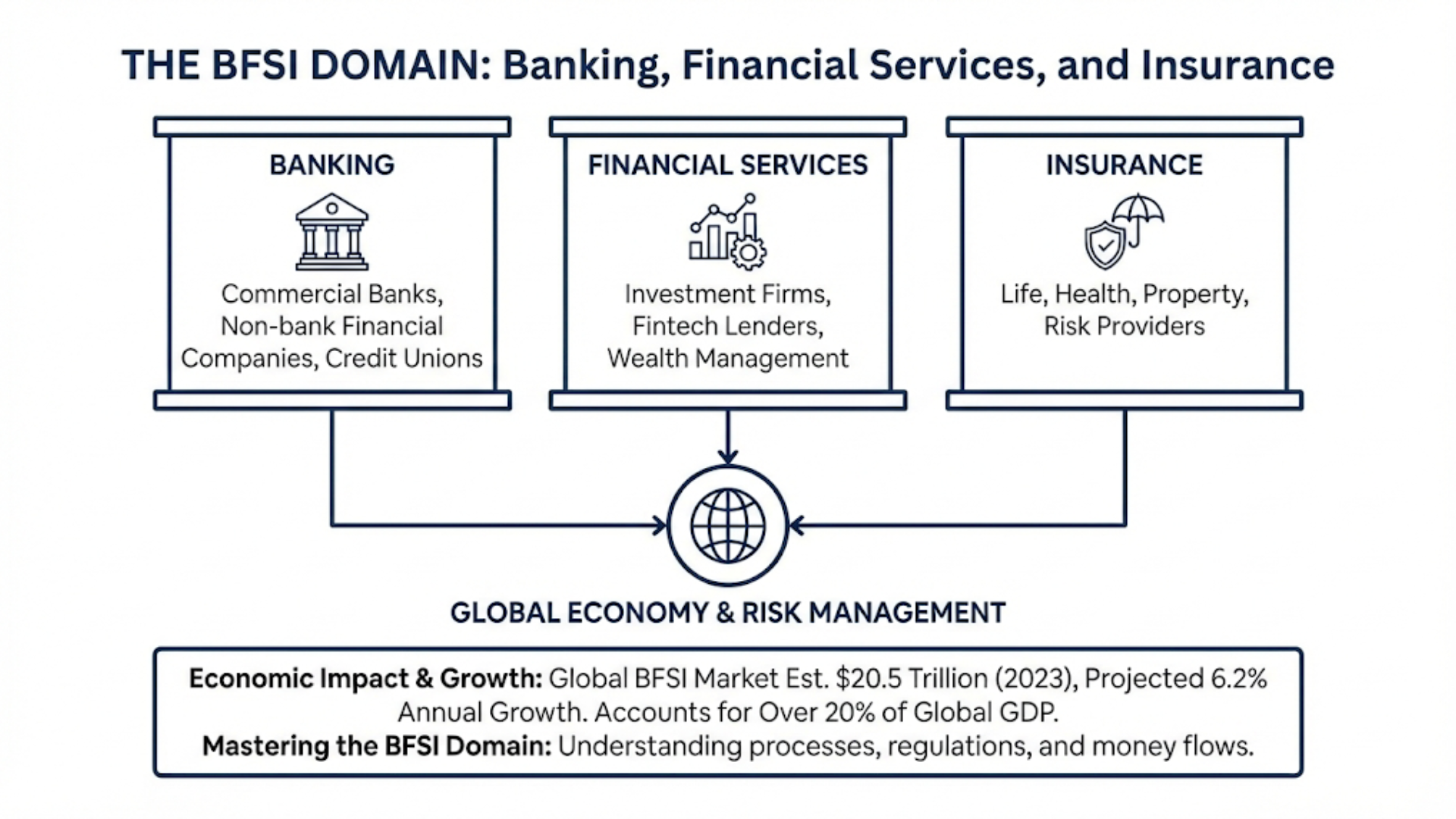

The term BFSI domain refers to the combined sectors of Banking, Financial Services, and Insurance. In other words, it encompasses commercial banks, non-bank financial companies, investment firms, insurance providers, and related regulatory bodies and institutions. Together, these organizations manage money, credit, investments and risk on a global scale. The BFSI sector underpins the entire economy – handling deposits, loans, payments, investments, and insurance coverage for individuals and businesses.

As of 2023, the global BFSI market was estimated at $20.5 trillion, and it is projected to grow at about 6.2% annually through 2030. In fact, the World Bank reports that BFSI activities account for over 20% of global GDP. This reflects the sector’s enormous economic impact: in good times it fuels growth, and in downturns (as during the 2008 crisis) its resilience helps stabilize economies.

In practical terms, anyone asking “What is the BFSI domain?” should understand that it is not a single company or product but a broad industry group. The domain includes everything from deposit-taking banks and credit unions to fintech lenders, from stock brokerage and wealth management firms to insurance companies covering life, health, property and other risks. All these organizations share a common focus on financial intermediation and risk management.

Mastering the BFSI domain requires knowledge of specialized processes (e.g. KYC customer verification, credit underwriting, claims adjudication, regulatory compliance) and an understanding of how money flows between people, businesses and markets. For IT professionals, business analysts, and investors new to BFSI, building this domain knowledge is crucial, since effective software or strategy in this space depends on understanding its unique products and regulations.

Core Sectors of the BFSI Domain

To clearly understand what is BFSI domain, it’s important to look beyond the acronym. BFSI represents a tightly connected ecosystem of banking, financial services, and insurance — three sectors that collectively power nearly every financial activity in the global economy.

