

Similarly, SDK.finance provides a versatile platform supporting use cases such as payment applications, crypto-to-fiat transactions, and digital asset accounting. Meanwhile, nCino is gaining traction with its cloud-based banking platform built on Salesforce, offering integrated solutions for account opening, loan origination, and customer relationship management.

These challengers emphasize speed, flexibility, and composability, key attributes for institutions aiming to stay competitive in a digital-first environment. As a result, they are increasingly recognized as part of the best BFSI tech solutions for banks 2025, particularly for banks pursuing agile, future-ready architectures.

Implementation Roadmap and Risks in Core Modernization

Even with the rise of the best BFSI tech solutions for banks 2025, core banking implementation remains one of the most complex and high-risk transformation projects. According to a 2025 survey by the American Bankers Association (ABA), only 53% of bankers report being “extremely” or “somewhat” satisfied with their core providers, with an average score of 3.19/5.

This gap in satisfaction is largely driven by persistent challenges, including:

- Complex data migration processes

- Limited flexibility for local customization

- System downtime during upgrades and transitions

These issues highlight a critical reality: adopting new technology does not automatically guarantee successful transformation. Execution strategy plays an equally important role.

To reduce operational risks, many banks and IT consulting partners are adopting an “Abstraction Layer” strategy. This approach introduces an intermediary layer that connects legacy systems with new platforms, allowing both environments to operate in parallel during migration. As a result, banks can modernize incrementally without disrupting day-to-day operations.

However, core modernization goes beyond simply replacing legacy systems. It requires a fundamental redesign of workflows and operating models to fully leverage digital capabilities. In parallel, banks must implement Open Banking APIs to enable seamless integration with third-party services, such as payment gateways and automated reconciliation tools.

Ultimately, successful transformation depends on balancing innovation with stability, ensuring that the transition toward the best BFSI tech solutions for banks 2025 delivers value without compromising business continuity.

