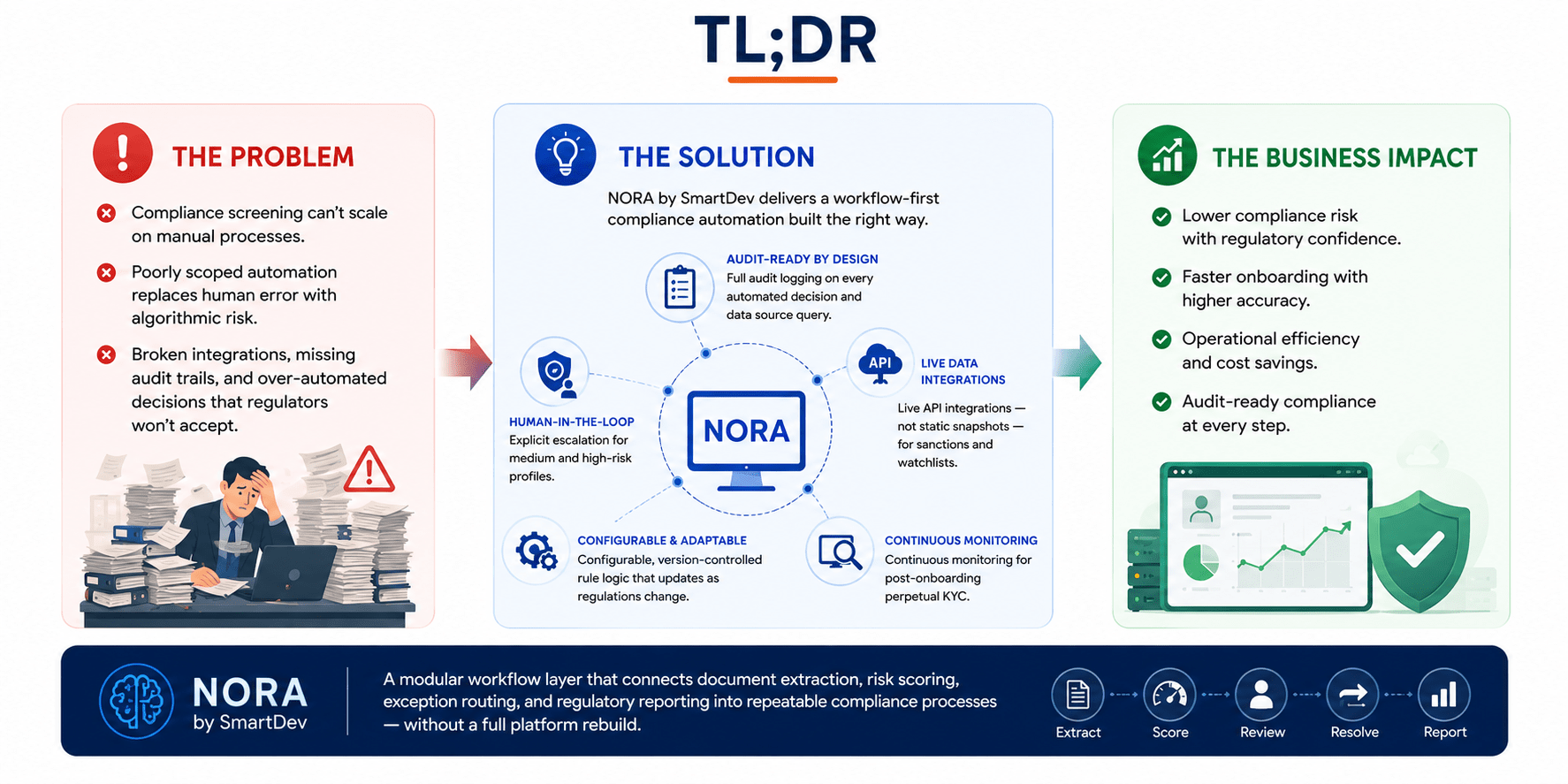

Compliance screening is breaking under the weight of scale, and the instinct to automate it is right. But automation without the right workflow architecture doesn’t eliminate risk; it just moves it somewhere harder to see. Here’s how to do it correctly.

TL; DR:

Compliance screening, KYC, AML, sanctions, PEP checks, cannot scale on manual processes alone. According to the FATF’s financial crime framework, the regulatory expectation for real-time, consistent screening has become a baseline requirement across all major jurisdictions, not an advanced capability. Automation workflow solves this, but only when built correctly. As SmartDev’s enterprise AI failure analysis documents, poorly scoped automation replaces human error with algorithmic risk: broken integrations, missing audit trails, and over-automated decisions that regulators, and the Basel Committee’s operational resilience principles, will not accept.

The safe path forward is a workflow-first model that connects AI-driven screening, configurable risk scoring, and human review into a single auditable process. Key requirements:

- Full audit logging on every automated decision and data source query

- Explicit human-in-the-loop escalation for medium and high-risk profiles

- Live API integrations, not static database snapshots, for sanctions and watchlist data

- Configurable, version-controlled rule logic that updates as regulations change

- Continuous monitoring for post-onboarding perpetual KYC

NORA by SmartDev delivers this as a modular workflow layer, connecting document extraction, risk scoring, exception routing, and regulatory reporting into repeatable compliance processes without requiring a full platform rebuild.

Introduction

Financial institutions and fintech platforms are under mounting pressure to screen every customer, transaction, and counterparty against growing regulatory requirements, sanctions lists, AML watchlists, PEP registries, and adverse media databases. These checks must be performed at a speed and scale that manual teams cannot sustain. According to FATF’s financial crime guidance, the global regulatory expectation is not slowing down, it is expanding in both scope and enforcement frequency. As a result, automation workflows are becoming the preferred solution for regulated businesses that need to maintain compliance without scaling headcount proportionally.

However, automation alone does not solve the compliance problem. If implemented carelessly, it simply relocates the risk. Instead of human error, organizations face algorithmic blind spots, broken integrations, and audit gaps that are harder to detect and more expensive to fix. As SmartDev’s analysis of enterprise AI project failure shows, the most common failure mode is not a flawed AI model; it is a fragmented implementation that leaves compliance gaps between automated steps.

This guide examines how well-designed automation workflows support compliance screening, connecting KYC verification, AML monitoring, sanctions screening, and human review into repeatable, auditable processes without introducing new operational risk. We also explore how NORA by SmartDev applies a workflow-first architecture to make compliance automation production ready for regulated businesses.

The Compliance Screening Problem in 2026

Compliance screening has never been more consequential, or more expensive. Today, financial institutions, fintech platforms, and regulated businesses face increasing scrutiny across every major jurisdiction. As a result, they must screen customers against sanctions lists, PEP (Politically Exposed Persons) databases, adverse media sources, and AML watchlists, both before and after onboarding. Meanwhile, screening volumes have surged alongside digital growth. However, many teams still rely on manually intensive processes that were designed for a much smaller era. According to LexisNexis Risk Solutions’ True Cost of AML Compliance report, global AML compliance costs have risen sharply year-on-year, with financial institutions in the US and Europe collectively spending hundreds of billions annually on compliance-related headcount and processes.