From everyday retail payments to large-scale capital investments and risk protection, these industries form the backbone of modern finance. While each sector operates with different business models and regulations, they increasingly share the same technology infrastructure, customer data systems, and digital transformation challenges.

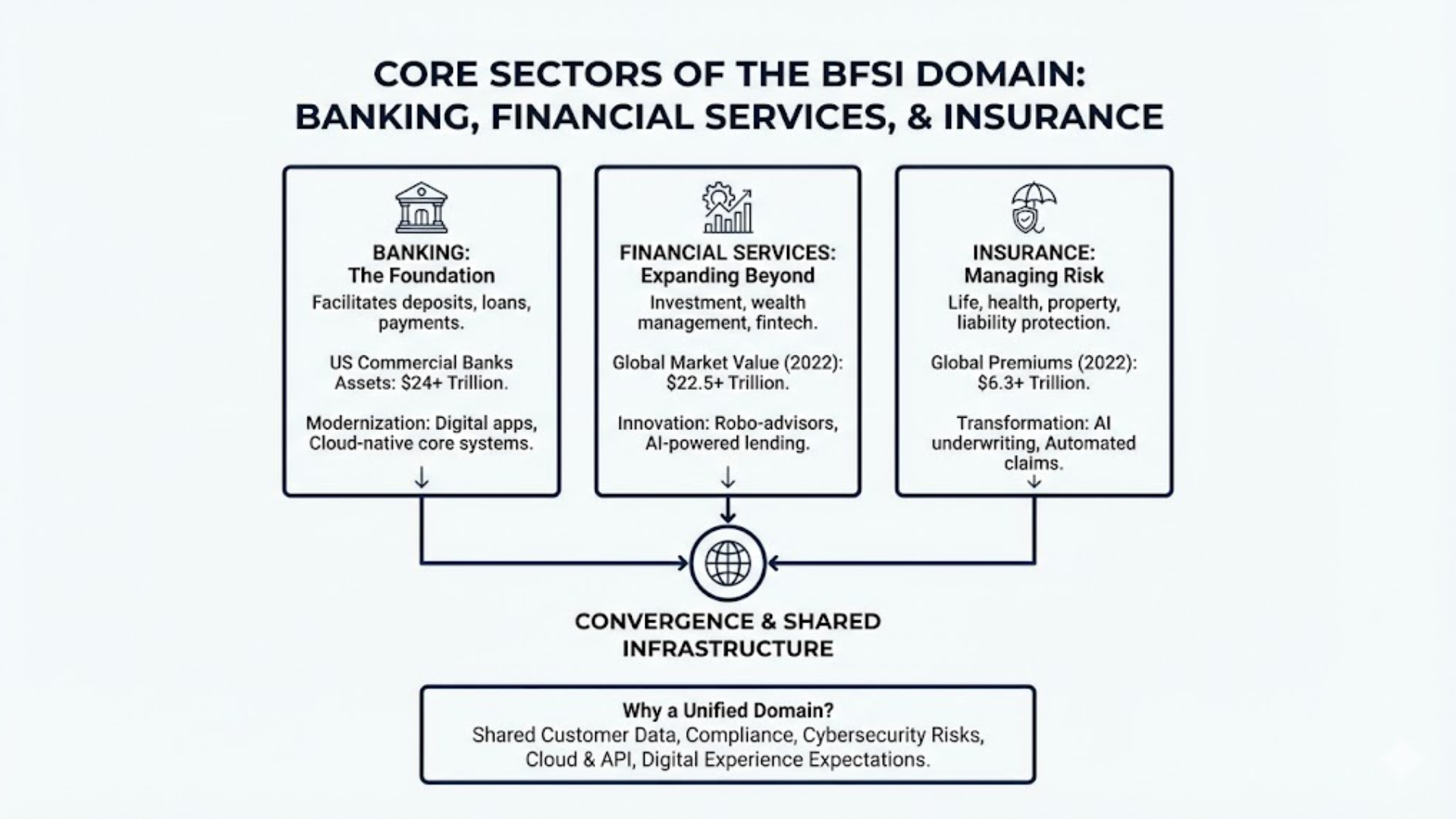

Banking: The Foundation of Financial Infrastructure

Banking remains the core pillar of the BFSI domain, responsible for facilitating deposits, loans, payments, and transactional services for both individuals and enterprises.

Commercial banks, retail banks, credit unions, and payment processors collectively manage trillions of dollars in assets worldwide. In the United States alone, more than 4,500 commercial banks oversee assets exceeding $24 trillion, demonstrating the scale and systemic importance of this sector.

However, modern banking is no longer branch-centric. Customers expect real-time, mobile-first services. As a result, financial institutions are rapidly modernizing their platforms with:

- Digital banking apps

- Online payment gateways

- API-based integrations

- Cloud-native core systems

This shift toward digital-first banking is driving significant demand for secure, scalable software solutions across the BFSI technology landscape.

Financial Services: Expanding Beyond Traditional Banking

While banking forms the base, the broader financial services sector extends into investment, wealth management, capital markets, and fintech innovation.

This segment includes investment banks, brokerage firms, asset managers, private equity funds, lending platforms, and emerging fintech startups. Together, they enable businesses to raise capital, individuals to grow wealth, and markets to function efficiently.

The size of this opportunity is substantial. The global financial services market was valued at approximately $22.5 trillion in 2022 and continues to expand as digital products reshape how consumers access credit, investments, and payments.

Today, innovation in this space is largely technology-driven. Robo-advisors, embedded finance, blockchain payments, and AI-powered lending platforms are redefining customer expectations and operational models alike.

