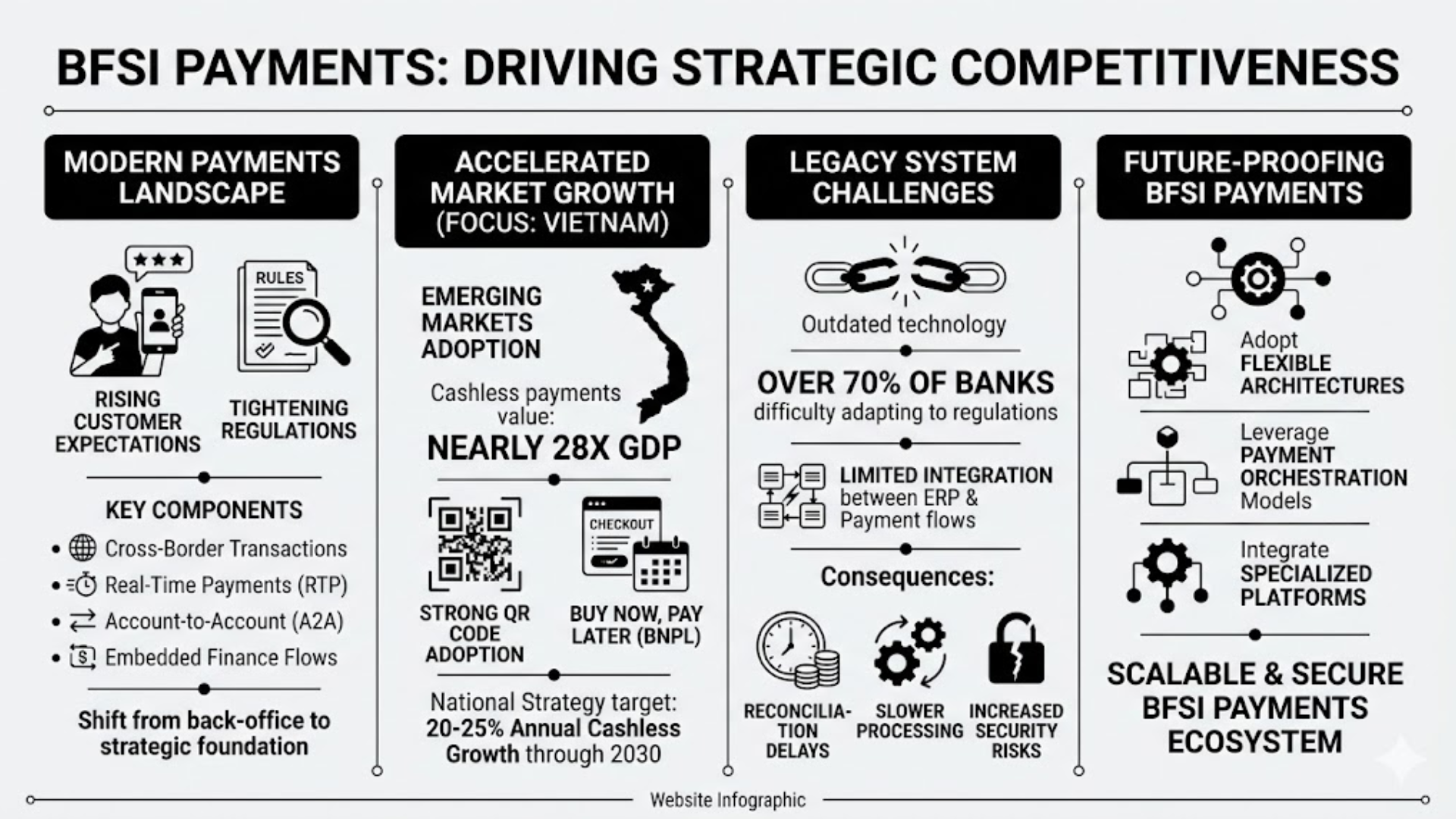

The Banking, Financial Services, and Insurance (BFSI) industry is undergoing rapid transformation as BFSI Payments shift from a back-office function to a strategic foundation for competitiveness. Modern BFSI Payments now include cross-border transactions, Real-Time Payments (RTP), Account-to-Account (A2A) transfers, and Embedded Finance flows. As customer expectations rise and regulations tighten, financial institutions must replace rigid legacy systems with scalable and data-driven payment architectures.

