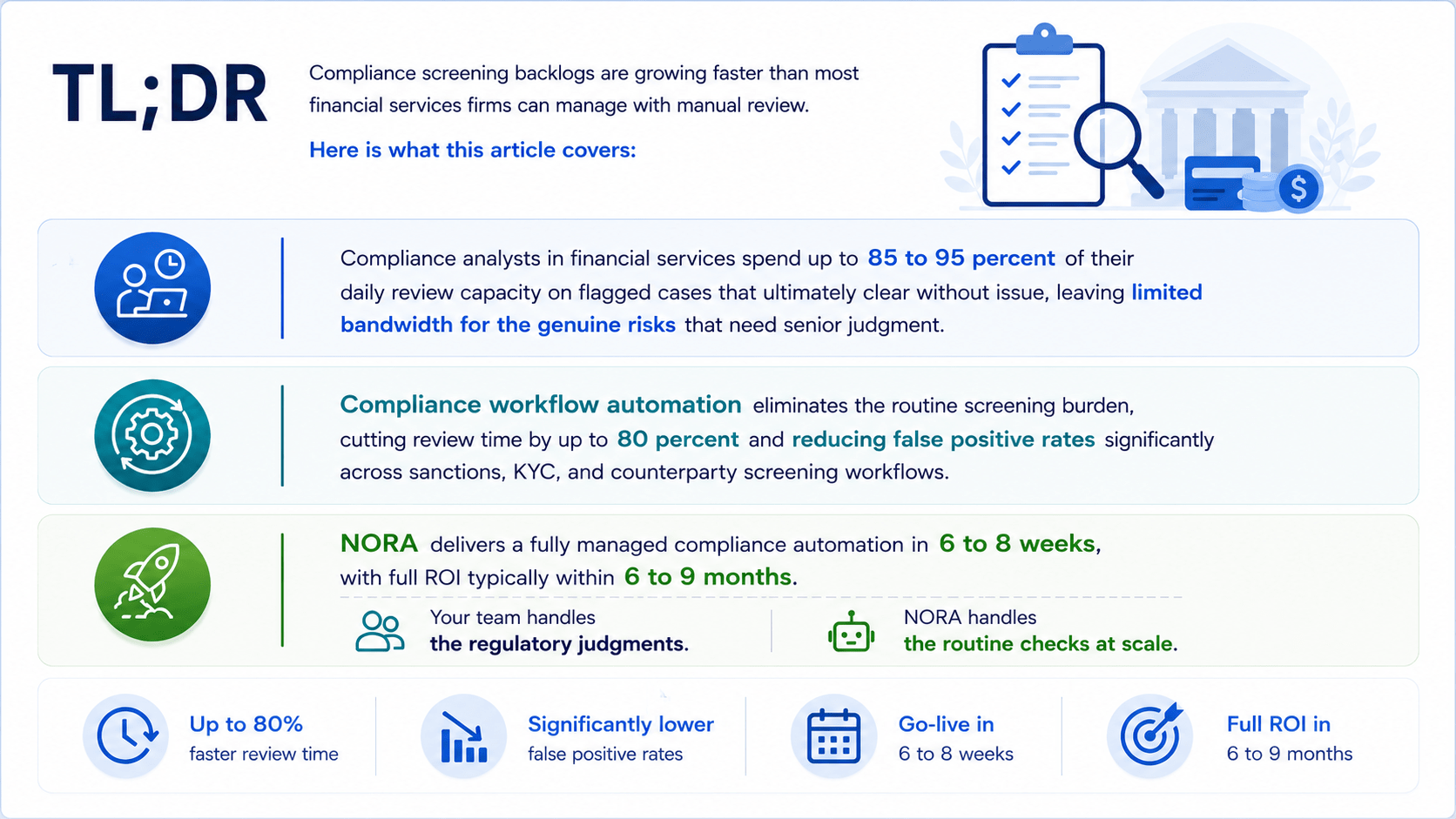

TL;DR

Compliance screening backlogs are growing faster than most financial services firms can manage with manual review. Here is what this article covers:

- Compliance analysts in financial services spend up to 85 to 95 percent of their daily review capacity on flagged cases that ultimately clear without issue, leaving limited bandwidth for the genuine risks that need senior judgment.

- Compliance workflow automation eliminates the routine screening burden, cutting review time by up to 80 percent and reducing false positive rates significantly across sanctions, KYC, and counterparty screening workflows.

- SmartDev’s NORA delivers a fully managed compliance automation in 6 to 8 weeks, with full ROI typically within 6 to 9 months. Your team handles the regulatory judgments. NORA handles the routine checks at scale.