Insurance: Managing Risk in a Data-Driven World

Insurance completes the BFSI ecosystem by addressing risk protection and financial stability. Life, health, property, and liability insurers help individuals and businesses mitigate financial uncertainty. In 2022, global insurance premiums exceeded $6.3 trillion, a clear indicator of how critical this sector is to economic resilience.

At the same time, insurance companies are undergoing their own digital transformation. Advanced analytics, AI-based underwriting, and automated claims processing are replacing manual processes, improving both efficiency and customer experience.

Why These Three Sectors Form One Unified Domain

Although banking, financial services, and insurance differ operationally, they increasingly converge in practice.

They share:

- Customer identity and transaction data

- Compliance requirements

- Cybersecurity risks

- Cloud and API infrastructures

- Digital customer experience expectations

This convergence is precisely why the term BFSI domain exists and why specialized technology expertise is required to support it.

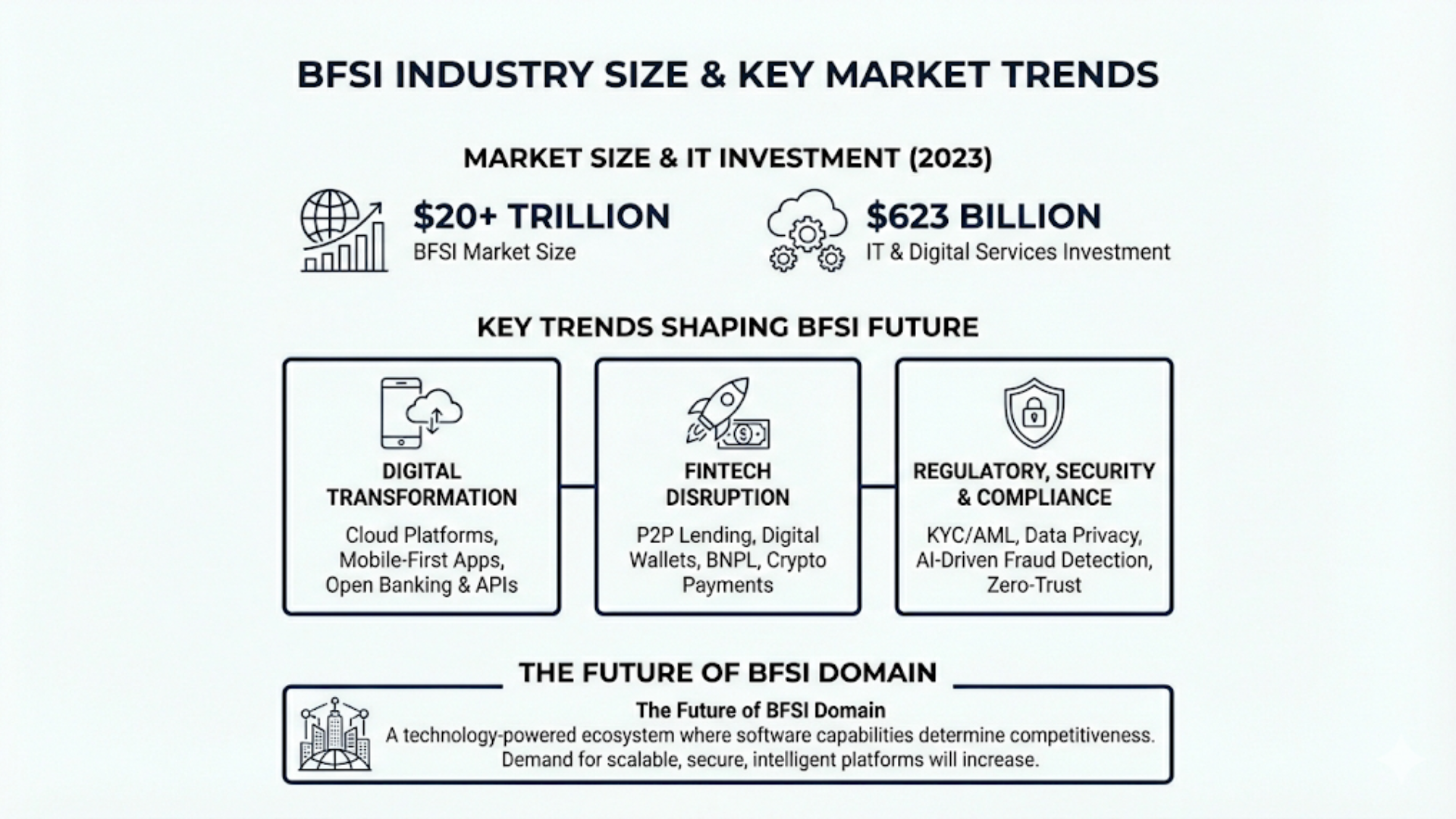

BFSI Industry Size and Key Market Trends

The BFSI industry is one of the largest and most technology-intensive sectors globally. In 2023, the total BFSI market size was estimated at over $20 trillion. More notably, the industry invested around $623 billion in IT and digital services in a single year, signaling aggressive modernization efforts.

This rapid investment is fueled by several major trends shaping the future of BFSI.

Digital Transformation Across Financial Institutions

Customers now demand seamless, always-on financial experiences. Banks and insurers must deliver services that are instant, personalized, and secure.

To meet these expectations, organizations are migrating to cloud platforms, launching mobile-first applications, and adopting open banking frameworks. Open APIs enable faster innovation and integration with third-party ecosystems, creating entirely new service models.

FinTech Disruption and Innovation

Fintech startups continue to challenge traditional players by offering simpler and faster solutions. Global fintech investment reached nearly $94 billion, accelerating the development of peer-to-peer lending, digital wallets, BNPL services, and crypto-based payments.