The expansion of digital transactions continues to accelerate the adoption of BFSI Payments, particularly in emerging markets such as Vietnam. The value of cashless payments has reached nearly 28 times the national GDP, driven by strong QR code adoption and the growth of Buy Now, Pay Later (BNPL) services. In addition, the National Financial Inclusion Strategy targets annual growth of 20–25% in cashless transactions through 2030, positioning digital payments as a core infrastructure connecting businesses, citizens, and government services.

Despite this momentum, legacy BFSI Payments systems remain a major challenge. More than 70% of banks report difficulty adapting to regulatory changes due to outdated technology. Limited integration between ERP platforms and payment flows often causes reconciliation delays, slower processing speeds, and increased security risks. To remain competitive, organizations must adopt flexible architectures, leverage payment orchestration models, and integrate specialized platforms that support scalable and secure BFSI Payments ecosystems.

The Dual Pressure: Compliance and Data Optimization in BFSI Payments

Today, BFSI Payments systems face two powerful forces: global standardization and strict local regulations. These are not just compliance tasks. Instead, they act as key drivers pushing banks to modernize their technology stack.

The Data Revolution with ISO 20022

On a global level, ISO 20022 is transforming how BFSI Payments are processed. Unlike legacy SWIFT MT formats (such as MT103 or MT101), this standard uses a flexible XML structure. As a result, it enables richer, well-structured data exchange. This improves interoperability, reduces manual intervention, and strengthens AML and fraud detection accuracy.

However, the shift also creates serious technical pressure. By November 2026, SWIFT will require all cross-border payments to use structured or hybrid address data, with clearly defined fields like Town/City and Country Code. At the same time, organizations sending MT101 must migrate to the pain.001 format.

For banks using legacy core systems, this creates a “double-edged sword.” The increased data volume requires major database upgrades and parallel data storage. In many cases, large ISO 20022 messages entering outdated systems lead to data truncation. This breaks Straight-Through Processing (STP) and forces manual review.

To manage this, some banks deploy translation middleware to convert MX messages back to MT formats. While this ensures short-term compliance, it creates a “translation trap.” As a result, banks lose the full value of ISO 20022 data and increase long-term system complexity and costs.

Reshaping Authentication in Vietnam

In Vietnam, BFSI Payments are also being reshaped by Circular 17/2024/TT-NHNN. By July 1, 2025, organizations must complete biometric verification for legal representatives, accountants, and authorized users. This process requires chip-based ID cards or valid passports and can be done at branches or via mobile apps.

The consequences of non-compliance are strict. Corporate accounts may lose access to digital transfers and withdrawals. In parallel, magnetic stripe cards will be fully replaced by EMV chip cards to improve encryption and reduce fraud risks.

These changes go beyond administration. They require banks to redesign their BFSI Payments architecture. Systems must integrate real-time API calls to national biometric databases before approving high-value transactions, often above 50 million VND. In addition, new security rules demand frequent testing of mobile banking apps and restrict outdated versions.

| Aspect | Legacy Payment Systems | Modern BFSI Payments Systems |

|---|---|---|

| Data Standards |

Dependent on SWIFT MT formats, limited information, free-text addresses. |

Native processing of ISO 20022 XML data, fully structured/hybrid addressing. |

| Transaction Authentication |

Relies on static passwords, basic SMS OTPs. Insecure magnetic stripe cards. |

Multi-layer tokenization, real-time biometric API matching with national databases (Circular 17). |

| Communication Scalability |

Siloed systems, difficult to communicate with ERP software or corporate treasuries. |

API-first open architecture, allowing reconciliation data to flow directly into ERPs. |

| Compliance Responsiveness |

Patchwork deployment of translation middleware, high risk of data “truncation”. |

Microservices-oriented architecture, allowing specific module updates without impacting the core system. |