Introduction

Compliance workflow automation is not a future investment for most financial services firms. It is an urgent fix for a process that has not changed in a decade. A reviewer opens a document manually. They check it against a sanctions list. They flag a potential match and pass it to a colleague. That colleague reviews the same document, applies their own judgment, and either escalates or clears the case. By the time that chain completes, hours have passed. The backlog has grown. The next batch is already waiting.

The problem is structural, not operational. When every document requires a human touch from start to finish, your compliance capacity is capped by headcount. Adding more reviewers helps in the short term. However, it does not fix the underlying design flaw: a process built for low volume that now runs at high scale. Compliance workflow automation fixes the design. This guide explains how it works, why manual review fails at scale, and how one financial services firm cut its review time by 80 percent in the first quarter of deployment.

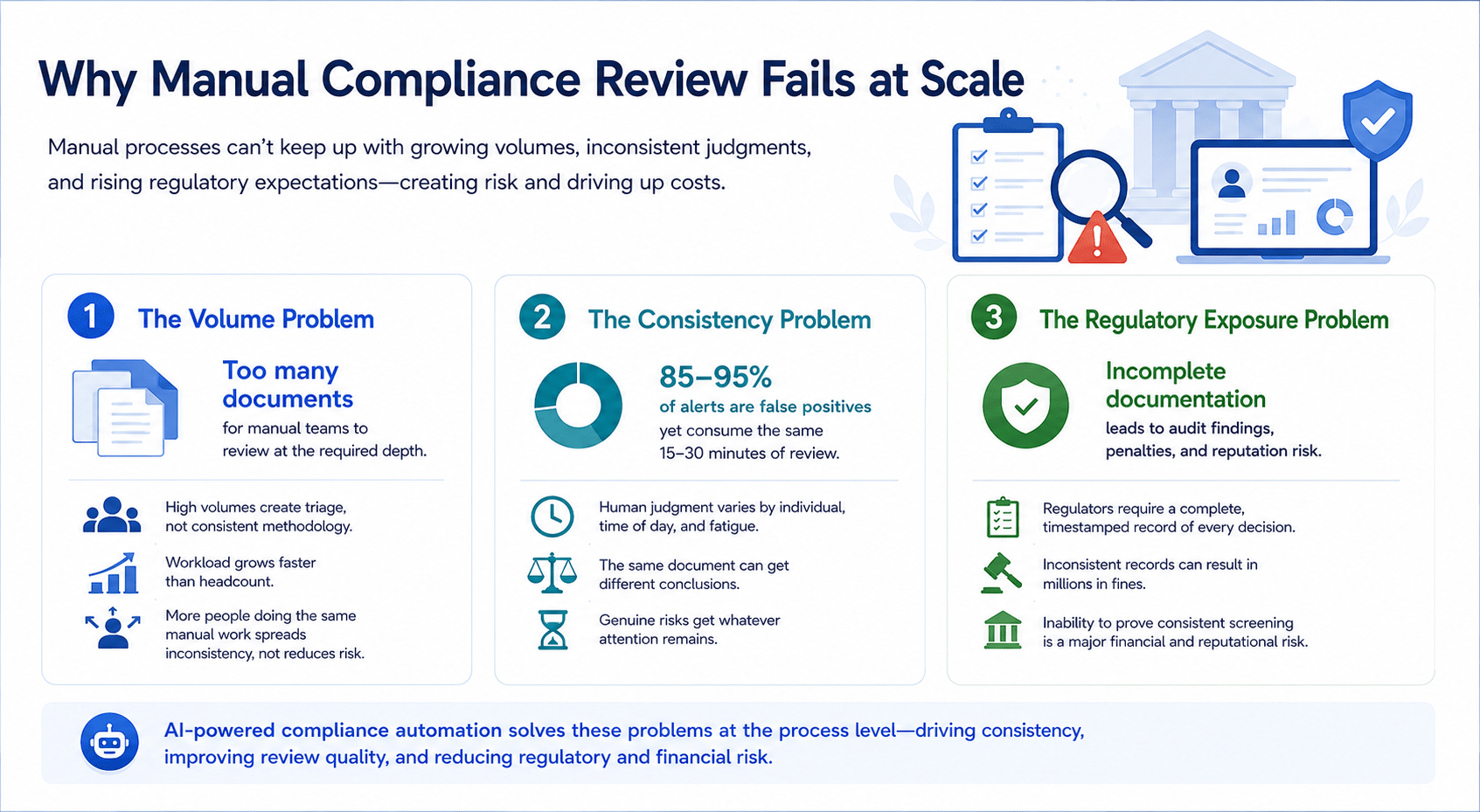

Why Manual Compliance Review Fails at Scale

1. The Volume Problem

Manual compliance review made practical sense when transaction volumes were lower. A team of three or four reviewers could work through a daily document queue with reasonable thoroughness. However, as financial services firms grow in transaction volume, geographic reach, and counterparty complexity, that model breaks down quickly.