According to McKinsey’s financial services benchmarks, many institutions allocate 10–15% of their full-time workforce solely to KYC and AML tasks. At scale, this model doesn’t just slow down onboarding; it introduces inconsistency, delays, and a false sense of security. The Wolfsberg Group’s AML principles make clear that the adequacy of a compliance program is judged not just by its intent but by its operational consistency, precisely what manual workflows cannot guarantee at scale. At the same time, institutions that rush into compliance automation without proper safeguards face a different threat: automating poorly designed workflows create new operational risk rather than eliminating old ones.

The central question for compliance leaders in 2026 is not whether to automate, it’s how to automate compliance screening without creating the very risk it’s meant to prevent. As SmartDev’s risk management guide outlines, the answer lies in a workflow-first approach that connects AI capabilities into governed, auditable processes rather than deploying them as isolated point tools.

What Is Compliance Screening, and Why It Breaks Under Scale

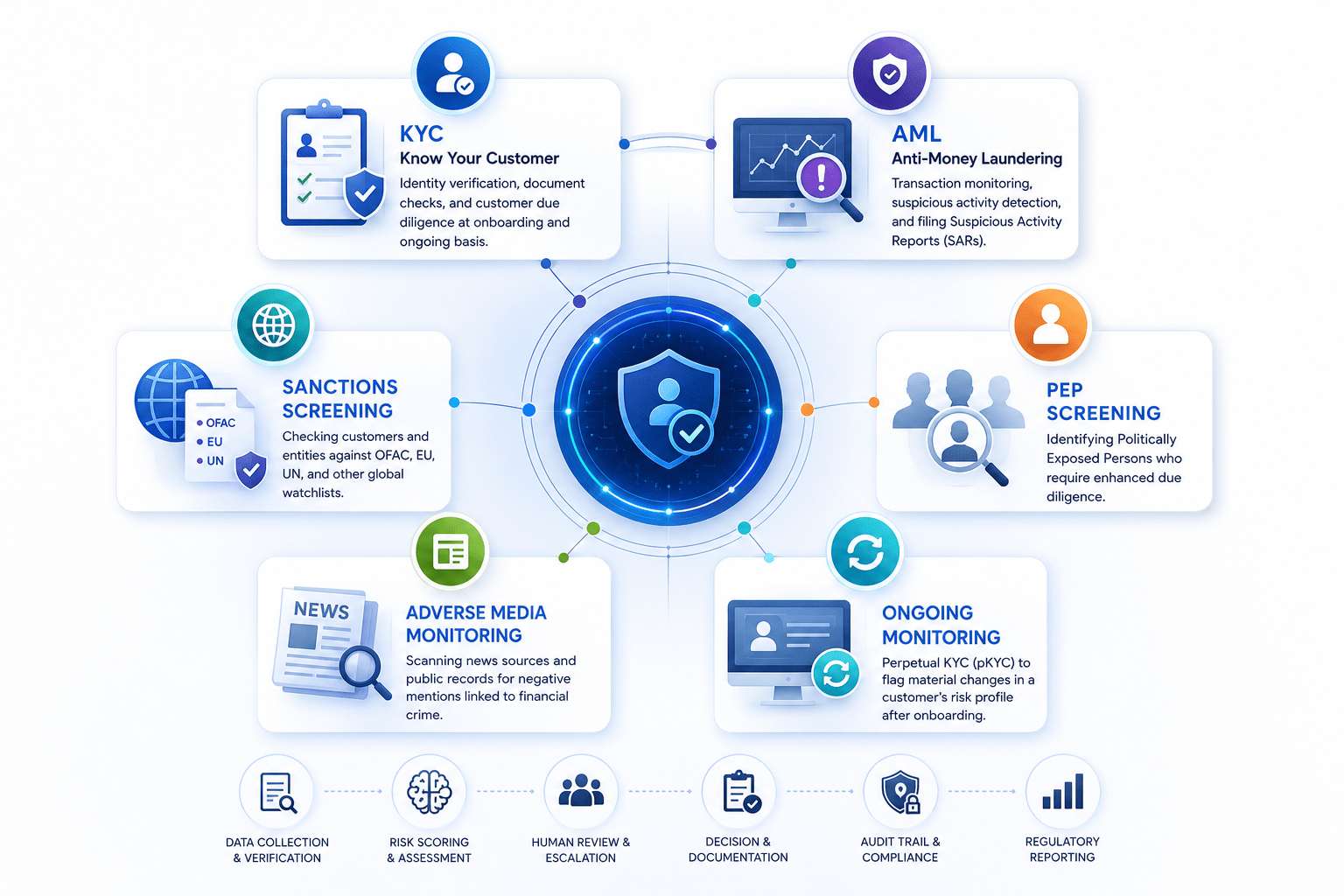

Compliance screening is the set of processes that verify customers, counterparties, and transactions against regulatory requirements. For most regulated businesses this includes:

At low volumes, these can be managed manually. On the scale that modern fintech platforms operate, thousands of onboardings daily, millions of transactions per month, they cannot. Manual screening introduces backlogs, creates inconsistent risk assessments, and makes it nearly impossible to maintain a defensible audit trail.

As detailed in SmartDev’s analysis of AI and regulatory compliance in fintech, regulators around the world are intensifying scrutiny while the pace of financial services operations continues to accelerate. The gap between what is required and what manual teams can deliver has become structurally unsustainable.