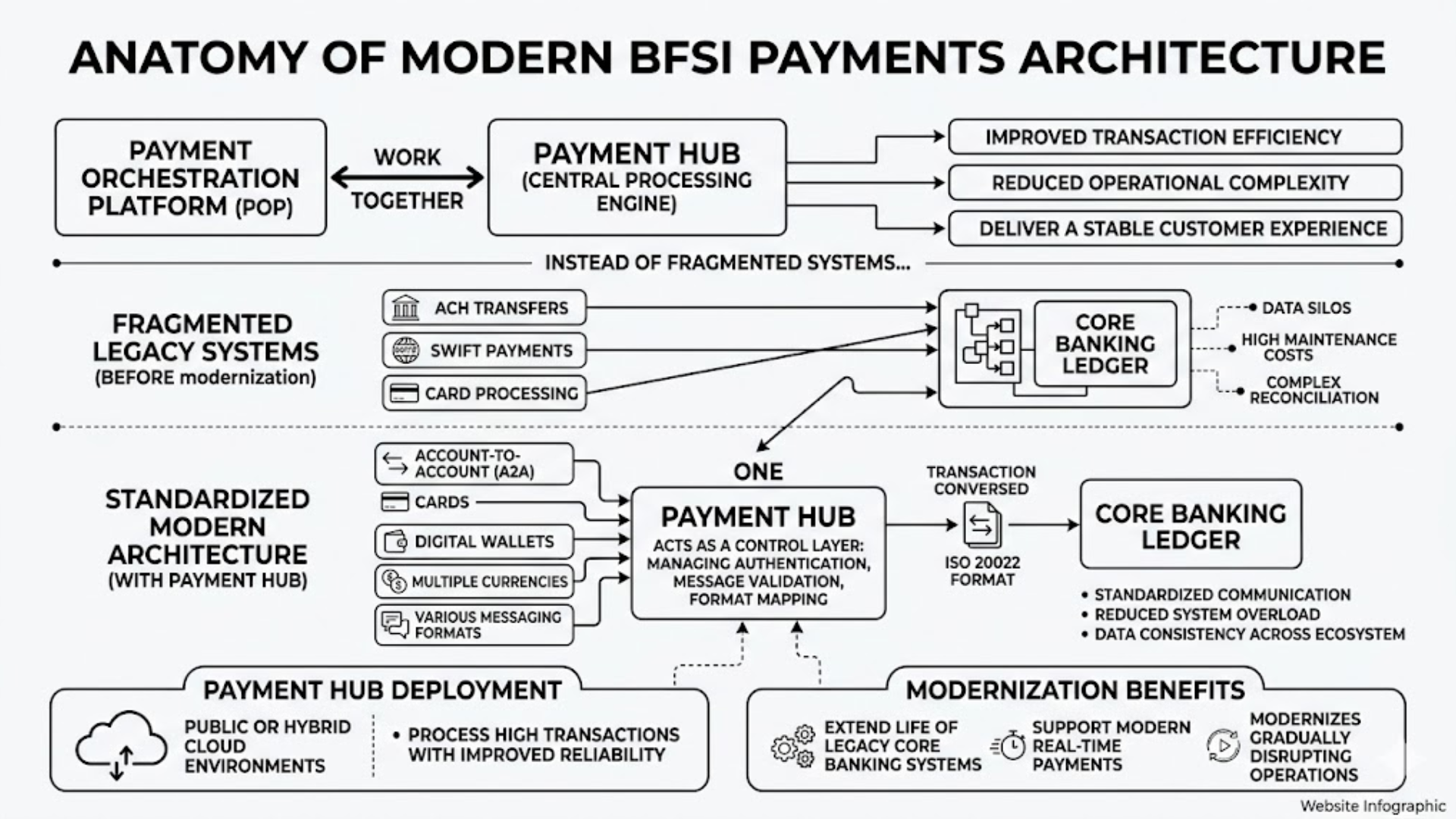

Anatomy of Modern BFSI Payments Architecture

To overcome regulatory pressure and remove the limitations of legacy infrastructure, modern BFSI Payments architecture often combines two key components: the Payment Hub and the Payment Orchestration Platform (POP). These elements work together to improve transaction efficiency, reduce operational complexity, and deliver a more stable customer experience. Instead of relying on fragmented systems, financial institutions can build a unified payment ecosystem that supports scalability and long-term innovation.

Payment Hub: The Central Processing Engine

A Payment Hub acts as the centralized engine for processing all payment flows within the BFSI Payments environment. It supports multiple instruments such as Account-to-Account transfers, cards, digital wallets, currencies, and messaging formats. Rather than maintaining separate systems for each payment method, organizations can manage transactions through one standardized architecture.

Historically, many banks implemented individual systems for ACH transfers, SWIFT payments, or card processing. Over time, these isolated platforms created data silos, increased maintenance costs, and complicated reconciliation processes. As transaction volumes increased, legacy systems struggled to maintain performance and flexibility.

A modern Payment Hub solves this problem by standardizing communication with the Core Banking ledger. Instead of allowing multiple subsystems to connect directly to the core, the hub acts as a control layer that manages authentication, message validation, and format mapping. For example, transactions can be converted into ISO 20022 format before reaching the core system. This structure reduces system overload and improves data consistency across the BFSI Payments ecosystem.

When deployed on public cloud or hybrid cloud environments, Payment Hubs enable financial institutions to process high transaction volumes with improved reliability. They also extend the lifespan of legacy core banking systems while supporting modern real-time payment requirements. As a result, organizations can modernize gradually without disrupting existing operations.