Consider a mid-market asset management firm screening 150 to 200 counterparty documents per day. Those documents span sanctions databases, PEP registries, and adverse media sources. Research on automated KYC and AML monitoring shows that firms at this volume routinely face a triage problem. There are simply too many documents arriving for a manual team to assess each one at the required depth. In practice, reviewers apply a triage instinct rather than a consistent methodology. Some documents receive close attention. Others move through quickly. The gap between those two categories is where regulatory exposure accumulates, day after day.

The volume problem compounds over time. As your firm adds counterparties and expands into new markets, the compliance workload grows faster than headcount. Most firms respond by adding reviewers rather than improving the underlying workflow. However, more people doing the same manual work does not reduce risk. It distributes the same inconsistency across more individuals. Each person applies their own interpretation of the same regulatory requirements. AI workflow automation addresses this at the process level, not the headcount level, which is the only intervention that actually scales.

2. The Consistency Problem

Even when compliance teams have enough time, human review is inconsistent. Reviewer judgment varies by individual and by time of day. Attention degrades over the course of a long review session. The same document reviewed by two experienced analysts can receive different conclusions. Neither is wrong. Manual review simply does not enforce a uniform standard across every case.

False positive rates make this problem measurable. According to Facctum’s AML False Positive Report, AML false positive rates typically range between 85 and 95 percent. That means the vast majority of compliance alerts do not represent genuine risk. Each false positive consumes the same 15 to 30 minutes of review time as a genuine hit. Consequently, daily capacity is absorbed by cases that do not represent real risk. The cases that do receive whatever attention remains at the end of a depleted queue.

According to Thomson Reuters’ annual Cost of Compliance report, compliance functions consistently identify manual screening as the single largest driver of compliance operating costs. Teams also report increasing difficulty maintaining review quality as volume grows. Human fatigue is a well-documented factor in that equation. Research on sustained attention shows that accuracy degrades after prolonged screening sessions. This pattern, known as the vigilance decrement, means an analyst reviewing their fiftieth document catches fewer signals than the same analyst reviewing their tenth. That degradation is not a performance failing. It is a predictable consequence of a high-volume process built around human attention spans.

3. The Regulatory Exposure Problem

Regulatory expectations for compliance documentation have intensified significantly in recent years. Auditors and regulators no longer accept a general assurance that documents were reviewed and cleared. They want a complete, timestamped record of every screening decision: what was checked, what was found, who reviewed it, and what determination was made. Manual compliance processes rarely produce documentation at that level of consistency.

When a firm relies on individual reviewers to document their own decisions, the quality of that documentation varies with each reviewer. One analyst writes detailed review notes. Another records only the final outcome. A third uses shorthand that is difficult to interpret during an audit six months later. As a result, the audit trail regulators request rarely matches the standard they require when they examine it closely.

The financial consequences of documentation failures are not theoretical. Regulatory penalties for inadequate compliance processes have reached millions of dollars across multiple jurisdictions. These penalties often arise not from a failure to screen, but from an inability to demonstrate that screening met a consistent and documented standard. Therefore, the risk is not only operational. It is reputational and financial in ways that dwarf the cost of the process itself. AI use cases in financial services increasingly address this documentation gap directly, treating a complete audit trail as a core workflow output, not an afterthought.