Rather than competing directly, many BFSI enterprises now collaborate with fintech partners to accelerate innovation and reduce time-to-market.

Regulatory, Security, and Compliance Pressures

Because BFSI handles highly sensitive financial data, regulatory compliance remains critical. Institutions must continuously adapt to evolving KYC, AML, and data privacy standards. Simultaneously, cybersecurity threats are growing in sophistication. As a result, organizations are adopting AI-driven fraud detection, zero-trust architectures, and RegTech solutions to safeguard operations.

The Future of the BFSI Domain

So, what is BFSI domain today? It is no longer just a traditional financial sector. It is a highly digital, technology-powered ecosystem where software capabilities determine competitiveness.

As banking, financial services, and insurance continue to modernize, demand for scalable platforms, secure architectures, and intelligent automation will only increase. Businesses that embrace this transformation will lead the next generation of financial innovation.

AI and Machine Learning in BFSI: Powering the Next Wave of Financial Innovation

When discussing what is BFSI domain today, it is impossible to ignore one defining factor: artificial intelligence.

AI and machine learning are no longer experimental technologies within banking, financial services, and insurance. They have become foundational capabilities that directly influence competitiveness, customer experience, and operational resilience. For many institutions, AI adoption now determines whether they can scale efficiently or fall behind faster, more agile digital players.

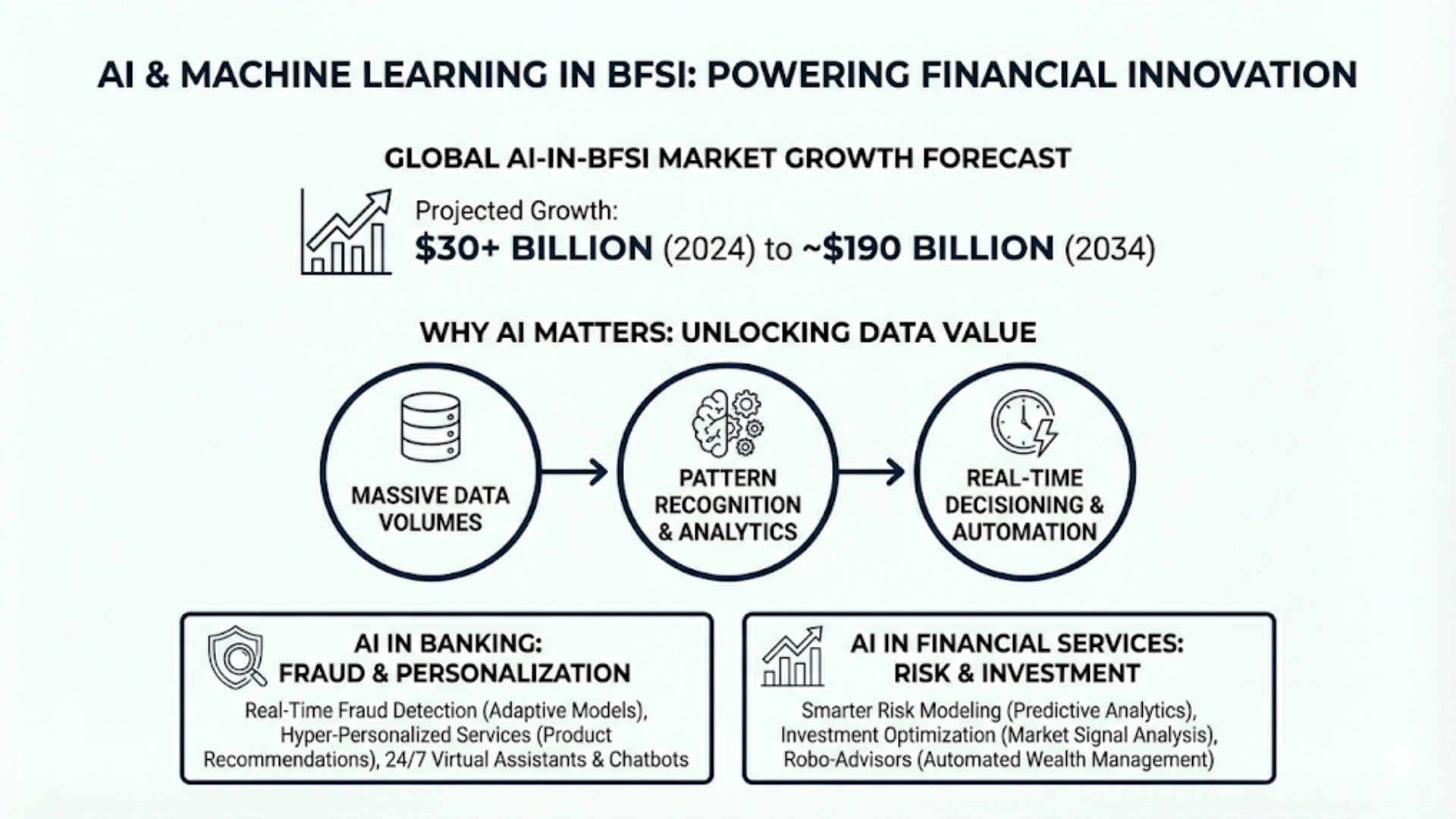

Market signals clearly reflect this shift. Industry analysts forecast explosive growth in AI investments across the BFSI sector. The global AI-in-BFSI market is expected to grow from over $30 billion in 2024 to nearly $190 billion by 2034, representing one of the fastest expansion rates across all industries. Financial institutions alone invested tens of billions of dollars in AI technologies last year, ranging from fraud detection engines and customer chatbots to predictive analytics and intelligent automation platforms.