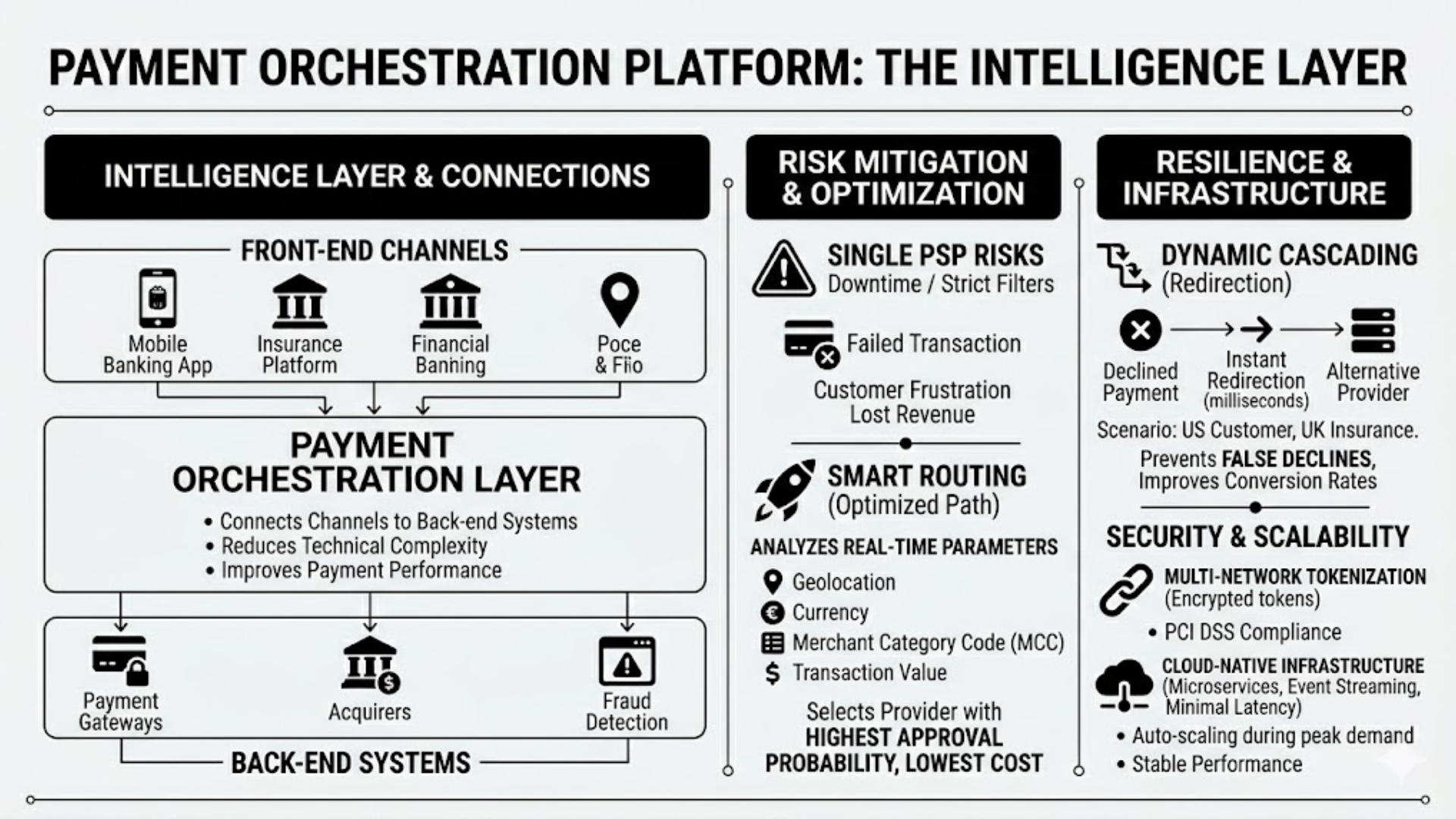

Payment Orchestration Platform: The Intelligence Layer

While the Payment Hub manages transaction processing, the Payment Orchestration Platform (POP) acts as the intelligence layer within BFSI Payments architecture. This platform connects front-end channels such as mobile banking apps or insurance platforms with multiple payment gateways, acquirers, and fraud detection systems. By coordinating these integrations, orchestration platforms reduce technical complexity and improve payment performance.