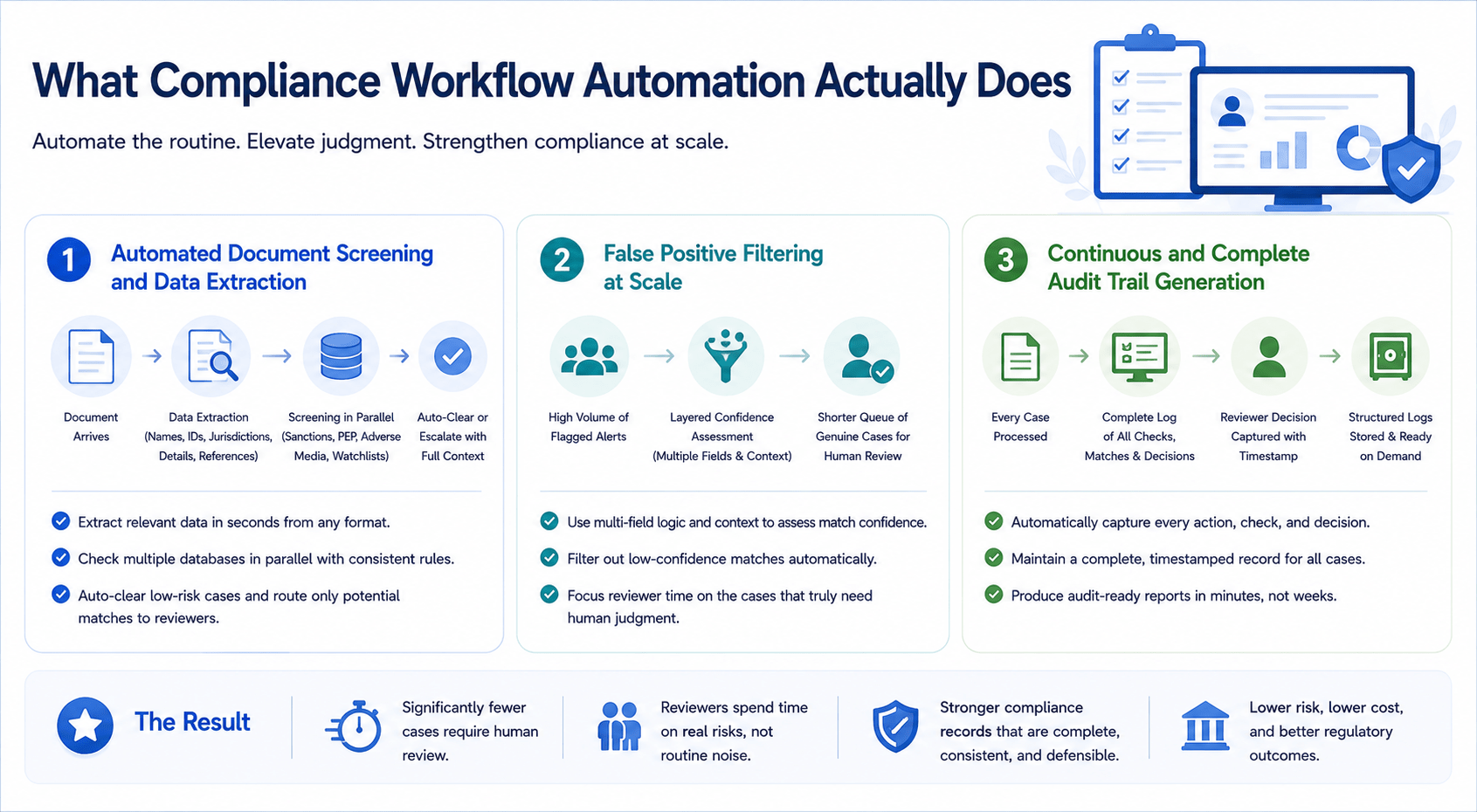

What Compliance Workflow Automation Actually Does

1. Automated Document Screening and Data Extraction

Compliance workflow automation begins at the point of document arrival. When a counterparty document reaches the system, the automated workflow reads it immediately. It extracts the relevant fields without manual input, regardless of whether the document arrived by email, upload, or platform integration. Names, entity identifiers, jurisdictions, registration details, and transaction references are pulled from the document in seconds.

Those extracted fields are screened automatically against the relevant databases. Sanctions lists, PEP registries, adverse media sources, and internal policy blacklists are checked in parallel, not sequentially. The screening logic applies the same rules and thresholds to every document, every time. A reviewer with eight years of experience and a reviewer who joined last month do not introduce different standards to the same case type. The system applies one standard, consistently, at scale.

The practical result is a significant reduction in documents requiring human review. Clear passes move forward automatically, with a complete log of every check performed. Potential matches are routed to a human reviewer with context pre-assembled. That includes the extracted field that triggered the match, the database entry it matched, and the confidence level the system assigned. AI-powered document intake and data processing makes this kind of structured, consistent extraction possible at the volume financial services compliance now requires.

2. False Positive Filtering at Scale

False positives are one of the most expensive operational problems in AML compliance screening, and they are also one of the most solvable. A name match that looks significant on first pass turns out to be a different entity with a similar name. A jurisdiction flag proves irrelevant when the transaction context is examined. Each of these cases consumes reviewer time and delays onboarding or transaction approval, without adding compliance value.

Compliance workflow automation reduces false positives through layered screening logic. Rather than flagging any partial match immediately, the system applies a structured confidence assessment. It cross-references multiple fields simultaneously: name variants, entity type, jurisdiction, registration number, and date of listing. It checks whether differentiating factors, such as date of birth or business category, clearly distinguish the counterparty from the listed entity. Low-confidence matches with clear distinguishing characteristics are filtered out before they reach the review queue.