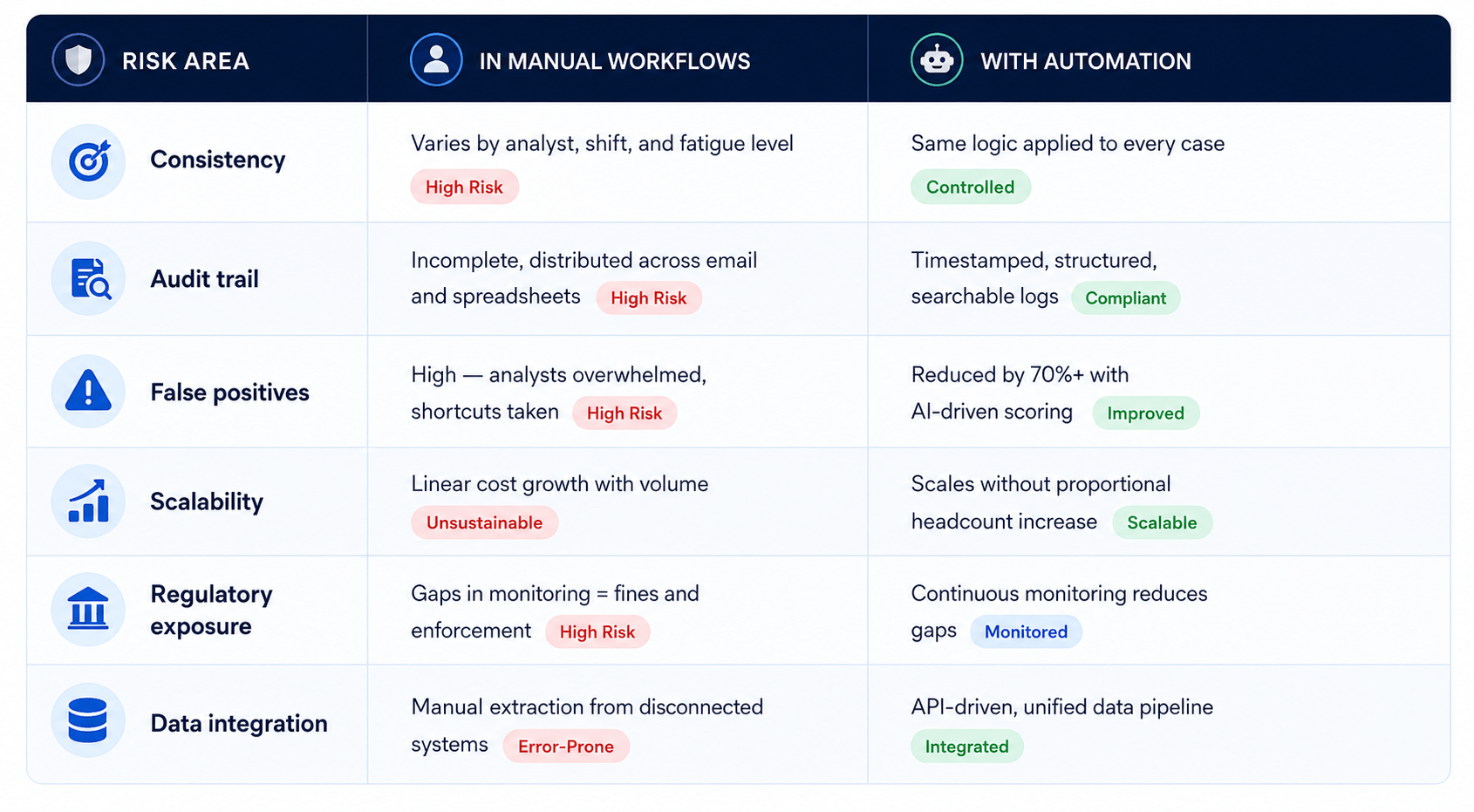

The Hidden Risks of Manual Compliance Workflows

Manual compliance screening is not simply slow; it actively generates the types of risk that compliance functions are meant to control. Understanding these risks is the starting point for a rational automation strategy.

These risks are compounded by regulatory complexity. As SmartDev’s guide to AI use cases in compliance highlights, the dynamic regulatory environment means that compliance teams must simultaneously monitor changes across multiple jurisdictions while managing day-to-day screening volumes, a combination that manual workflows cannot sustain.

How Automation Workflow Transforms Compliance Screening

Workflow automation in compliance is not a single tool; it is a connected layer that orchestrates multiple specialized processes into a repeatable, auditable sequence. The key distinction from simple task automation is that workflow automation connects people, data, rules, and systems into a coherent end-to-end process.