Relying on a single Payment Service Provider may appear simple, but it creates operational risks. If the provider experiences downtime or applies strict risk filters, transactions may fail even when customers have valid payment credentials. Failed transactions often result in customer frustration and lost revenue opportunities.

To reduce these risks, orchestration platforms use smart routing. This capability analyzes transaction parameters in real time, including geolocation, currency, Merchant Category Code, and transaction value. Based on these factors, the system selects the payment provider with the highest approval probability and the lowest processing cost. Smart routing improves authorization rates and ensures stable performance across different markets.

Another important capability is dynamic cascading. When one acquirer rejects a transaction, the orchestration layer automatically sends the request to an alternative provider. This process happens within milliseconds and remains invisible to the end user. In complex cross-border scenarios, dynamic cascading helps prevent false declines and improves conversion rates for digital services.

For example, a customer in the United States may attempt to pay for an insurance product offered by a company in the United Kingdom. If the first acquirer declines the payment due to risk thresholds, the orchestration system instantly redirects the transaction to another provider that supports cross-border processing. The customer completes the payment without noticing any disruption.

Security and Scalability in BFSI Payments

Security requirements remain a critical concern in BFSI Payments architecture. Modern orchestration platforms support multi-network tokenization, which replaces sensitive card data with encrypted tokens. This approach reduces exposure to data breaches and supports compliance with PCI DSS standards.

Cloud-native infrastructure further improves scalability and resilience. Technologies such as event streaming and microservices allow orchestration platforms to process large transaction volumes with minimal latency. These capabilities enable BFSI Payments systems to automatically scale during peak demand while maintaining stable performance.

Realizing the Power of BFSI Payments Across Service Segments

The true advantage of modern BFSI Payments lies in the ability to customize payment architecture for different financial service segments. Unlike traditional payment systems, Payment Orchestration enables organizations to solve specific operational bottlenecks, improve transaction visibility, and enhance liquidity management across complex financial ecosystems.

Breakthroughs in Insurtech Operations

In the global insurance market, valued at more than $6 trillion, payment flows are often slowed by manual processes, fragmented systems, and disconnected operational platforms. Many insurers rely on separate infrastructures for premium collection and claims disbursement, which creates inefficiencies in treasury management. As a result, companies often face the “trapped cash” challenge, where capital must remain locked within local entities to ensure claims liquidity.

By implementing an orchestration layer within BFSI Payments, insurers can centralize premium collection and claims payout processes into a unified management platform. Customers can pay premiums using multiple channels, including ACH transfers, credit cards, and digital wallets such as PayPal or Apple Pay. More importantly, real-time payments (RTP) and API-based integration allow insurers to release claim payouts immediately after approval, often through direct A2A transfers or virtual cards. Faster payouts improve customer satisfaction while reducing administrative workload for finance teams.

Advanced Liquidity Management for Corporate Banking (B2B Payments)

In corporate banking, payment infrastructure must support complex global trade flows, supply chain transactions, and vendor payments across multiple currencies. Organizations increasingly expect banks to integrate BFSI Payments directly into Treasury Management Systems (TMS) and Enterprise Resource Planning (ERP) platforms. Without modern architecture, companies struggle to maintain real-time visibility into cash flow and cross-border reconciliation processes.

Through Open API frameworks, modern BFSI Payments platforms enable real-time balance monitoring, automated reconciliation, and improved transaction transparency. Payment orchestration supports smart routing capabilities that optimize transaction paths based on currency, geography, and processing costs. As a result, Chief Financial Officers can reduce foreign exchange expenses, improve working capital efficiency, and manage global liquidity with greater precision.

Explore how SmartDev partners with BFSI teams through a focused AI sprint to validate use cases, align stakeholders, and define a clear path forward before AI development begins.

SmartDev helps BFSI organizations clarify AI use cases and assess feasibility, enabling confident decisions and reducing risks before committing to AI development.

Learn how SmartDev accelerates AI initiatives, ensuring rapid deployment and reduced time to market.