In practice, this upstream filtering changes what compliance teams spend their time on. A team that previously reviewed 80 to 100 flagged cases per day may find their queue contracts to 15 to 25 genuinely ambiguous cases. As a result, each case receives more thorough attention. Reviewers are no longer managing volume. They are applying judgment where judgment actually adds value. The quality of compliance decisions improves not despite automation, but because of it. AI workflow automation in business processes consistently produces this upstream filtering benefit across screening-intensive financial services workflows.

3. Continuous and Complete Audit Trail Generation

One of the most operationally valuable outputs of compliance workflow automation is the audit trail it generates automatically. Every document that enters the system produces a log. That log records what fields were extracted, which databases were checked, what matches were identified, and what confidence assessment was applied. It also records whether the case was auto-cleared or escalated to a human reviewer.

For cases that reach a human reviewer, the log extends further. It captures who reviewed the case and when. It records what supporting information was presented to them and what decision they recorded. That record is timestamped, linked to the original document, and stored in a structured format that is immediately retrievable on demand. Your compliance function no longer reconstructs its decision history from email threads and shared spreadsheets when an auditor makes a request. The documentation exists automatically for every case processed since the system went live.

This audit trail capability directly addresses persistent regulatory concerns. When an auditor requests evidence of compliance screening for a specific counterparty or time period, the system produces a complete and structured report within minutes. Moreover, the consistency of the log across thousands of decisions makes the evidence far more defensible than documentation produced by multiple individuals at varying levels of thoroughness. In that case, the value of automation extends well beyond speed. It is the quality, completeness, and defensibility of the compliance record your firm can produce when regulators ask for it.