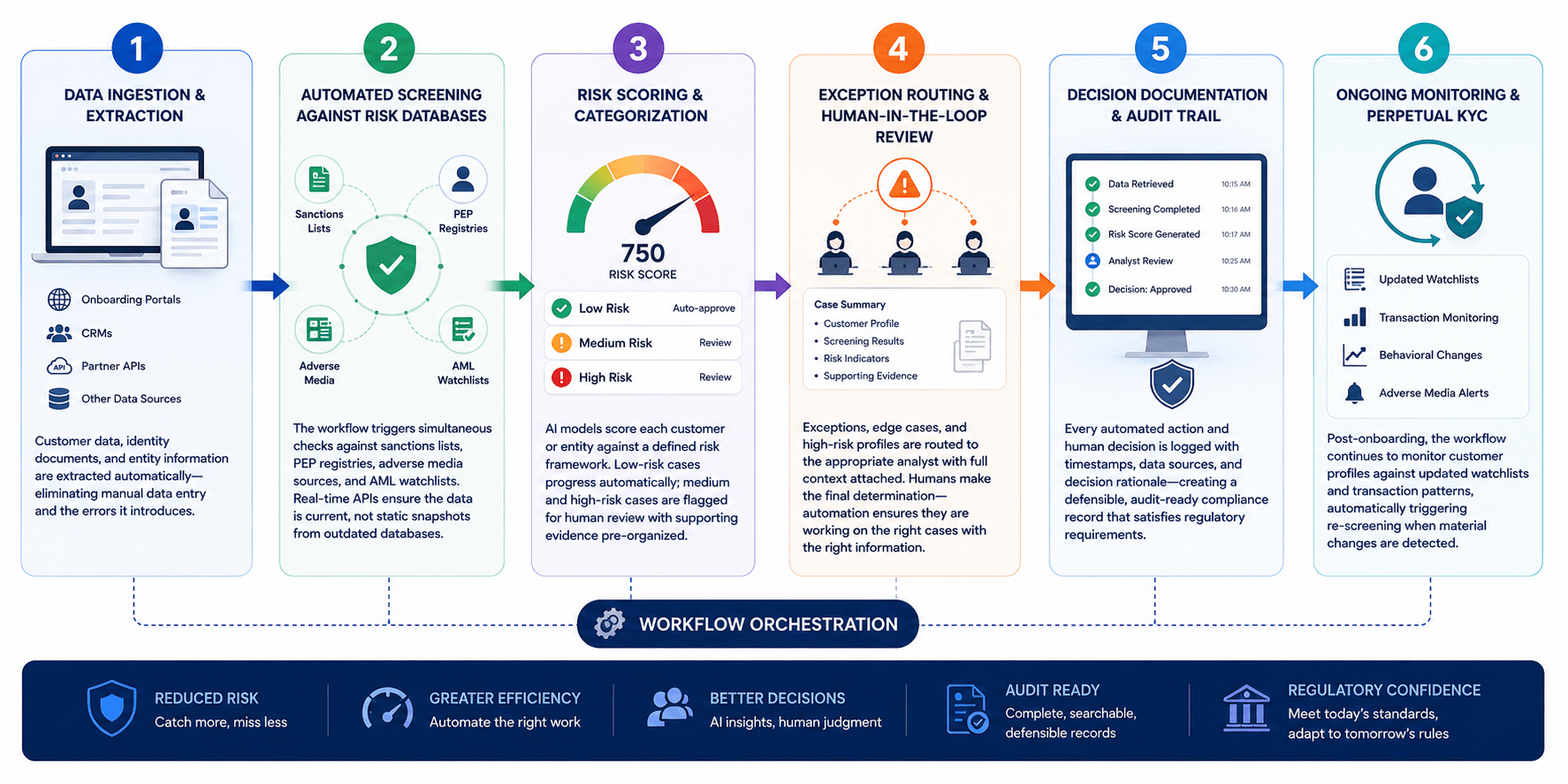

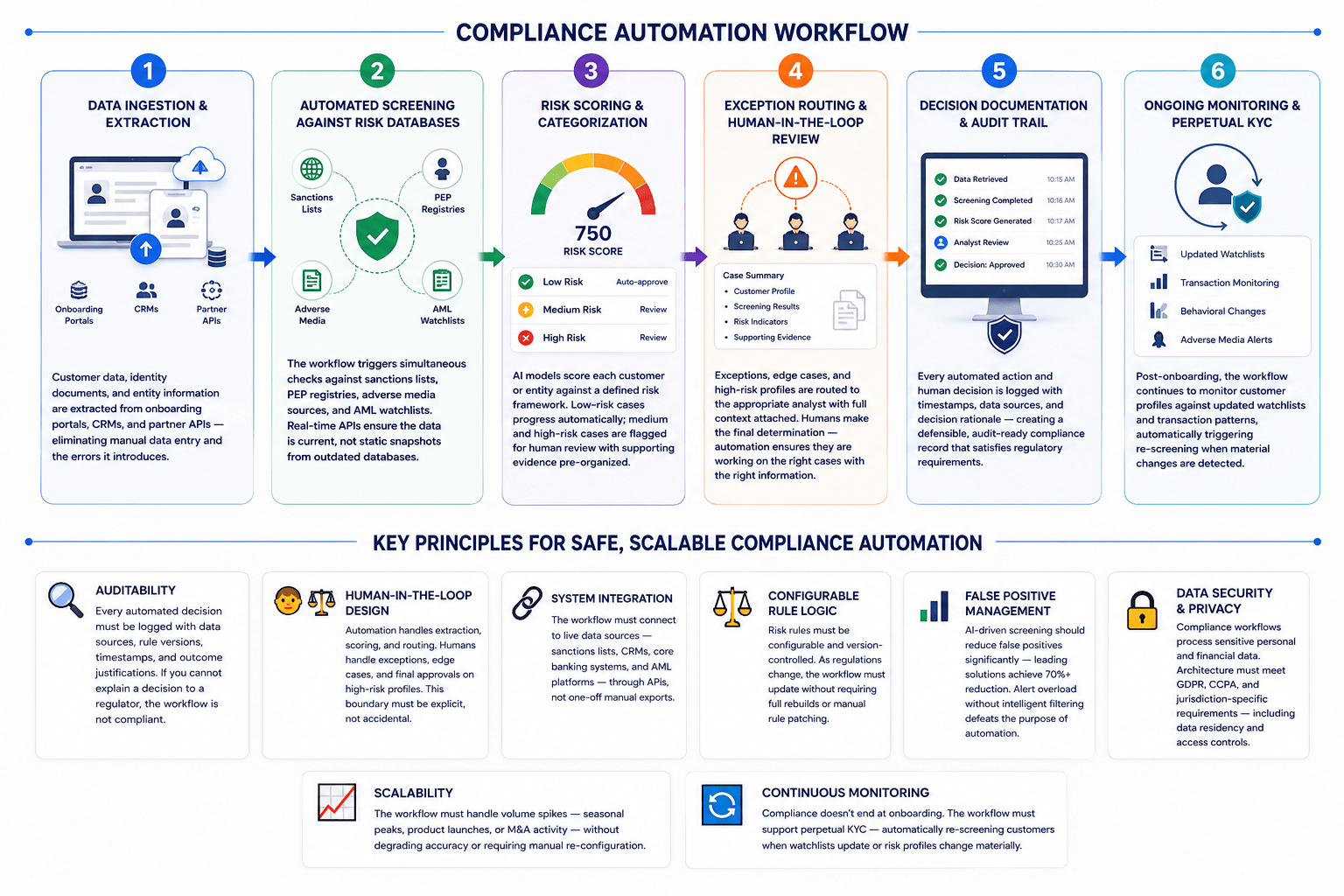

A well-designed compliance automation workflow typically covers the full screening lifecycle:

Data Ingestion & Extraction

The first stage of any compliance automation workflow is data ingestion, gathering customer data, identity documents, and entity information from every relevant source and structuring it for downstream processing. In practice, this means extracting fields from uploaded identity documents using OCR and document intelligence models, pulling entity data from onboarding portals and CRMs, and ingesting structured records from partner APIs and third-party identity verification services, all without manual re-keying.

The value of this step goes beyond convenience. Manual data entry is one of the leading sources of compliance error: transposed characters in names, missing fields, and formatting inconsistencies that cause legitimate customers to appear as watchlist matches or, worse, allow genuine risks to pass undetected. Automating ingestion eliminates this error class entirely. As detailed in SmartDev’s Document & Data Processing white paper, document intelligence pipelines built for compliance must handle unstructured documents, passports, utility bills, corporate certificates, as reliably as structured database records. The extraction layer must also be designed to flag low-confidence extractions for human verification rather than silently passing incomplete data into the screening pipeline.

Automated Screening Against Risk Databases

Once customer data is ingested and structured, the workflow triggers simultaneous checks across multiple risk databases, sanctions list (OFAC, EU, UN, HMT), PEP registries, adverse media sources, and AML watchlists, in parallel rather than in sequence. This concurrency is not just a performance improvement; it is a compliance requirement. Sequential screening introduces temporal gaps where a customer may be partially cleared before all checks have been completed, creating a window of regulatory exposure.

Critically, real-time API integrations ensure that screening is performed against current data, not static snapshots from databases that may be days or weeks out of date. FATF’s financial crime guidance explicitly addresses the risk of stale data in sanctions and PEP screening programs, noting that the adequacy of a screening program is evaluated in part by how current the underlying data is. For adverse media specifically, SmartDev’s AI-driven fraud detection analysis shows that real-time media monitoring can surface risk signals significantly earlier than periodic batch screening, often before a formal regulatory action is filed.

Risk Scoring & Categorization

Raw screening results, a list of potential matches, flagged entities, and adverse media hits, are not decisions. Risk scoring is the step that transforms screening outputs into actionable risk classifications. AI models evaluate each customer or entity against a defined risk framework, weighing factors such as geographic risk, entity type, transaction profile, screening match confidence, and adverse media severity to generate a composite risk score.

Low-risk cases, where screening returns no matches and the risk profile is consistent with the expected customer type, progress automatically through the workflow. Medium-risk cases, partial name matches, customers from elevated-risk jurisdictions, or profiles with minor adverse media, are queued for analyst review with supporting evidence pre-organized. High-risk profiles are escalated immediately, with enhanced due diligence checklists pre-populated based on the specific risk factors identified. As SmartDev’s AI risk management guide outlines, the key design principle here is that risk scoring must be explainable, every score must be traceable to specific data inputs and rule logic, so that analysts reviewing escalated cases understand exactly why a profile was flagged and regulators can audit the decision rationale.

This explainability requirement also guards against one of the most dangerous failure modes in compliance with AI: a black-box model that produces accurate aggregate results but cannot justify individual decisions. The Basel Committee’s operational resilience framework makes clear that institutions cannot rely on algorithmic outputs they cannot explain, a principle that applies directly to AI-driven risk scoring in compliance contexts.

Exception Routing & Human-in-the-Loop Review

Exception routing is where the human-in-the-loop principle becomes operational. Exceptions, edge cases, and high-risk profiles are not simply flagged and left in a queue, they are routed to the appropriate analyst with the full context of the case already compiled: screening match details, risk score breakdown, customer history, previous review outcomes, and any regulatory notes relevant to the specific risk type.

The analyst’s task is to make the final determination, not to reconstruct the case from scratch. This design principle, structured escalation rather than raw alert delivery, is central to reducing the analyst burden that causes compliance fatigue in manual workflows. As SmartDev’s compliance AI use case guide notes, the majority of false positives in manual screening environments occur not because the underlying match is genuinely ambiguous, but because analysts lack the context to resolve it efficiently. Pre-compiled case packages eliminate this gap. The ACAMS guidance on AML program effectiveness similarly emphasizes that the quality of human review is heavily dependent on the quality of information presented to the reviewer, a direct argument for structured, automated case preparation over raw alert dumps.