Strengthen Your BFSI Security Testing with UsThe Zero-Downtime Migration Roadmap for BFSI Payments

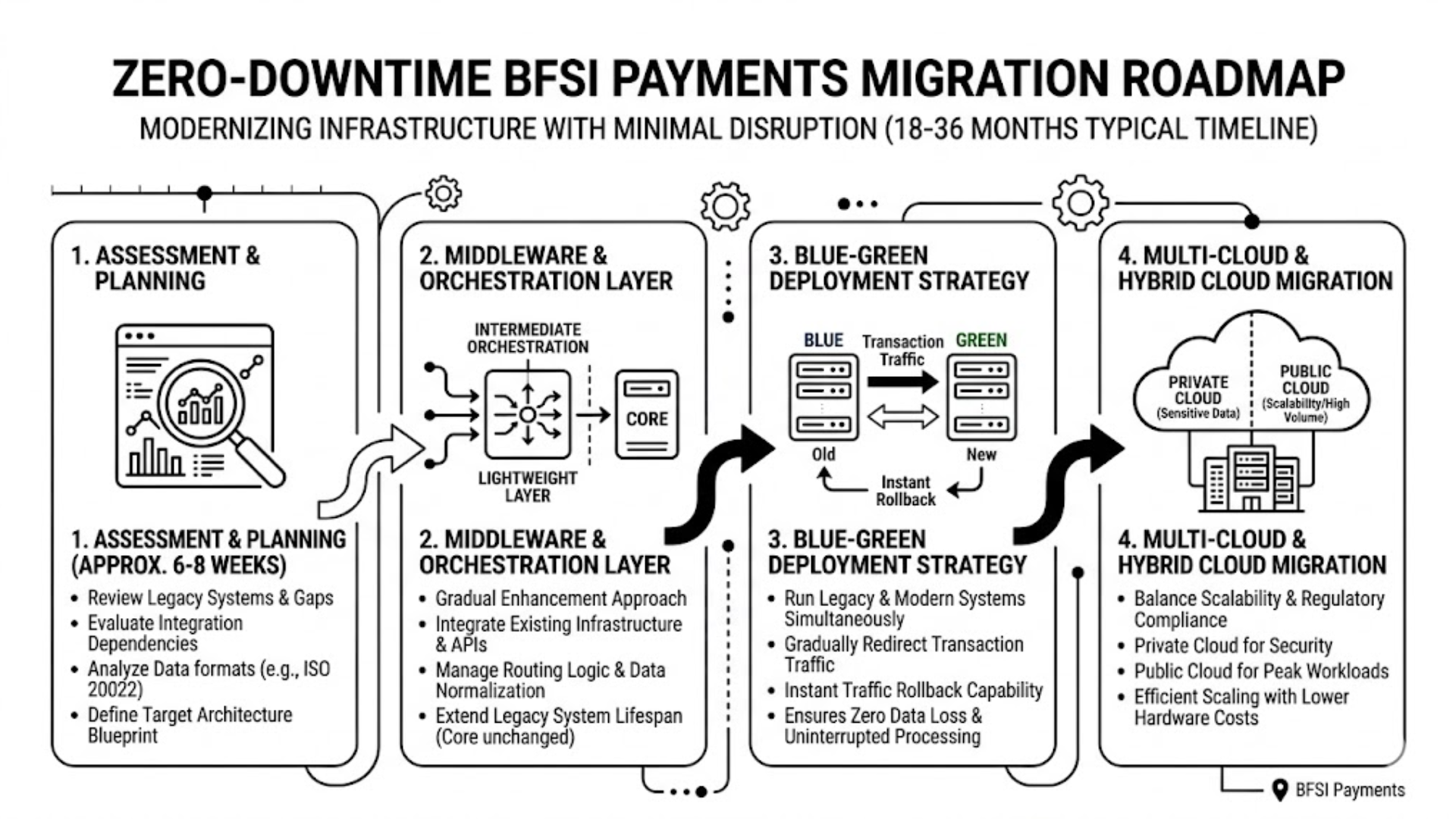

Modernizing core BFSI Payments infrastructure is often compared to major surgery because any system interruption can directly impact customer transactions and regulatory compliance. As a result, many banks hesitate to replace legacy mainframe systems and instead rely on temporary fixes. However, advanced integration strategies now enable financial institutions to deploy next-generation BFSI Payments architecture with minimal disruption, typically within an 18–36 month roadmap.

Phase 1: Assessment and Planning

The transformation process begins with a structured assessment phase lasting approximately six to eight weeks. During this stage, organizations review legacy payment systems, evaluate integration dependencies, and identify gaps between internal data formats and global standards such as ISO 20022. This analysis helps define the target architecture and ensures alignment with regulatory and operational requirements.

Clear planning also reduces migration risk by identifying potential data inconsistencies early. With a detailed architecture blueprint, financial institutions can prioritize modernization initiatives while maintaining business continuity.

Phase 2: Middleware and Orchestration Layer Implementation

Instead of replacing core banking systems immediately, many organizations implement a middleware or orchestration layer that integrates with existing infrastructure. This lightweight layer manages routing logic, connects with external APIs, and performs data normalization before sending structured accounting entries to the core system.