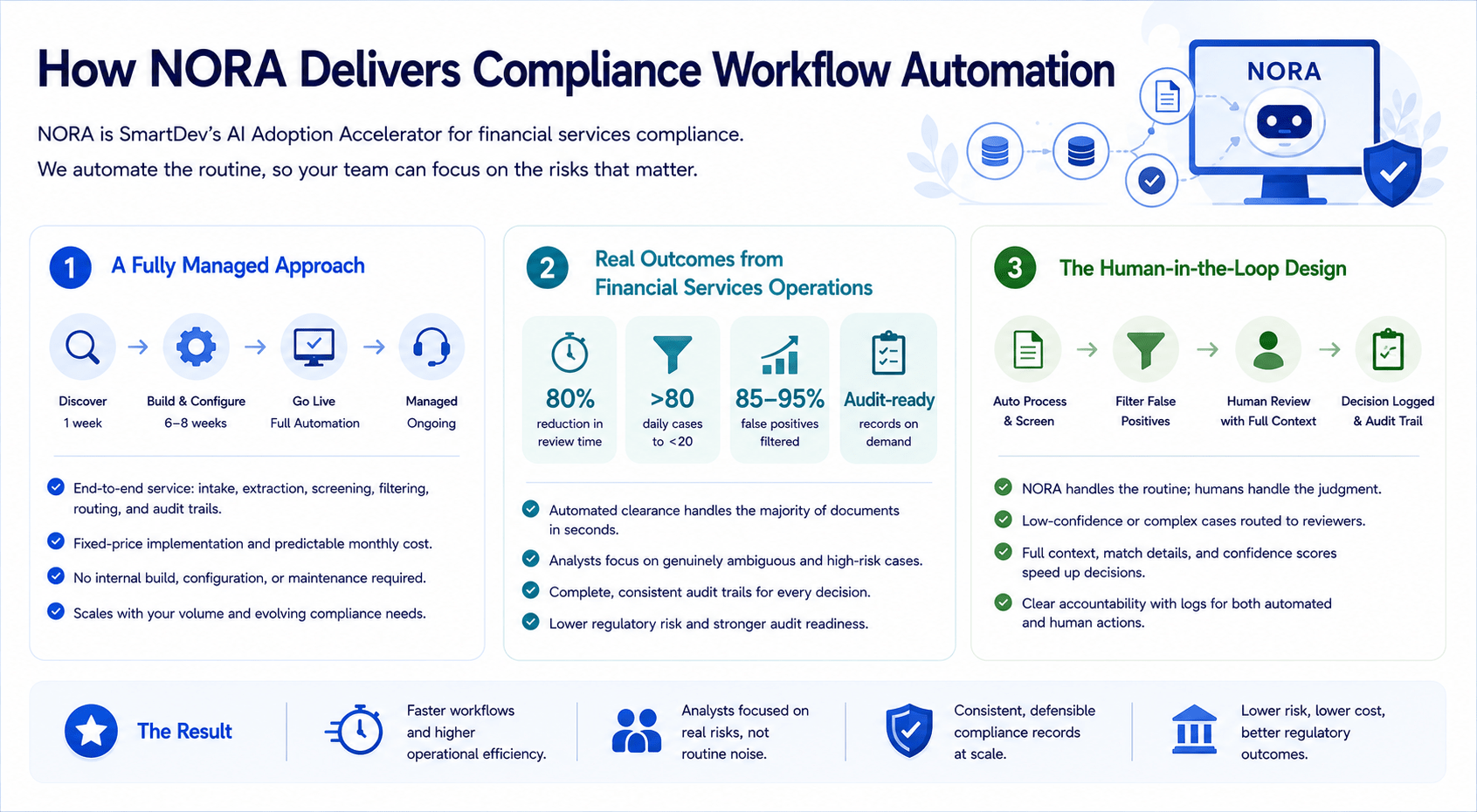

How NORA Delivers Compliance Workflow Automation

1. A Fully Managed Approach

NORA is SmartDev’s AI Adoption Accelerator. It is a fully managed service that designs, builds, and continuously operates compliance workflow automation for financial services firms. For compliance screening specifically, NORA handles document intake, field extraction, multi-database screening, false positive filtering, exception routing, and audit trail generation as a single integrated workflow. Your team does not need to build, configure, or maintain any of it internally.

The implementation starts with a one-week structured discovery phase. SmartDev maps your current compliance screening process in detail. That includes the document types you receive, the databases you screen against, the rules that govern escalation, and the integration requirements for your existing onboarding systems. From that foundation, SmartDev produces a fixed-price implementation proposal. There is no commitment required beyond the discovery phase itself. The 3-week AI discovery program is also available for compliance teams that want a broader assessment of their automation readiness before committing to a specific scope.

After the discovery phase, the first working compliance automation is delivered in 6 to 8 weeks. In practice, NORA processes every incoming document automatically. It filters false positives and routes genuine matches to a human review queue with all supporting context assembled. Your compliance team focuses on the cases that actually require their judgment. NORA handles the routine screening at scale. The pricing model covers both setup and ongoing managed service at a fixed monthly cost. Your compliance budget stays predictable regardless of how document volume changes month to month.

2. Real Outcomes from Financial Services Operations

One financial services firm was processing counterparty screening requests daily across sanctions, PEP, and adverse media databases. Each event required 10 to 15 minutes of manual analyst time from start to finish. Before automation, the compliance team spent the majority of each working day on routine document review. Consistent with industry benchmarks, approximately 85 to 95 percent of the daily review queue consisted of false positives that cleared after investigation. Senior analysts had limited capacity remaining for the complex cases that genuinely required their experience.

After implementing compliance workflow automation, review time dropped by 80 percent. Automated clearance handled the majority of incoming documents within seconds. The human review queue contracted from more than 80 cases per day to fewer than 20 genuinely ambiguous cases. Consequently, each case that reached a reviewer arrived with full context pre-assembled. That included the specific field that triggered the escalation, the database entry, the confidence assessment applied, and the relevant regulatory reference. Analysts spent less time assembling information and more time making informed decisions.

The compliance team also reported a marked improvement in audit readiness after deployment. According to EQS Group’s overview of the compliance officer role, compliance officers, analysts, and operations leads each carry distinct documentation responsibilities. The CCO is accountable for the overall programme. Analysts own case-level decision records. Operations leads manage escalation trails. Automation gave each layer a consistent, structured record to work from. When regulators requested evidence of screening decisions, the system produced a complete record on demand. That capability had previously required hours of manual reconstruction across email threads and spreadsheets. Additionally, consistent screening logic reduced the firm’s exposure to regulatory findings based on uneven review standards.

3. The Human-in-the-Loop Design

NORA in Financial Compliance does not replace human judgment in the compliance screening process. It removes human effort from the parts of the process that do not require judgment: reading documents, extracting fields, running database checks, filtering false positives, and routing cases. Genuine matches and ambiguous edge cases go to a human reviewer with full context attached. Your team makes an informed decision in minutes, rather than spending 15 minutes assembling the evidence themselves.

This design directly addresses the concern most compliance leaders raise when evaluating automation for regulated workflows. What happens when the system encounters something it cannot handle confidently? With NORA, the answer is clear. When the system encounters a document it cannot assess with high confidence, it does not auto-clear or auto-reject. It routes the case to a human reviewer. It flags exactly what triggered the uncertainty: the specific field that matched, the database record involved, and the confidence score assigned. The reviewer has everything they need to make a well-documented decision.

Beyond exception handling, the human-in-the-loop model produces something equally valuable from a regulatory standpoint: a clear and verifiable accountability structure. Every automated clearance carries a log of the rules applied. Every escalated case carries a log of the human decision made and by whom. Together, those logs form a compliance record that is complete, consistent, and structured in a way that manual processes cannot replicate at scale. SmartDev’s AI and machine learning solutions are built around this principle: automation handles the predictable, humans handle the judgment, and the audit trail covers both.