Decision Documentation & Audit Trail

Every automated action and human decision within a compliance of workflow must be logged. Each record should include timestamps, data sources, rule versions, and decision rationales. Moreover, organizations should store this information in an audit-ready format. This documentation is not optional. Instead, it forms the evidentiary foundation of the compliance program itself.

During regulatory examinations, regulators treat undocumented actions as if they never occurred. Therefore, compliance teams must maintain complete records. However, many organizations still rely on email threads, spreadsheets, and informal approval processes. As a result, they often struggle to reconstruct decision rationales. Consequently, regulators may challenge those decisions during review. Automated audit logging addresses this challenge systematically. Every workflow step generates a record automatically. Therefore, organizations no longer depend on analysts for manual documentation. As highlighted in SmartDev’s AI in Audit use cases guide, structured audit trails offer another advantage. They significantly reduce preparation time for regulatory examinations. Instead of spending weeks gathering evidence, teams can query structured logs directly. Furthermore, the Wolfsberg Group’s AML principles emphasize record-keeping completeness. They identify it as a core indicator of program quality. Therefore, robust audit logging delivers both operational and regulatory value.

Ongoing Monitoring & Perpetual KYC

Compliance responsibilities do not end after onboarding. A customer classified as low risk today may become high-risk later. For example, sanctions of designations, PEP appointments, adverse media coverage, or behavioral changes can increase risk. As a result, organizations must monitor customers continuously. Perpetual KYC (pKYC) enables this capability. Instead of relying on periodic reviews, it supports continuous monitoring. Moreover, it automatically triggers re-screening when material changes occur. These changes may appear in customer profiles or relevant watchlists. Consequently, organizations can identify emerging risks much faster.

In practice, the workflow maintains active monitoring across the entire customer portfolio. It continuously checks updated sanctions and PEP lists. In addition, it monitors transaction patterns against established behavioral baselines. When activity exceeds predefined thresholds, the system flags the deviation automatically. Subsequently, the workflow initiates a new screening cycle. It generates an updated risk assessment and routes the case for review. Furthermore, it follows the same exception-handling process used during onboarding. As SmartDev’s regulatory compliance analysis notes, regulators increasingly expect ongoing monitoring capabilities. In many jurisdictions, they view the absence of such capabilities as a program of deficiency. Likewise, SmartDev’s regulatory compliance analysis supports this approach. It found that pKYC programs consistently outperform periodic reviews. Specifically, automated triggers and structured re-screening workflows detect material risks earlier. As a result, organizations can address issues before they become reportable at events.

The value of this approach is explored in detail in SmartDev’s analysis of AI workflow automation ROI, which shows that in BFSI environments, the winning model is not human-less automation but rather human-supervised automation that improves speed, consistency, and traceability.

Key Criteria for Safe Compliance Automation

Not all compliance automation is created equally. Many early adopters discovered that poorly scoped automation simply moves the compliance risk to a new layer, creating algorithmic blind spots instead of human ones. The following criteria define what separates safe, effective compliance automation from implementations that introduce new risk.

These criteria align with SmartDev’s self-qualification guide for workflow automation, which emphasizes that the strongest automation candidates are not theoretical efficiencies but real bottlenecks, compliance review queues, delayed onboarding, and manual reporting cycles that operations leaders already know are broken.

Automating KYC and AML: A Step-by-Step Workflow

KYC and AML represent the most mature and high-impact areas for compliance automation within BFSI and fintech. As regulatory expectations continue to increase, these processes have evolved from manual, fragmented tasks into core operational priorities that demand both scale and precision. However, traditional approaches often remain siloed across tools, teams, and data sources, leading to inefficiencies and inconsistent outcomes.

A workflow automation layer fundamentally changes this structure by replacing fragmentation with a connected, end-to-end process. Instead of isolated steps, it brings together verification, screening, risk scoring, and human review into a single coherent flow. As a result, compliance operations become more structured, consistent, and fully auditable across the entire lifecycle.

Customer Onboarding: Automated KYC Flow

A customer submits an application. The workflow engine immediately receives the trigger and starts parallel processes. First, it extracts data from uploaded identity documents. Simultaneously, it enriches records through third-party identity verification services. Meanwhile, it screens applicants against PEP and sanctions databases in real time. Within seconds, the system generates a risk score. If the score falls within low-risk thresholds, onboarding proceeds automatically. However, the workflow routes medium-risk cases to analysts for review. In addition, its pre-compiles all supporting evidence. If the system classifies a profile as high-risk, it escalates the case immediately. Furthermore, it pre-populates priority flags and enhances due diligence checklists.

According to Fenergo’s KYC automation research, effective platforms require several core capabilities. These include dynamic workflow orchestration and real-time identity verification. In addition, organizations need document verification and automated AML screening. The platform should also support risk scoring and comprehensive audit trails. Most importantly, the workflow must connect these functions into a unified process. Otherwise, they operate as isolated point solutions. Consequently, organizations cannot achieve the full benefits of compliance automation.

Transaction Monitoring: Automated AML Flow

For ongoing AML compliance, the workflow monitors transaction patterns in real time. It compares customer behavior against established profiles and risk models. As a result, the system detects anomalies such as unusual volumes, geographic inconsistencies, and structuring patterns. Consequently, it generates automated alerts. However, it does not send raw alerts directly to analysts. Instead, it enriches each alert with customer history, screening results, risk indicators, and related transaction data. The system then prioritizes cases by risk level and routes them to the appropriate review team.

This enrichment-before-routing approach improves both efficiency and effectiveness. According to FATF guidance, AML programs should focus resources on high-risk cases. However, excessive raw alerts often overwhelm analysts with noise. Likewise, the ACAMS AML effectiveness framework emphasizes alert quality over alert quantity. Therefore, organizations should prioritize meaningful, evidence-backed alerts. Otherwise, triage fatigue can cause analysts to miss genuine risks. Furthermore, LexisNexis Risk Solutions links poor alert quality to rising compliance costs. By enriching alerts before review, organizations reduce workload while improving decision quality.

As detailed in iDenfy’s AML automation guide, continuous monitoring remains a core AML capability. Organizations must detect changes in customer risk profiles and suspicious transactions. In addition, they should monitor Source of Funds information, PEP updates, and watchlist changes. Together, these capabilities strengthen AML effectiveness. Most importantly, automation enables continuous monitoring at scale. As a result, compliance programs become more proactive, allowing organizations to identify and address risks earlier.

Sanctions & Adverse Media: Real-Time Automated Screening

Sanctions screening has historically been plagued by excessive false positives. As a result, name-matching algorithms often flag thousands of irrelevant results. Consequently, genuine risks can become buried among low-value alerts. However, modern AI-powered compliance automation takes a more sophisticated approach. Specifically, it incorporates behavioral analytics, transactional context, and entity resolution. As a result, the system can better distinguish common name matches from genuine risk indicators.

According to ShadowDragon’s research on automated KYC, enhanced screening delivers more accurate outcomes. In particular, the research highlights the value of OSINT intelligence and behavioral analytics. When combined, these capabilities can significantly reduce false positive rates. At the same time, they improve the quality of genuine risk signals. Therefore, compliance teams can focus their attention on higher-priority cases.

Automation Is Not Risk-Free, What to Watch

Compliance automation, like any operational change, carries its own risk surface. The organizations that manage it best are the ones that design these risks from the start rather than discovering them after implementation.