By introducing orchestration gradually, banks can enhance BFSI Payments capabilities without disrupting critical transaction workflows. This approach extends the lifespan of legacy systems while enabling integration with modern payment technologies.

Phase 3: Blue-Green Deployment Strategy

Blue-green deployment allows financial institutions to run legacy and modern BFSI Payments systems simultaneously. Transaction traffic is gradually redirected from the old system to the new architecture without affecting end users. If any technical issue occurs, traffic can be instantly routed back to the previous environment, ensuring zero data loss and uninterrupted payment processing.

This deployment method significantly reduces operational risk and supports continuous system validation throughout the migration journey.

Phase 4: Multi-cloud and Hybrid Cloud Migration

Many financial institutions adopt hybrid cloud models to balance scalability with regulatory compliance. Private cloud environments protect sensitive financial data, while public cloud infrastructure supports high transaction volumes and fluctuating workloads.

Hybrid cloud architecture allows BFSI Payments platforms to scale efficiently during peak transaction periods without requiring significant hardware investment. This flexibility improves performance, reduces infrastructure costs, and ensures readiness for future digital payment innovations.

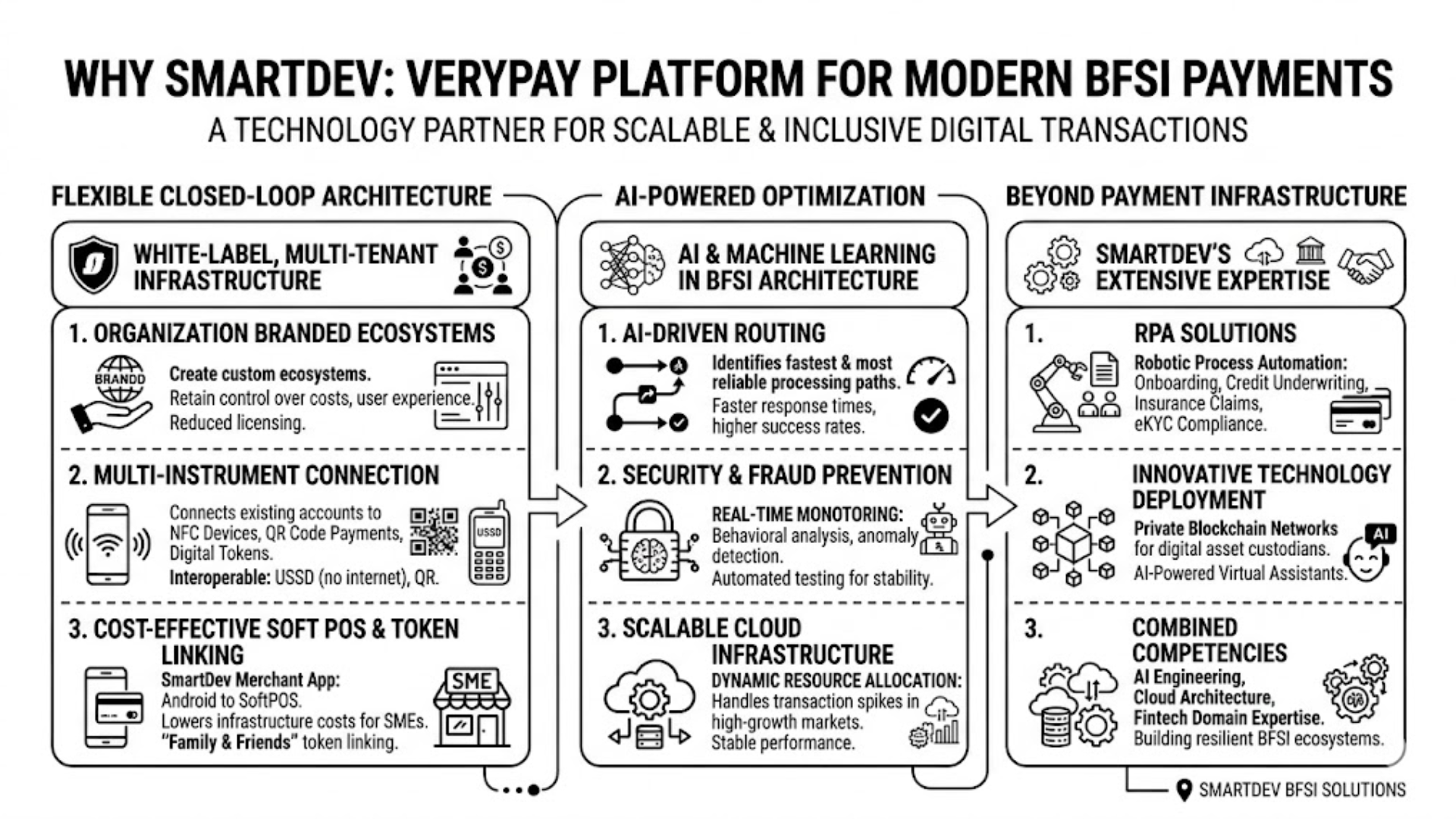

Why SmartDev: VeryPay Platform for Modern BFSI Payments

Applying advanced architecture in BFSI Payments requires more than strong development skills. Financial institutions need a technology partner with deep expertise in payment flows, compliance requirements, and AI-driven optimization. SmartDev demonstrates this capability through the development of VeryPay, a flexible payment connection platform designed to support financial inclusion and scalable digital transactions.

VeryPay enables Mobile Network Operators, e-wallet providers, and retail ecosystems to build customized payment environments without depending entirely on traditional card networks. This approach helps organizations maintain greater control over transaction costs, user experience, and system scalability across emerging markets.

Flexible Closed-Loop Architecture

Unlike traditional providers, VeryPay does not operate as a bank or financial fund holder. Instead, the platform offers a white-label, multi-tenant infrastructure that allows organizations to create closed-loop payment ecosystems under their own brand. This structure reduces licensing complexity while improving flexibility in BFSI Payments deployment strategies.

The platform connects existing bank accounts or e-wallets with multiple payment instruments, including NFC-enabled devices, QR code payments, and digital tokens. SmartDev’s Merchant App can transform any Android smartphone into a SoftPOS terminal, allowing merchants to accept payments without investing in expensive POS hardware. This significantly lowers infrastructure costs for small and medium-sized businesses.

VeryPay also supports interoperability through QR code scanning and USSD protocols. With USSD functionality, users in remote areas can transfer money, pay bills, or check balances without requiring internet access. These capabilities expand financial inclusion while maintaining stable BFSI Payments performance across diverse connectivity environments.