This rapid investment is not driven by hype. It is driven by necessity.

Why AI Matters So Much in the BFSI Domain

Every second, banks process transactions, insurers evaluate claims, lenders assess credit risk, and investment firms analyze market movements. These activities produce massive volumes of behavioral, financial, and operational data that would be impossible to manage manually.

The challenge has never been data availability. It has always been extracting value from it.

This is where AI and machine learning excel. By identifying hidden patterns across millions of data points, algorithms can detect anomalies, forecast risks, and automate decisions in real time. Instead of relying on static rules or human intuition alone, BFSI organizations can make faster, evidence-based decisions at scale.

As a result, AI has evolved from a back-office optimization tool into a strategic engine for innovation.

AI in Banking: From Fraud Detection to Hyper-Personalized Services

In the banking sector, AI adoption often begins with security and operational efficiency but quickly expands into customer experience.

Fraud detection is one of the earliest and most impactful use cases. Modern machine learning models continuously monitor transaction behavior and flag suspicious activities in real time. Unlike traditional rule-based systems, these models adapt dynamically as fraud tactics evolve, significantly reducing false positives while improving protection.

Beyond security, banks increasingly use AI to personalize services. By analyzing transaction histories, spending habits, and financial goals, intelligent systems can recommend relevant products such as credit cards, loans, or savings plans. This level of personalization not only increases conversion rates but also strengthens long-term customer loyalty.

AI-powered virtual assistants and chatbots further enhance the experience by providing 24/7 support, enabling customers to complete routine tasks instantly without visiting a branch or waiting in a queue.

For digital-first banks, these capabilities are no longer differentiators, they are baseline expectations.

AI in Financial Services: Smarter Risk and Investment Decisions

Across the broader financial services landscape, machine learning plays a critical role in risk modeling and investment optimization.

Lenders use predictive analytics to evaluate borrower behavior and estimate default probability with greater accuracy. Instead of relying solely on traditional credit scores, AI models incorporate alternative data sources, improving financial inclusion while reducing risk exposure.

Investment firms and asset managers apply advanced algorithms to analyze market signals, rebalance portfolios, and forecast trends. Robo-advisors, for example, automate wealth management services that were previously accessible only to high-net-worth clients, democratizing financial planning at scale.

By turning complex datasets into actionable insights, AI enables faster and more confident decision-making, a key competitive advantage in volatile markets.

AI in Insurance: Data-Driven Underwriting and Claims Automation

Traditionally, underwriting and claims processing were manual, document-heavy workflows that slowed customer service and increased costs. Today, insurers use machine learning and computer vision to automate large portions of these processes.

AI can assess risk profiles, estimate premiums, detect fraudulent claims, and even analyze damage through uploaded images or videos. Claims that once took days or weeks to process can now be resolved within minutes.

This automation improves both operational efficiency and customer satisfaction, two critical metrics in an industry where trust and responsiveness are paramount.

Intelligent Automation Across BFSI Operations

Financial institutions manage countless repetitive tasks such as document verification, compliance reporting, account reconciliation, and regulatory checks. Intelligent automation solutions combine AI with robotic process automation (RPA) to handle these workflows with minimal human intervention.

The result is lower operational costs, fewer errors, and faster processing times. More importantly, it allows employees to focus on higher-value strategic work rather than manual data entry. For large enterprises, even small efficiency gains can translate into millions of dollars in annual savings.

Emerging Technologies: Generative AI and the Next Frontier

Large language models are already being tested for drafting financial reports, summarizing contracts, automating customer communication, and assisting developers in building banking applications faster. Some insurers are experimenting with AI-generated claim summaries, while financial advisors are exploring conversational AI to simulate personalized guidance.

Although still early, these technologies signal how deeply AI will be embedded into everyday BFSI operations in the near future.

Challenges and Considerations for AI Adoption

Financial institutions must navigate strict regulatory requirements, data privacy concerns, and algorithmic fairness risks. Systems must be explainable, auditable, and compliant with evolving standards such as AML, KYC, and emerging AI governance regulations.

Security is equally critical. As AI models access sensitive financial data, robust cybersecurity and responsible AI practices become essential. For this reason, successful AI adoption often requires more than internal experimentation. It demands strong technical architecture, domain expertise, and experienced technology partners.

AI as a Strategic Imperative for the BFSI Domain

Ultimately, AI and machine learning are redefining what the BFSI domain represents. It is no longer simply a collection of financial institutions. It is a technology-driven ecosystem where data intelligence determines success.

Organizations that embrace AI can deliver faster services, reduce risks, and create highly personalized experiences at scale. Those that hesitate risk losing relevance to digital-native competitors and fintech disruptors.

For IT leaders, business executives, and investors evaluating opportunities in BFSI, one reality is clear: AI is not optional. It is the foundation of the industry’s future growth.

Ready to modernize your BFSI systems and accelerate digital transformation?

SmartDev helps banks, insurers, and fintech companies build secure, scalable platforms powered by cloud, AI, and automation.

Turn strategy into production-ready solutions with a trusted BFSI technology partner.

Talk to a BFSI ExpertTechnology and Digital Transformation in the BFSI Domain

While artificial intelligence often dominates the conversation, AI is only one part of a much broader modernization wave. To fully understand what is BFSI domain in today’s context, it is equally important to examine the wider technology ecosystem shaping the industry.