Algorithmic Bias and Model Drift

AI models trained on historical data can embed the biases of that data. A risk-scoring model that was trained on a predominantly domestic customer base may systematically mis-score international customers. Regular model auditing, bias testing, and recalibration must be built into the workflow governance process, not treated as optional maintenance.

Over-Automation: Removing Human Judgment Too Early

One of the most common mistakes in compliance automation is automating decisions that require contextual judgment. Sanctions screening for a common name in a high-risk jurisdiction, for example, may require human expertise to interpret correctly. Workflows must be designed with explicit escalation thresholds, and these thresholds must be reviewed regularly as the model matures.

Integration Risk: Data Quality and System Connectivity

Automated compliance workflows are only as accurate as the data flowing through them. Broken API connections, stale watchlist data, or incomplete customer records can generate false clearances, the most dangerous outcome in compliance. Data quality checks must be built into the workflow at every ingestion point.

Regulatory Technology Risk

As SmartDev’s regulatory compliance analysis notes, AI compliance systems must meet GDPR, CCPA, and jurisdiction-specific data requirements. The architecture of the workflow, where data is stored, who can access it, how decisions are explained, must be designed with regulatory technology requirements in mind from day one.

NORA by SmartDev: A Workflow-First Approach to Compliance

Most compliance automation projects fail not because the underlying AI is inaccurate. Instead, they fail because AI is not integrated into a governed process. Too often, organizations deploy isolated point tools. For example, they may use document extraction models or sanctions to screen APIs. However, these tools operate independently. Without a workflow layer, their outputs cannot become auditable decisions. As a result, organizations struggle to produce regulator-ready outcomes. This is precisely the gap NORA was built to address.

NORA is SmartDev’s AI adoption accelerator. Specifically, it helps enterprises move beyond fragmented AI experiments. Instead, it enables scalable and operational workflows. In compliance environments, NORA is not a standalone screening tool. Rather, it serves as the workflow layer connecting multiple AI capabilities. As a result, organizations can establish a coherent compliance process. Furthermore, the process remains auditable, governable, and continuously improvable. Most importantly, it can be confidently defended during regulatory reviews.

What Makes NORA Different

Unlike compliance point tools that automate a single task, NORA orchestrates the entire screening lifecycle. Rather than handing works off to emails or spreadsheets, it creates a connected workflow. For example, a submitted KYC document is not simply extracted. Instead, it is validated, screened, scored, and routed appropriately. In addition, every action is documented within a structured audit log. All of this occurs within the same governed process. As a result, every step remains traceable. Furthermore, every exception is logged. Most importantly, every decision can be explained and audited.

According to SmartDev’s analysis of enterprise AI project failure, fragmented implementation remains the most common challenge. Therefore, NORA is designed to address this issue from the beginning. Rather than starting with individual AI models, it starts with workflow architecture. As a result, organizations can establish governance and process integrity first. Only then are AI capabilities integrated into the workflow. This approach helps ensure scalability, consistency, and long-term operational success.

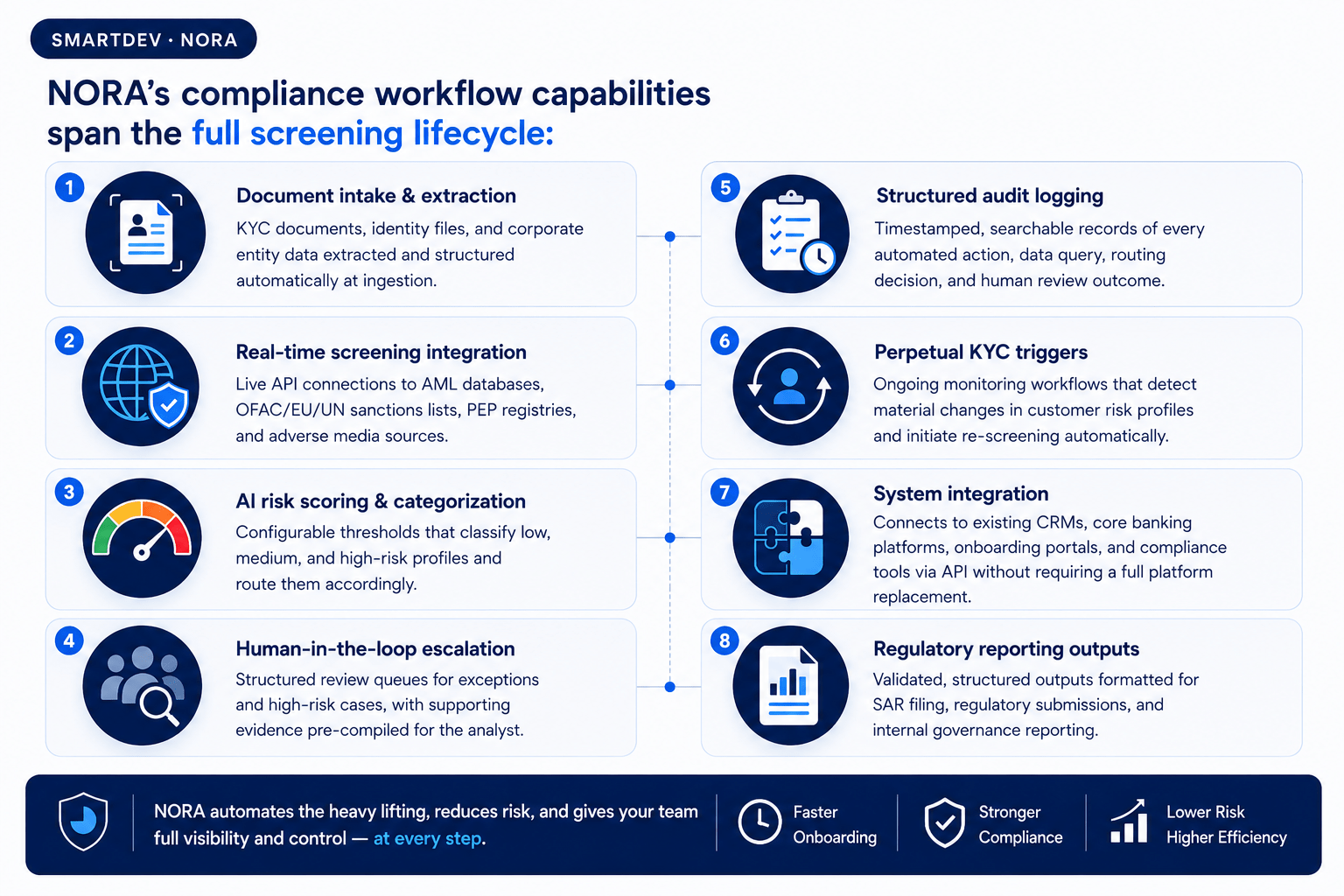

NORA’s Compliance Capabilities

NORA’s compliance workflow capabilities span the full screening lifecycle:

- Document intake & extraction – KYC documents, identity files, and corporate entity data extracted and structured automatically at ingestion

- Real-time screening integration – live API connections to AML databases, OFAC/EU/UN sanctions list, PEP registries, and adverse media sources

- AI risk scoring & categorization – configurable thresholds that classify low, medium, and high-risk profiles and route them accordingly

- Human-in-the-loop escalation – structured review queues for exceptions and high-risk cases, with supporting evidence pre-compiled for the analyst

- Structured audit logging – timestamped, searchable records of every automated action, data query, routing decision, and human review outcome

- Perpetual KYC triggers – ongoing monitoring workflows that detect material changes in customer risk profiles and initiate re-screening automatically

- System integration – connects to existing CRMs, core banking platforms, onboarding portals, and compliance tools via API without requiring a full platform replacement

- Regulatory reporting outputs – validated, structured outputs formatted for SAR filing, regulatory submissions, and internal governance reporting

NORA Is Not Human-less Automation

A common misconception about compliance automation is that it eliminates human analysts. However, NORA follows the opposite approach. Instead, it maximizes the value of analyst time. As a result, analysts focus on tasks that require judgment. These include edge cases, high-risk profiles, and complex entity assessments. Meanwhile, the workflow automates routine activities. For example, it handles data extraction, list matching, and report generation. Consequently, organizations execute these tasks consistently and on a scale.