Another distinctive feature is the “Family and Friends” token-linking capability. Multiple physical cards, wearables, or payment tokens can connect to a single primary account. This flexibility supports family expense management, corporate allowances, and shared spending scenarios. As a result, organizations can accelerate user adoption while improving payment convenience.

AI-Powered Optimization in BFSI Payments

SmartDev enhances BFSI Payments performance by embedding Artificial Intelligence and Machine Learning into the VeryPay platform architecture. AI-driven routing algorithms continuously analyze transaction data to identify the fastest and most reliable processing paths. This approach improves response time while maintaining high transaction success rates.

AI also strengthens payment security through behavioral analysis and anomaly detection. The system monitors transaction patterns in real time to detect fraud risks without introducing delays for legitimate users. Automated testing capabilities further improve system stability by identifying vulnerabilities earlier in the development lifecycle.

Combined with cloud-native infrastructure, VeryPay can dynamically allocate computing resources to handle sudden transaction spikes in high-growth markets. This ensures stable BFSI Payments performance even during periods of rapid digital adoption.

Beyond Payment Infrastructure

SmartDev’s expertise extends beyond payment platform development. The company has implemented Robotic Process Automation solutions to streamline onboarding, credit underwriting, insurance claims processing, and eKYC compliance workflows. In addition, SmartDev has designed private blockchain networks for digital asset custodians and deployed AI-powered virtual assistants that improve customer communication and analytics capabilities.

By combining AI engineering, cloud architecture, and fintech domain expertise, SmartDev supports financial institutions in building resilient and scalable BFSI Payments ecosystems aligned with long-term digital transformation strategies.

Conclusion

The shift toward modern BFSI Payments is redefining how financial institutions compete in the digital economy. Legacy batch-processing systems can no longer support real-time data exchange, regulatory compliance, or scalable API ecosystems. As standards such as ISO 20022 and stricter identity regulations evolve, outdated architectures increase operational risk and limit innovation capacity.

A future-ready BFSI Payments architecture combines Payment Hub standardization with intelligent Payment Orchestration. This model improves transaction reliability, reduces decline rates, and strengthens liquidity management across banking and insurance environments. At the same time, it enhances customer payment experience through faster, more secure, and more flexible transaction flows.

With platforms such as VeryPay and SmartDev’s AI-driven engineering capabilities, financial institutions can modernize payment infrastructure using zero-downtime strategies. By investing in scalable BFSI Payments solutions today, organizations can transform payment systems into a long-term competitive advantage.