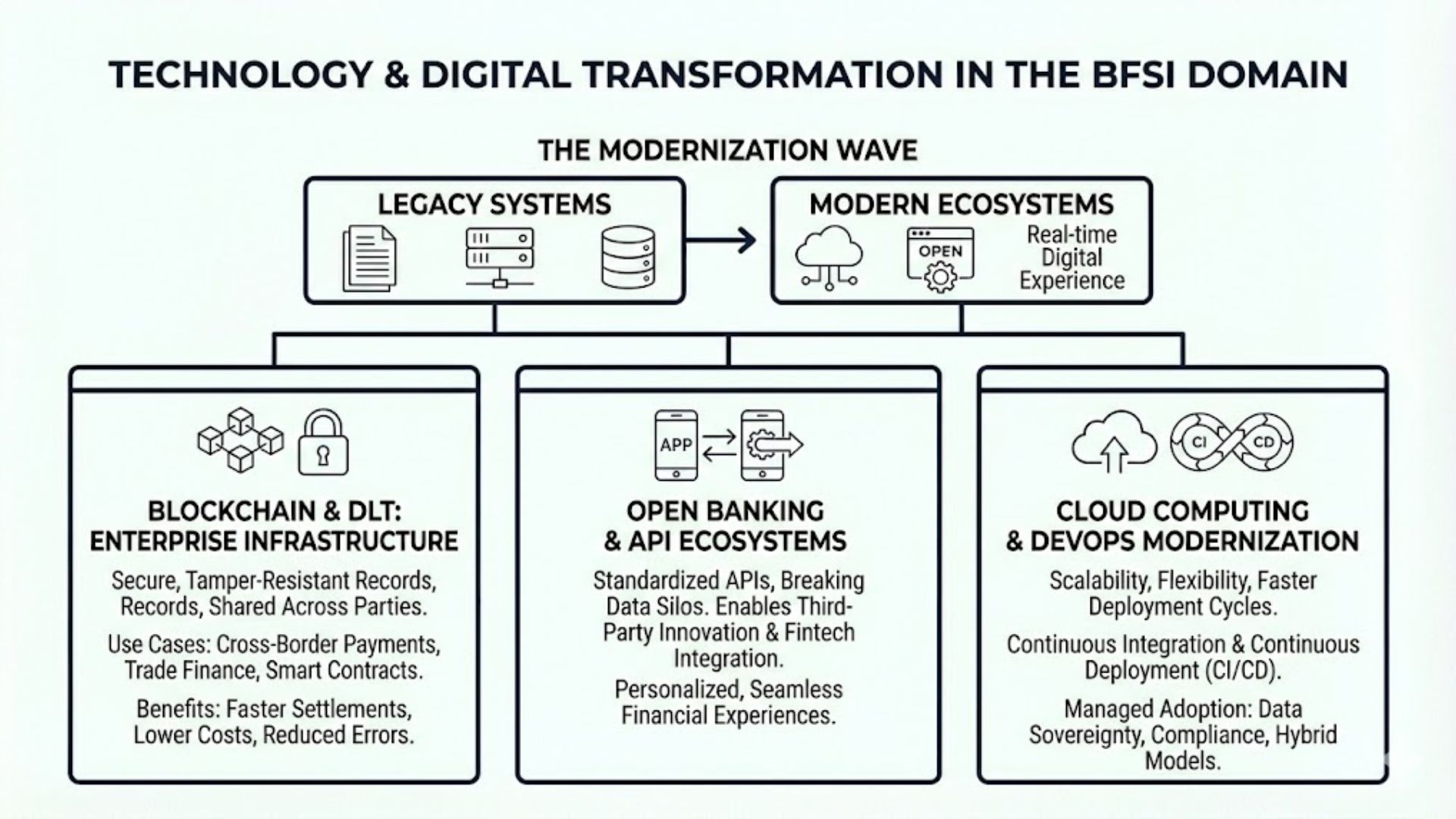

Banking, financial services, and insurance organizations are undergoing a large-scale digital transformation. Legacy core systems, paper-heavy processes, and siloed data infrastructures are steadily being replaced by cloud-native platforms, open ecosystems, and real-time digital experiences.

Blockchain and Distributed Ledger Technologies in BFSI

Blockchain has moved beyond its early association with cryptocurrencies and is increasingly being evaluated as enterprise infrastructure for financial services. For banks and insurers, trust, transparency, and data integrity are critical. Distributed ledger technologies provide exactly that secure, tamper-resistant records that can be shared across multiple parties without relying on a single centralized authority.

In practical terms, blockchain is being tested in areas such as cross-border payments, trade finance, smart contracts, identity verification, and claims processing. These use cases aim to reduce settlement times, minimize reconciliation errors, and lower operational costs.

For example, international money transfers that traditionally take days can potentially be settled in minutes through blockchain-based systems. Insurance claims involving multiple stakeholders can be automated through smart contracts, increasing speed and reducing disputes.

Although adoption is still evolving, the long-term potential is significant. Many analysts view blockchain as a foundational layer for the next generation of financial infrastructure.

Open Banking and API-Driven Ecosystems

In many regions, regulators now require banks to securely share customer-permissioned data through standardized APIs. This shift breaks down traditional data silos and enables third-party providers to build new services on top of existing financial platforms.

The result is a more connected and competitive ecosystem. Fintech startups can create budgeting apps, lending platforms, or payment tools that integrate directly with bank accounts. Customers benefit from more personalized and seamless financial experiences, while institutions gain access to new partnership opportunities.

Rather than operating as isolated entities, banks and insurers are increasingly becoming platforms within broader digital ecosystems. For BFSI organizations, success now depends on how well they can collaborate, integrate, and innovate with external partners not just how strong their internal systems are.