In practice, NORA-powered workflows automate 70–80% of routine screening volume. As a result, cases move through automated pipelines with full audit coverage. Meanwhile, the remaining 20–30% require human judgment. Therefore, the workflow routes these cases to analysts. By then, it has already compiled and organized relevant evidence. In addition, supporting documentation is immediately available. Consequently, analysts can review cases more efficiently. The result is faster resolution, stronger documentation, and fewer false positives. Ultimately, organizations reduce the operational burden on compliance teams.

Implementation Approach

SmartDev’s implementation framework for NORA-based compliance workflows follows a workflow-first sequence: map the existing process against real documents and real exception patterns, define escalation thresholds explicitly, connect live data integrations before any automation goes live, and validate audit log completeness before deployment. As outlined in SmartDev’s enterprise automation ROI guide, this approach consistently delivers faster time-to-compliance than tool-first implementations that retrofit workflow governance after the fact.

Want to see NORA in action for compliance?

SmartDev’s team works with BFSI and fintech clients to map existing compliance workflows, identify automation-ready stages, and design the escalation and audit architecture before any code is written.

→ Request a compliance workflow assessment

Industry Applications: BFSI, Fintech & Beyond

Banking and Financial Services

Banks face some of the strictest compliance requirements across industries. They also manage the highest screening volumes. As a result, operational efficiency becomes a compliance requirement, not just a performance metric. When onboarding backlogs grows, customers wait longer. Consequently, revenue slows, and regulatory scrutiny increases. Automated KYC workflows address these challenges directly. They reduce onboarding times from days to minutes. At the same time, they maintain regulatory defensibility through structured data extraction. In addition, they support real-time screening and comprehensive audit logging throughout the process.

AML transaction monitoring automation addresses another critical challenge. Manual review queues often create dangerous delays. As a result, suspicious activity may remain unreviewed for days. Automated monitoring removes these bottlenecks through real-time alert processing. Furthermore, it enriches alerts with customer context before analysis. The system then routes prioritized, evidence-backed cases to human reviewers. Consequently, organizations detect risks faster and miss fewer threats. At the same time, they maintain a defensible record of every compliance decision.

According to SmartDev’s analysis of AI in finance, institutions deploying AI for compliance screening have reduced false positives by up to 200% and achieved estimated savings of 20% in fraud-related costs. Critically, these outcomes are only achievable when automation is integrated into the full end-to-end workflow, not applied as isolated point tools that leave gaps between automated and manual steps. For a deeper breakdown of how these gains are structured across banking use cases, SmartDev’s AI in compliance use cases guide covers the specific workflow architectures behind KYC, AML, and sanctions automation programs in retail and corporate banking environments.

Fintech Platforms

Fintech companies face a structurally distinct compliance challenge. On one hand, they scale quickly and experiment frequently, launching new products, entering new markets, and onboarding customers at volumes that grow faster than headcounts. On the other hand, they typically operate with lean teams, and regulatory frameworks expect structure, control, and traceability from day one, not after the next funding round. As a result, maintaining compliance while sustaining operational velocity becomes increasingly complex, and the gap between the two widens at exactly the moment of growth is fastest.

Compliance automation addresses this directly. According to SmartDev’s guide to AI use cases in fintech, compliance automation delivers some of the highest returns on investment of any AI application in financial services, precisely because it enables regulatory compliance without blocking the operational speed that defines fintech competitiveness. For a broader view of where AI creates the most value across the fintech stack, SmartDev’s AI in finance use cases analysis maps the full opportunity landscape, from onboarding to fraud detection to regulatory reporting.

For early-stage startups, automation helps reduce the compliance risks created by oversight or rapidly growing transaction volumes, allowing lean teams to manage regulatory obligations that would otherwise require dedicated compliance headcount from day one. For larger fintech organizations expanding across jurisdictions, automation becomes the standardization layer that maintains consistency across teams, products, and regulatory regimes. Without it, compliance processes fragment as the organization scales, creating the inconsistency that regulators penalize, and that internal audit surface at the worst possible moments. SmartDev’s regulatory compliance in fintech analysis covers how this scaling challenge plays out across different fintech verticals and what workflow architecture decisions determine whether compliance stays ahead of growth or falls behind it.

Insurance and Capital Markets

Insurance companies apply compliance automation across more workflows than most industries. For example, claims compliance requires screening claimants against fraud databases and sanctions lists. It also requires policy verification against regulatory requirements. Additionally, teams must document review rationales for every claim decision. Meanwhile, policyholder screening resembles banking of KYC processes. However, insurers must also assess geographic exposure, claim history, and product-specific risks. These factors add complexity beyond standard PEP and sanctions of screening. Furthermore, anti-fraud workflows require continuous transaction monitoring. Like AML programs, they analyze claim patterns instead of payment flows.

Capital markets firms also rely heavily on compliance automation. They screen counterparties before and after transactions. In addition, they automate reporting under MiFID II, EMIR, and similar regulations. They also use behavioral analytics to detect market abuse. These systems monitor trading patterns for insider trading and market manipulation indicators. Moreover, capital markets regulations are complex and deadline driven. Consequently, firms have little tolerance for manual errors. SmartDev’s AI-driven fraud detection analysis highlights this overlap. Specifically, behavioral AI models share core principles with AML monitoring systems. Therefore, firms can often leverage similar infrastructure across both cases.

Although insurance and capital markets face different use cases, they share the same requirement. Both need connected workflows that unify data collection, rule execution, human review, and audit logging. As a result, teams gain full traceability across compliance processes. Without this connectivity, compliance remains fragmented. Moreover, fragmented compliance is difficult to defend during audits or regulatory reviews. Ultimately, even sophisticated tools cannot compensate for disconnected workflows.

Risk Management Across All Sectors

Compliance screening is one component of a broader enterprise risk management function, and the workflow principles that govern it apply equally across fraud detection, credit risk assessment, operational risk monitoring, and third-party due diligence. As SmartDev’s AI risk management guide outlines, AI-powered systems can automate the routine, high-volume elements of risk management, screening, scoring, anomaly detection, and reporting, while preserving human judgment for the decisions that require contextual expertise. The risk reduction comes not just from catching more threats, but from catching them consistently, documenting the response, and building an audit record that demonstrates the program is working as designed.