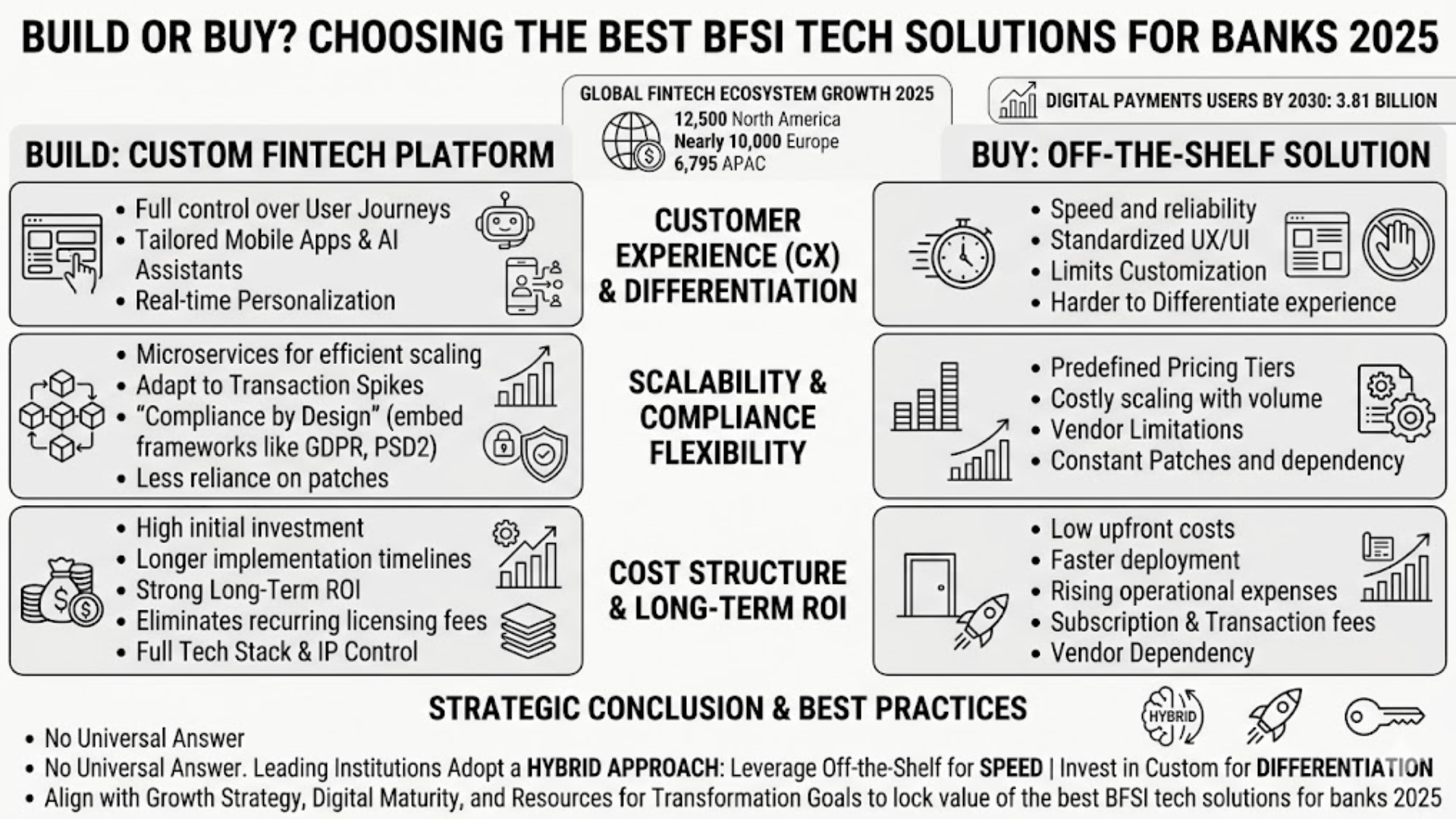

Build or Buy? Choosing the Best BFSI Tech Solutions for Banks 2025

Beyond vendor selection, financial institutions in 2025 face a deeper strategic question: should they “Buy” off-the-shelf solutions or “Build” custom fintech platforms? This decision plays a critical role in defining long-term competitiveness and directly impacts how banks adopt the best BFSI tech solutions for banks 2025.

The rise of the global fintech ecosystem has intensified this debate. By 2025, the market includes over 12,500 companies in North America, nearly 10,000 in Europe, and 6,795 in APAC. These players are reshaping financial services, especially in digital payments, a segment expected to reach 3.81 billion users by 2030. As fintech innovation accelerates, traditional banks must rethink how they build and deliver digital capabilities.

Customer Experience and Differentiation

Customer expectations in 2025 are higher than ever. Users demand instant payments, intuitive interfaces, and AI-driven financial insights.

Off-the-shelf solutions offer speed and reliability but often come with standardized UX/UI, limiting customization. This can make it difficult for banks to differentiate their digital experience.

In contrast, custom fintech development enables full control over user journeys. Banks can design tailored mobile apps, integrate AI assistants, and connect directly to data platforms for real-time personalization. This flexibility is a key reason why custom development is increasingly considered part of the best BFSI tech solutions for banks 2025, especially for customer-centric strategies.

Scalability and Compliance Flexibility

Scalability is another major factor in the Build vs. Buy decision. Off-the-shelf platforms typically rely on predefined pricing tiers, which can become costly as transaction volumes grow.

Custom-built systems, however, can leverage microservices architecture to scale more efficiently. This allows banks to adapt quickly to market expansion or transaction spikes without being constrained by vendor limitations.

Equally important is regulatory compliance. With custom development, banks can embed compliance frameworks, such as GDPR or PSD2 directly into the system from the start. This “compliance by design” approach reduces reliance on continuous patches and improves long-term system integrity.

Cost Structure and Long-Term ROI

The financial trade-offs between the two approaches are significant. Off-the-shelf SaaS solutions offer low upfront costs and faster deployment, making them attractive for quick wins. However, ongoing operational expenses can increase substantially over time due to subscription fees, transaction costs, and vendor dependency.

Custom fintech development requires higher initial investment and longer implementation timelines. Yet, it offers stronger long-term ROI by eliminating recurring licensing fees and giving banks full control over their technology stack, data, and intellectual property.

There is no universal answer to the Build vs. Buy dilemma. Leading institutions are increasingly adopting a hybrid approach, leveraging off-the-shelf platforms for speed while investing in custom development for differentiation.

Ultimately, the right balance depends on each bank’s growth strategy, digital maturity, and resource capacity. Those that align this decision with their broader transformation goals will be best positioned to unlock the full value of the best BFSI tech solutions for banks 2025.