The Business Case for Compliance Workflow Automation

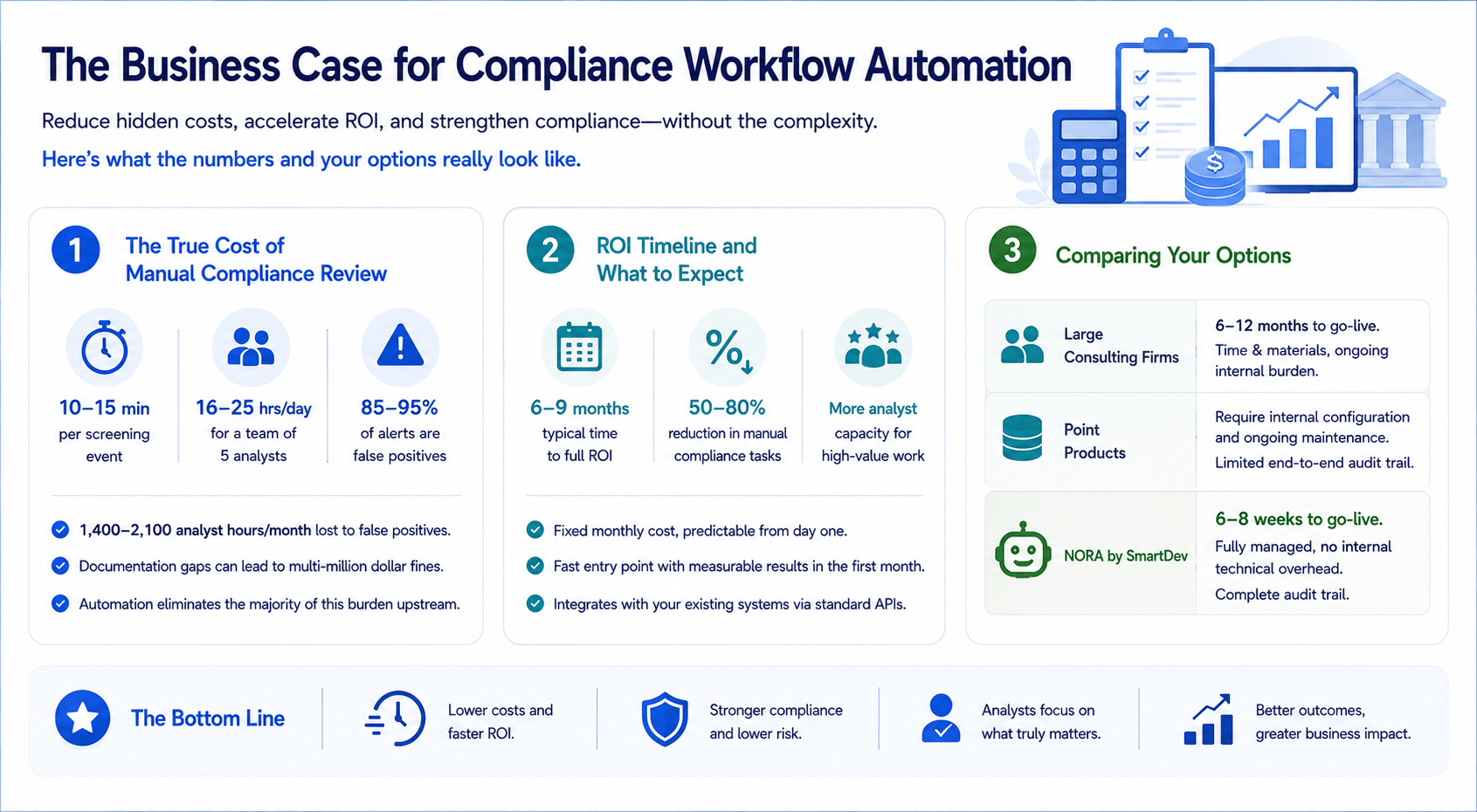

1. The True Cost of Manual Compliance Review

The direct cost of manual compliance screening is easy to underestimate. It appears as staff time rather than a discrete line item. However, when you account for the time spent per screening event, the fully loaded staff cost, the time spent on false positives, and the regulatory risk carried by documentation gaps, the true operational cost is significantly higher than most compliance budgets acknowledge.

A compliance analyst spending 10 to 15 minutes per screening event across a daily queue of 100 documents is committing 16 to 25 hours per day to routine screening work. For a team of five analysts, that represents most of the team’s available capacity. The cost of a single regulatory finding related to documentation failures can exceed the annual cost of a fully managed compliance automation deployment by a substantial margin. The operational cost and the regulatory risk are two separate arguments for automation, and each is compelling on its own terms.