Cloud Computing and DevOps Modernization

Historically, many financial institutions relied on on-premise legacy infrastructure that was expensive to maintain and slow to adapt. Scaling new services or launching updates often required months of preparation.

By migrating to cloud-native architectures, BFSI firms gain scalability, flexibility, and faster deployment cycles. They can process massive volumes of transaction data, run advanced analytics, and launch new digital products more quickly than ever before.

DevOps practices further accelerate this progress. Continuous integration and continuous deployment (CI/CD) pipelines allow teams to release updates frequently while maintaining reliability and security. For innovation-driven BFSI organizations, this agility is critical. The ability to experiment, iterate, and scale rapidly often determines who leads the market.

That said, cloud adoption must be carefully managed. Data sovereignty, regulatory compliance, and cybersecurity remain top priorities, which is why many institutions adopt hybrid or private cloud models to balance flexibility with control.

Mobile Banking and Digital Payment Experiences

Today’s users expect financial services to be instant, mobile, and frictionless. Visiting a branch or filling out paper forms feels outdated when everything else in life happens through smartphones. This behavior has fueled explosive growth in mobile banking, digital wallets, and contactless payments.

From remote check deposits and biometric authentication to peer-to-peer transfers and QR-based payments, mobile technology is redefining how people interact with money. Fintech platforms and digital-first challengers have set new standards for simplicity and speed, forcing traditional institutions to modernize quickly.

In response, many banks and insurers are redesigning their services with a digital-first mindset, prioritizing intuitive interfaces and seamless customer journeys. Increasingly, the BFSI experience is not about physical locations, it is about digital touchpoints.

A Continuous Cycle of Innovation

The BFSI domain is no longer defined solely by financial products. It is defined by technological capability. Blockchain enhances trust and transparency. APIs enable ecosystem collaboration. Cloud and DevOps accelerate delivery. Mobile platforms redefine customer experience. AI powers intelligence and automation. Each layer reinforces the others, creating a continuous cycle of innovation.

For decision-makers, this means digital transformation is not a one-time project. It is an ongoing strategic commitment. Organizations that fail to modernize risk being outpaced by more agile competitors, while those that invest early can unlock significant efficiency gains and new revenue opportunities.

The Importance of BFSI Domain Knowledge

Understanding what is BFSI domain is not just useful for executives or strategists. It is essential for the engineers, analysts, and consultants building the systems behind the scenes.

Financial services are highly specialized and heavily regulated. Terms such as SWIFT messaging, Basel III compliance, underwriting workflows, KYC/AML checks, or claims adjudication are not just jargon — they represent real operational requirements that directly impact software design. Without this knowledge, even technically sound solutions can fail to meet business or regulatory needs.

For example, a payment platform must comply with strict security standards. A lending system must reflect complex credit risk models. An insurance application must align with policy rules and legal obligations. These nuances cannot be addressed through generic technology approaches alone.

That is why BFSI domain knowledge is often considered mandatory for IT professionals working in this sector. Developers, business analysts, testers, and architects must understand both technology and finance to deliver effective solutions.

In practice, this means learning:

- Financial products such as loans, accounts, policies, and investment instruments

- Core processes like onboarding, lending, underwriting, and claims management

- Compliance frameworks and regulatory constraints

- Customer behavior within financial ecosystems

This combination of technical and domain expertise enables teams to build systems that are not only functional but also compliant, secure, and aligned with real business outcomes. And for technology partners serving BFSI clients, deep domain knowledge becomes a key differentiator.

Why SmartDev: Your Educational Entry Point to the BFSI Domain

The bigger challenge for most organizations lies in execution, translating industry knowledge, regulatory requirements, and emerging technologies into secure, scalable software solutions that work in real business environments.