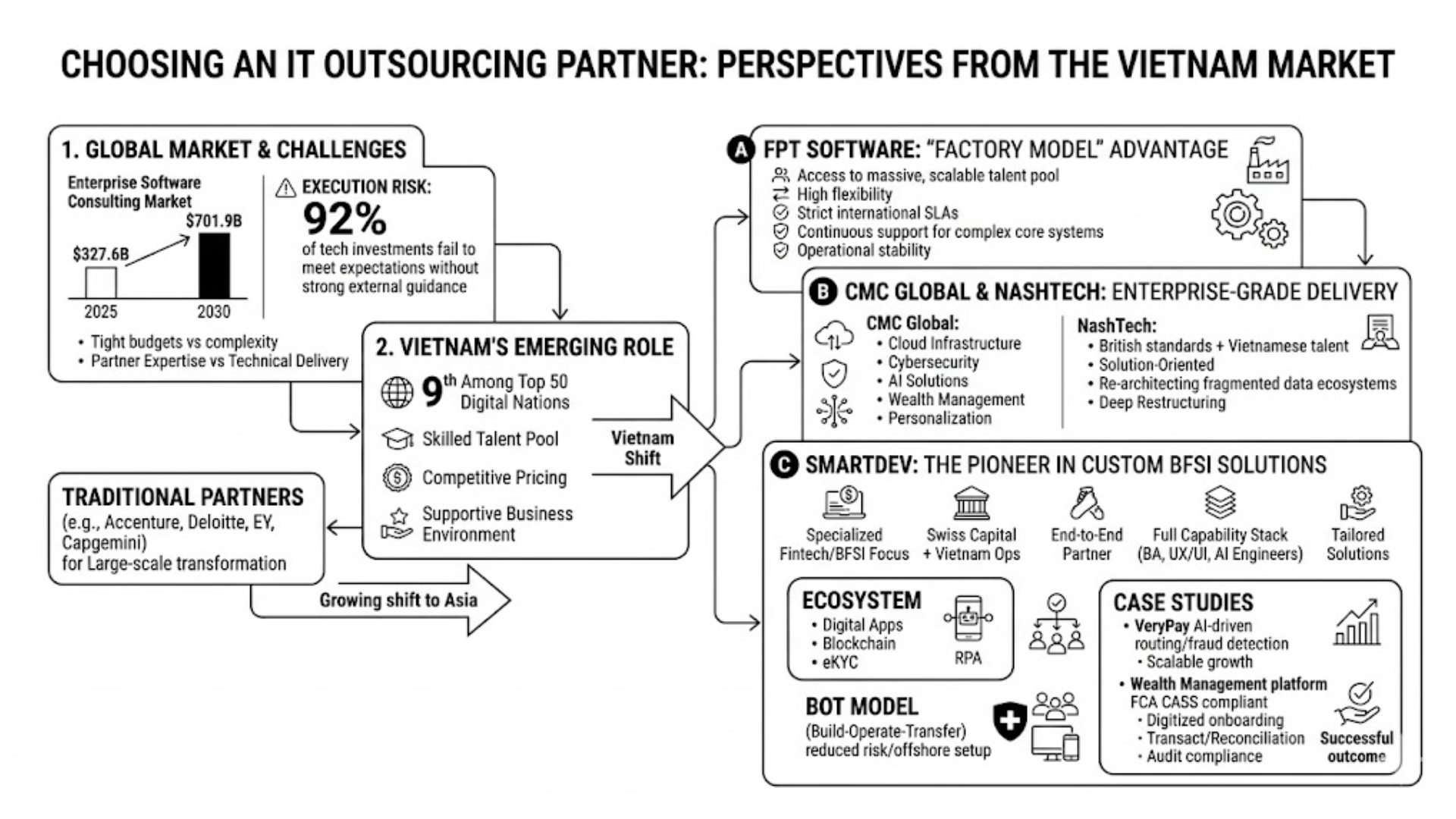

Choosing an IT Outsourcing Partner: Perspectives from the Vietnam Market

Given the complexity of financial systems and tightening internal budgets, IT outsourcing and technology consulting have become essential pillars of digital transformation. The global enterprise software consulting market is valued at $327.6 billion in 2025 and is projected to reach $701.9 billion by 2030.

At the same time, execution risk remains high. Up to 92% of tech investments fail to meet expectations without strong external guidance. This makes it critical for banks to partner with vendors that offer deep BFSI expertise, not just technical delivery when implementing the best BFSI tech solutions for banks 2025.

Traditionally, financial institutions rely on Tier-1 consultancies such as Accenture, Deloitte, EY, and Capgemini for large-scale transformation. However, to optimize cost and speed, a growing shift toward Asia—particularly Vietnam is clearly underway.

Vietnam has emerged as a leading IT outsourcing destination, ranking 9th among the top 50 digital nations. Its combination of skilled talent, competitive pricing, and a supportive business environment makes it highly attractive for BFSI technology development. Evaluating the best BFSI tech solutions for banks 2025 at the partner level reveals several key players with distinct strategies:

1. FPT Software: The “Factory Model” Advantage

As Vietnam’s largest IT services company, FPT Software offers access to a massive and scalable talent pool. Its “factory model” allows banks to quickly adjust development capacity with high flexibility while maintaining strict international SLAs.

This approach is particularly effective for large financial institutions that need continuous support for complex core systems. By combining cost efficiency with global delivery capabilities, FPT helps accelerate execution timelines and maintain operational stability.