False positives add a layer of compounding inefficiency that most compliance cost analyses undercount. At a typical initial flagging rate of 50 to 60 percent across 150 to 200 daily counterparty submissions, a compliance team can expect 80 to 110 flagged cases per day. With false positive rates running between 85 and 95 percent according to the Facctum AML False Positive Report, 68 to 104 of those cases are non-issues consuming real analyst hours. Over a working month, that amounts to between 1,400 and 2,100 analyst hours consumed by false positive management alone. Compliance workflow automation eliminates the majority of that burden before it reaches the review queue.

2. ROI Timeline and What to Expect

NORA implementations in financial services compliance typically reach full ROI within 6 to 9 months. The fixed setup fee and monthly managed service model means costs are predictable from the first day of deployment. There are no variable consulting hours, no internal development costs, and no per-seat licensing fees that scale unexpectedly as screening volume grows.

For compliance functions evaluating where to start with automation, screening and document review workflows are among the strongest entry points. The inputs are structured, the validation rules are well-defined, and the reduction in reviewer burden is measurable from the first month of operation. Unlike broader AI transformation initiatives, compliance workflow automation does not require a complete overhaul of existing systems. It integrates with your current compliance databases, onboarding platforms, and case management tools via standard APIs.

Manual compliance tasks across screening, documentation, and exception management are generally reduced by 50 to 80 percent, depending on current workflow complexity and document volume. This range is consistent with AI-assisted compliance deployments in financial services. The Thomson Reuters Cost of Compliance report documents that firms adopting structured automation report significant reductions in per-review handling time and documentation overhead. That reduction translates directly into analyst capacity. Your compliance team does not shrink. Instead, their time shifts from routine data processing to analytical work that actually requires their expertise.

3. Comparing Your Options

Large consulting firms, including Deloitte, PwC, Accenture, and McKinsey, offer AI transformation programmes for financial services compliance. These programmes typically take 6 to 12 months to reach production. They are delivered on a time-and-materials basis, meaning costs are open-ended throughout the engagement. Their own published frameworks confirm that discovery, design, build, and testing phases for enterprise compliance automation routinely span two to four quarters before any live workflow is operational. Furthermore, the deliverable at the end is often a custom build that your internal team must then operate and maintain without the consultancy’s ongoing support.

Point products for compliance screening, such as ComplyAdvantage, Refinitiv World-Check, and Dow Jones Risk and Compliance, provide database access and initial screening capability. However, they require your team to configure screening rules, maintain database integrations, and update sanction lists and adverse media feeds manually over time. Their own documentation acknowledges that ongoing rule maintenance and integration upkeep fall to the client’s internal team after implementation. That overhead is consistently underestimated during procurement. Moreover, point products rarely produce end-to-end audit trails. They address one step in the compliance workflow, not the complete process from document arrival to decision record.

NORA delivers a working compliance workflow automation in 6 to 8 weeks, fully managed, with no internal technical overhead required. SmartDev maintains the screening logic, database integrations, and system performance as part of the ongoing service. Your team gains compliance capability without the infrastructure burden. SmartDev’s fintech and financial services industry page outlines the full range of automation opportunities available to mid-market firms in regulated industries.

Conclusion

Compliance backlogs are not a staffing problem. They are a process problem. And process problems do not resolve themselves as volume grows. They compound.

The financial services firms that continue to rely on manual compliance review are not failing because their teams lack expertise or diligence. They are operating within a process architecture designed for a lower volume, a simpler regulatory environment, and a narrower counterparty base. As all three of those conditions have changed, the gap between what manual review can reliably deliver and what regulators now expect has widened significantly. Adding headcount narrows that gap temporarily. Automating the process closes it permanently.

Compliance workflow automation processes every document consistently, screens against the required databases without variation, and filters out false positives before they consume analyst time. It generates a complete audit trail for every decision automatically. The result is faster throughput, lower operational cost, and a compliance function that is more defensible under regulatory scrutiny. For a deeper look at how SmartDev structures AI automation for regulated environments, SmartDev’s BFSI compliance framework covers the full implementation approach and what financial services teams can expect at each stage.

SmartDev’s NORA brings this capability to financial services operations as a fully managed service, with no internal technical overhead required. A working automation is delivered in 6 to 8 weeks. Full ROI is typically reached within 6 to 9 months. Your team handles the regulatory judgments. NORA handles everything else, from day one.

If you are ready to reduce your compliance review burden and build a more defensible screening process, contact SmartDev to discuss your specific requirements.