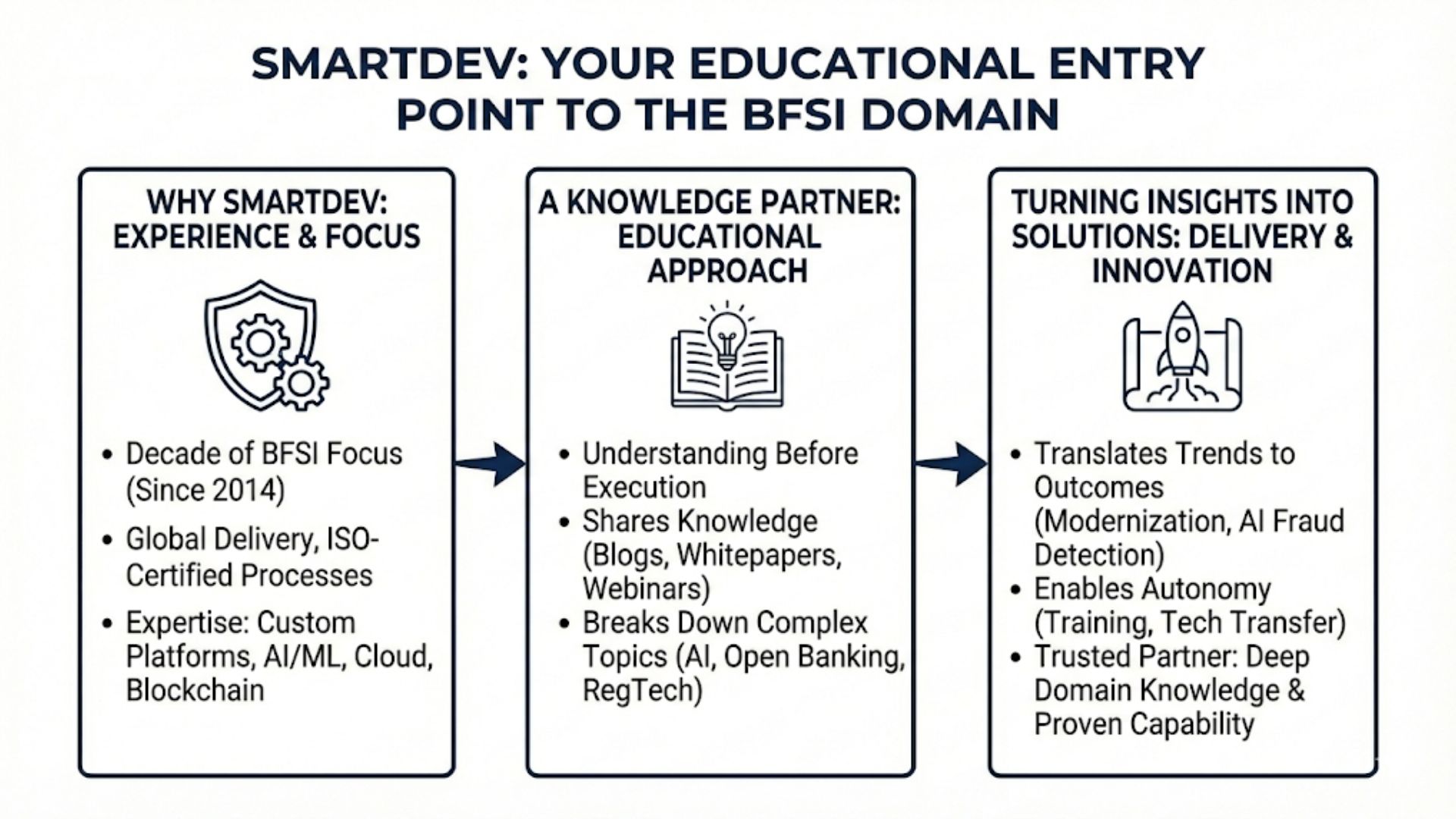

At SmartDev, we have spent more than a decade working exclusively at the intersection of BFSI and technology, helping banks, financial service providers, and fintech innovators turn ideas into production-ready systems. Since our founding in 2014, BFSI has not simply been one of many verticals for us. It has been a core focus.

Our early engagements included building applications for a major Swiss credit card issuer and an airline-owned fintech startup, where reliability, security, and compliance were non-negotiable. These projects shaped our DNA, teaching us that financial software must meet not only functional requirements but also strict regulatory and risk standards.

Today, SmartDev operates globally with delivery teams across multiple continents, supporting clients with:

- Custom banking and fintech platforms

- AI and machine learning solutions

- Mobile and digital payment applications

- Cloud-native modernization

- Blockchain and emerging technology consulting

All delivered through ISO-certified processes and Agile methodologies designed specifically for high-security industries like BFSI.

More Than a Vendor – A Knowledge Partner

What differentiates SmartDev, however, goes beyond technical capability. We believe that successful digital transformation starts with understanding.

Many BFSI organizations know they need AI, cloud, or automation but are unsure where to begin. Technology can feel overwhelming without clear guidance on business impact, regulatory implications, or implementation strategy. That’s why we position ourselves as an educational entry point, not just a development vendor. In practice, this means we actively share knowledge before selling solutions.

Through research-driven blogs, whitepapers, webinars, and workshops, we break down complex topics such as AI in insurance, open banking architecture, regulatory technology, and fintech trends into practical insights. Our goal is to help decision-makers build clarity and confidence long before the first line of code is written.

By explaining concepts like what is BFSI domain, industry trends, and technology transformation, we aim to equip businesses with the context they need to make smarter strategic decisions.

Turning BFSI Insights into Real-World Solutions

Once the strategy is clear, SmartDev helps organizations translate BFSI trends into tangible outcomes. Whether it’s modernizing a legacy core system, launching a secure mobile banking application, implementing AI-driven fraud detection, or building an end-to-end digital lending platform, our teams combine domain understanding with engineering expertise to deliver production-ready solutions.

We provide training, documentation, and technology transfer to ensure that solutions are sustainable long after deployment. Instead of creating dependency, we enable autonomy — empowering organizations to confidently manage and scale their own systems.

A Trusted Partner for BFSI Innovation

Over the years, SmartDev has been recognized as one of Vietnam’s leading technology companies, earning multiple certifications and industry awards for quality and delivery excellence. But beyond accolades, what truly defines us is our long-term commitment to BFSI innovation.

We understand the regulatory pressures, the security expectations, and the pace of change within the financial services world. That domain familiarity allows us to anticipate challenges and design solutions that are both compliant and future-ready. For banks, insurers, fintech startups, and financial enterprises seeking a reliable transformation partner, SmartDev offers a rare combination of:

- Deep BFSI knowledge

- Proven engineering capability

- A consultative, education-first approach

Conclusion: Understanding What Is BFSI Domain in a Technology-Driven Era

The BFSI domain: spanning banking, financial services, and insurance sits at the core of the global economy. Today, it is no longer defined solely by financial products, but by technology-driven innovation.

From AI and machine learning to cloud, blockchain, and digital platforms, modern BFSI organizations must continuously evolve to stay competitive, secure, and customer-centric. Understanding what is BFSI domain therefore means understanding how finance and technology work together to create smarter, faster, and more resilient services.

For businesses entering or modernizing within this space, domain knowledge and the right technology strategy are equally essential. At SmartDev, we combine both: acting as an educational entry point and a trusted technology partner to help BFSI organizations turn digital transformation into measurable results.