2. CMC Global & NashTech: Enterprise-Grade Delivery

CMC Global focuses on enterprise cloud infrastructure, cybersecurity, and AI-driven financial solutions. In the BFSI space, it emphasizes wealth management and personalized financial services powered by data and automation.

NashTech, backed by British standards and Vietnamese engineering talent, takes a more solution-oriented approach. Instead of simply executing requirements, it focuses on solving complex system challenges—especially in re-architecting fragmented data ecosystems. This makes it a strong partner for banks undergoing deep digital restructuring.

3. SmartDev: The Pioneer in Custom BFSI Solutions

SmartDev stands out by maintaining a specialized focus on fintech and BFSI, rather than operating as a general outsourcing provider. Backed by Swiss capital and operating in Vietnam, the company positions itself as an end-to-end technology partner.

Its strength lies in offering a full capability stack, from Business Analysts and UX/UI Designers to AI Engineers, enabling banks to build tailored solutions aligned with strategic goals. This specialization makes SmartDev highly relevant when evaluating the best BFSI tech solutions for banks 2025.

SmartDev’s ecosystem for banking includes digital banking applications, blockchain integration, eKYC systems, and Robotic Process Automation (RPA). In addition, its Build-Operate-Transfer (BOT) model allows banks to establish offshore operations with reduced risk, before fully taking ownership of the system and team.

SmartDev Case Studies in BFSI

SmartDev’s capabilities are demonstrated through complex, real-world implementations. In the VeryPay project, the company integrated AI-driven routing systems to optimize payment flows and enhance fraud detection in real time, supporting large-scale user growth.

In another case, SmartDev developed a fully compliant wealth management platform aligned with UK FCA CASS standards. The system digitized investor onboarding, transaction management, and reconciliation processes, ensuring transparency and audit compliance.

Why “SmartDev” is a High-Intent Comparison Keyword

In the BFSI technology space, not all traffic delivers equal value. Many B2B organizations still focus heavily on Top of Funnel (ToFU) queries like “What is Fintech?” or “What is a KPI?”, which generate high traffic but low conversion impact. In contrast, Bottom of Funnel (BoFU) keywords, though lower in volume can drive conversion rates up to 2,400% higher.

This is where queries like “best BFSI tech solutions for banks 2025”, “best core banking software,” or brand-specific searches such as “SmartDev vs FPT” become critical. These are classified as High-Intent Comparison Keywords, signaling that users are close to making a purchasing decision.

1. The Vendor Evaluation Phase Indicator

When decision-makers search for terms like “compare,” “alternatives,” or “vendors,” they have already passed the awareness stage. At this point, CTOs and CMOs are actively building a shortlist for their RFP pipeline.

These searches often stem from real business pressure, such as dissatisfaction with legacy systems or the need to justify new investments. Structured comparison content helps them evaluate options clearly and present data-backed recommendations to leadership teams.

2. Risk Mitigation and Feasibility Validation

BFSI transformation projects involve significant financial and operational risks. As a result, buyers use comparison queries to validate vendor capabilities before making commitments.

Searches related to SmartDev, for example, often reflect a need to assess real-world performance—particularly in complex areas like AI implementation, payment systems, or regulatory compliance. Demonstrated success in these areas helps reduce uncertainty and builds confidence in execution.

This is why SmartDev becomes more than just a vendor name, it represents a benchmark for reliability, integration capability, and project feasibility within the best BFSI tech solutions for banks 2025 landscape.

3. CRO (Conversion Rate Optimization) Alignment

At the bottom of the funnel, SEO and Conversion Rate Optimization (CRO) are tightly connected. Content targeting high-intent comparison queries is designed not just to inform, but to convert.

Instead of broad education, these pages focus on:

- Clear value propositions and differentiators

- Data-driven comparisons between vendors

- Strong Calls to Action (CTAs) such as “Book a demo” or “Compare solutions”

In addition, trust signals such as client testimonials, case studies, and third-party reviews, play a critical role in influencing decisions. In the BFSI sector, where trust is paramount, these elements are essential for turning high-intent traffic into actual business outcomes.

Conclusion: Navigating the Best BFSI Tech Solutions for Banks 2025

The landscape of the best BFSI tech solutions for banks 2025 reflects a clear shift toward AI-driven operations, hybrid infrastructure, and more flexible core banking architectures. While major vendors still dominate, composable banking and cloud-native approaches are redefining how banks scale and innovate.

At the same time, the rise of custom development and specialized outsourcing partners like SmartDev, FPT, and CMC is helping banks accelerate transformation with better cost control. Ultimately, aligning technology choices with real buyer intent, especially high-intent comparison queries is key to staying competitive in this evolving market.