For organizations mapping the full AI opportunity across their risk and compliance functions, SmartDev’s AI in audit use cases guide explores how automation extends into the internal audit function itself, reducing the manual sampling and evidence-gathering burden that has historically made compliance audits resource-intensive and slow. Together, these capabilities, screening automation, transaction monitoring, fraud detection, and audit automation, form the operational infrastructure of a modern, workflow-driven risk management program.

Best Practices to Automate Without Adding Risk

The following practices define the difference between compliance automation that reduces operational risk and automation that merely redistributes it.

Start with Real Documents, Not Hypothetical Processes

As SmartDev’s workflow automation qualification guide emphasizes, successful compliance automation starts with operational reality. Specifically, organizations should review actual documents from their workflows. These include real KYC files, screening cases, and exception patterns. By doing so, teams gain a clearer understanding of process complexity and risk exposure. Without this foundation, project assumptions can become unreliable. As a result, accuracy estimates are often overly optimistic. Likewise, delivery timelines may not reflect real-world requirements. Consequently, organizations risk creating compliance gaps that only emerge after deployment.

Define Escalation Thresholds Explicitly

Human-in-the-loop design is not merely a safety net. Instead, it serves as a foundational architectural principle. Therefore, organizations should clearly define escalation criteria from the outset. Specifically, they must identify which case types escalate automatically. In addition, they should determine which risk scores require human review. Likewise, decision types requiring supervisor approval must be explicitly documented. Most importantly, these thresholds should not remain in informal guidelines. Instead, they should be documented, version-controlled, and consistently maintained. Furthermore, organizations should review them quarterly. As a result, governance standards remain aligned with evolving risks, regulations, and operational requirements.

Build Audit Logging from Day One

Audit trails cannot be retrofitted into compliance workflows. Instead, they must be embedded within the data model from the beginning. Therefore, auditability should be treated as a core design requirement, not an afterthought. Specifically, every automated decision must be recorded. Every data source query should be logged. Likewise, all routing actions and human review outcomes must be documented. As a result, organizations can maintain complete process transparency. Most importantly, these records must be stored in a format that satisfies regulatory inspection requirements, ensuring that compliance decisions remain traceable, defensible, and ready for audit at any time.

SmartDev’s AI in Audit use cases guide covers how structured audit logging reduces manual audit hours while improving evidence coverage, a particularly high-value capability in environments where regulators may request transaction-level decision trails at short notice. For document-heavy compliance workflows, SmartDev’s Document & Data Processing white paper details the data model patterns that make audit logging both complete and operationally maintainable.

Use API-First Integrations for Live Data

Compliance workflows that rely on static database exports are inherently vulnerable to compliance gaps. This vulnerability exists because regulatory data changes continuously. For example, sanctions lists may change daily. Likewise, political developments can quickly alter PEP registries. In addition, adverse media sources generate new information around the clock. As a result, exported databases become outdated rapidly. Therefore, organizations should connect workflow automation to live data sources through real-time APIs. They should avoid relying on periodic data loads. By doing so, they can make decisions using current information. Consequently, they improve accuracy, reduce risk exposure, and strengthen regulatory defensibility.

This principle shapes SmartDev’s regulatory compliance framework for fintech. Specifically, the framework treats live API connectivity as a baseline requirement. It does not treat it as an optional enhancement. For teams evaluating integration architecture, SmartDev’s workflow automation readiness guide offers a practical checklist. It helps organizations assess whether current data pipelines support real-time compliance needs. Externally, FATF’s guidance on financial inclusion and AML reinforces the importance of timely screening data. It recognizes data timeliness as a key factor in compliance effectiveness. Therefore, organizations should prioritize real-time data access when designing compliance workflows.

Assign Internal Ownership

Even with a managed service like NORA, vendors only carry technical responsibility. However, organizations must maintain clear internal accountability. According to SmartDev’s implementation framework, several prerequisites must exist before deployment. First, organizations need a clear internal point of contact. Second, they need a well-defined workflow. Third, they need genuine organizational buy-in. Without these foundations, implementation becomes fragmented and inconsistent. Ultimately, automation alone cannot satisfy compliance requirements. Instead, compliance depends on both technology and internal accountability working together.

This theme appears repeatedly in SmartDev’s analysis of enterprise AI project failure. In most cases, technical capability is not the primary constraint. Instead, organizations struggle when they view automation as vendor delivery. Rather, successful organizations treat it as an internal transformation effort. For additional guidance, SmartDev’s AI consulting services offer compliance readiness assessments. These assessments map ownership, accountability, and escalation structures before implementation. Likewise, the Basel Committee’s principles on operational resilience reinforce this approach. They emphasize active internal governance for third-party technologies. Therefore, organizations should never rely on vendors alone.

Monitor and Improve Continuously

The best compliance automation programs treat workflows as living systems. Teams continuously monitor and optimize performance. They track false positive rates, escalation volumes, processing times, and audit findings. Importantly, they treat these as operational indicators, not vanity metrics. These signals reveal how effectively the system performs over time. Moreover, teams retrain models as new data patterns emerge. Likewise, they adjust thresholds when business conditions change. As a result, the system evolves with the organization. Ultimately, this improvement cycle separates effective automation from static approaches that quickly become outdated.

SmartDev’s AI risk management guide explains how fintech organizations should structure continuous monitoring frameworks. It also shows how performance reviews support broader risk governance cycles. Meanwhile, SmartDev’s enterprise automation ROI analysis provides benchmark metrics across compliance maturity levels. Externally, ACAMS guidance highlights rising regulatory expectations for AML program effectiveness. Specifically, regulators increasingly require documented evidence of model reviews and threshold calibration. Therefore, continuous improvement is no longer optional. Instead, it has become both a best practice and a regulatory expectation.

Supporting Resources

For teams exploring AI in audit and compliance verification, SmartDev’s AI in Audit use cases guide provides a detailed breakdown of how automation reduces manual audit hours while improving coverage. SmartDev’s AI Automation: Document & Data Processing white paper offers ROI benchmarks and implementation playbooks for document-heavy compliance workflows.

Conclusion: Compliance Automation Is a Risk Management Strategy

Automation workflow is not the enemy of compliance; poorly designed automation is. However, a well-designed workflow strengthens compliance operations. It embeds auditability, human escalation, live data integration, and configurable risk logic. As a result, it has become one of the most effective tools for managing compliance risk.

Moreover, leading organizations treat compliance automation as a workflow challenge, not a technology purchase. First, they use real operational data. Next, they define clear escalation boundaries. Then, they build audit trails from day one. Finally, they continuously refine workflows instead of treating implementation as a one-time project.

NORA by SmartDev follows this philosophy. As an AI adoption accelerator, it connects document extraction, risk scoring, exception routing, human review, and regulatory reporting. Consequently, teams can execute repeatable compliance workflows. As a result, compliance teams scale screening operations without increasing headcounts. Furthermore, NORA helps organizations avoid risks that poorly governed automation often creates.

For BFSI institutions, fintech platforms, and regulated businesses, now is the time to adopt workflow-first compliance automation. Indeed, regulatory pressure and competitive costs continue to increase. Meanwhile, proven tools already support safe implementation. Contact us to explore how AI-powered compliance automation can help your organization stay compliant, reduce manual effort, and scale with confidence.