TL,DR

- Legacy compliance systems create too many false positives, forcing analysts to spend hours reviewing alerts that often turn out to be harmless.

- AI helps add context to each alert by analyzing customer profiles, transaction history, past cases, and risk patterns.

- The real value is not just reducing alert volume, but helping teams investigate faster, prioritize real risks, and document decisions clearly.

- NORA supports this by turning fragmented compliance tasks into AI-powered workflows with human review still in control.

Introduction

Compliance teams were built to detect risk. Today, many are spending most of their time proving that risk is not actually there. Across banking, fintech, insurance, payments, and other regulated industries, compliance teams are facing a growing operational problem: too many alerts, too little context, and not enough time to separate real threats from harmless activity.

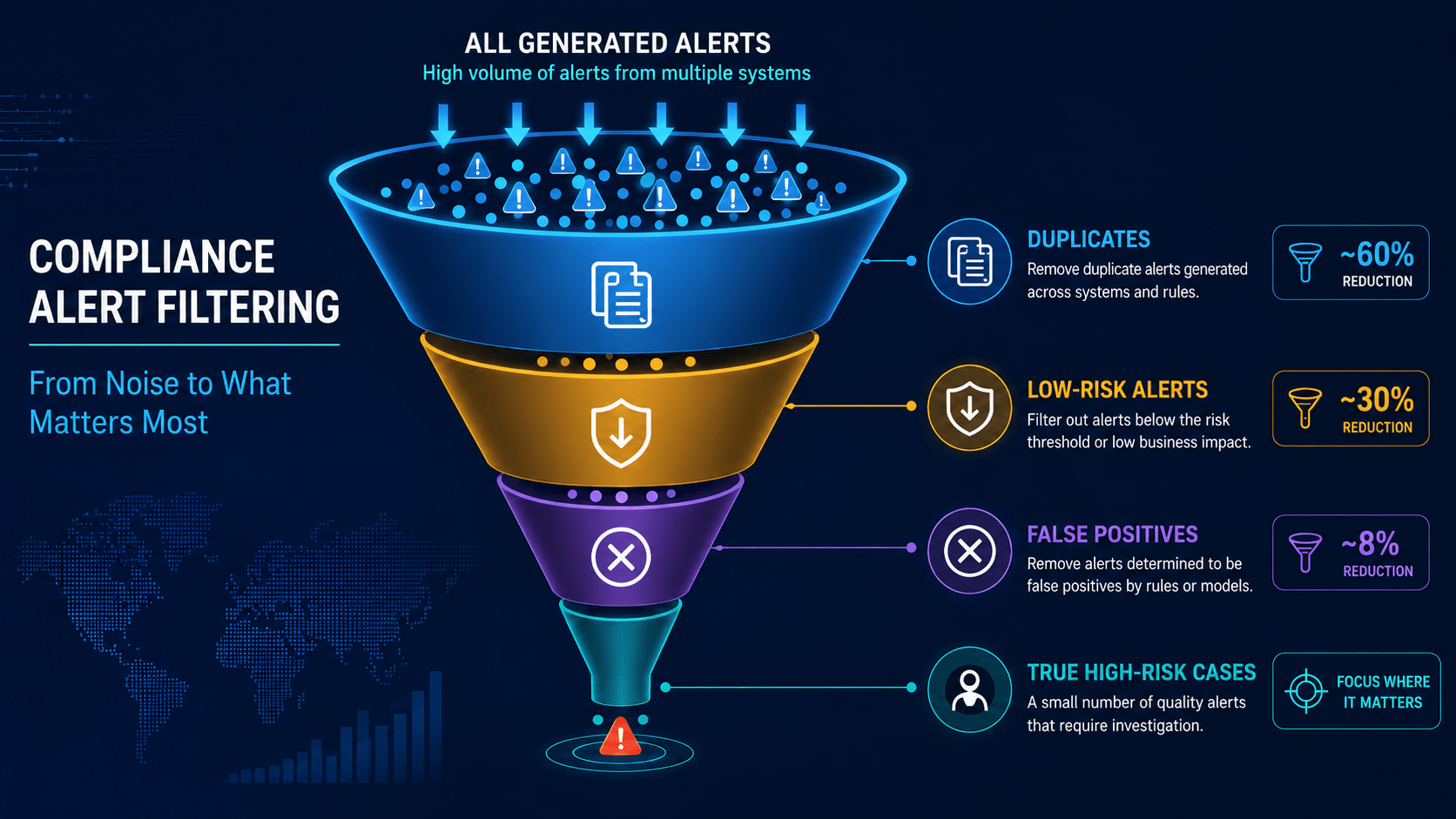

This is not a minor inconvenience. False positives create real business pressure. Analysts spend hours reviewing low-value alerts. Customer onboarding slows down. Operational costs increase. Investigation backlogs grow. Most importantly, genuine risks can become harder to spot because they are buried under too much noise. Google Cloud has noted that traditional AML systems can generate extremely high false positive rates, while its AML AI work with HSBC reportedly reduced alert volumes by more than 60% and identified two to four times more suspicious activity. The lesson is clear: stronger compliance does not come from producing more alerts. It comes from producing better, more contextual, and more actionable alerts. (IBM)

At SmartDev, we see this as more than a technology problem. This is where AI workflow automation becomes critical. AI can help reduce noise, but its real value appears when it is embedded into the full compliance workflow: from alert intake and case enrichment to human review, escalation, documentation, and continuous improvement.

What Are False Positives in Compliance?

What Is a False Positive?

A false positive in compliance is an alert that appears suspicious at first but turns out to be harmless after review. For example, a transaction monitoring system may flag a customer because they made several high-value transfers in a short period. The system sees unusual activity and creates an alert. However, after reviewing the customer’s profile, transaction history, and business context, the analyst may discover that the customer is simply paying suppliers or moving funds for a legitimate business purpose. In that case, the alert was not wrong to be cautious, but it did not represent real risk.

Why Do False Positives Happen?

False positives happen because compliance systems are intentionally sensitive. In regulated sectors, missing a suspicious transaction can lead to serious consequences, including fines, regulatory scrutiny, and reputational damage. As a result, many organizations prefer systems that “over-alert” rather than miss potential risk.

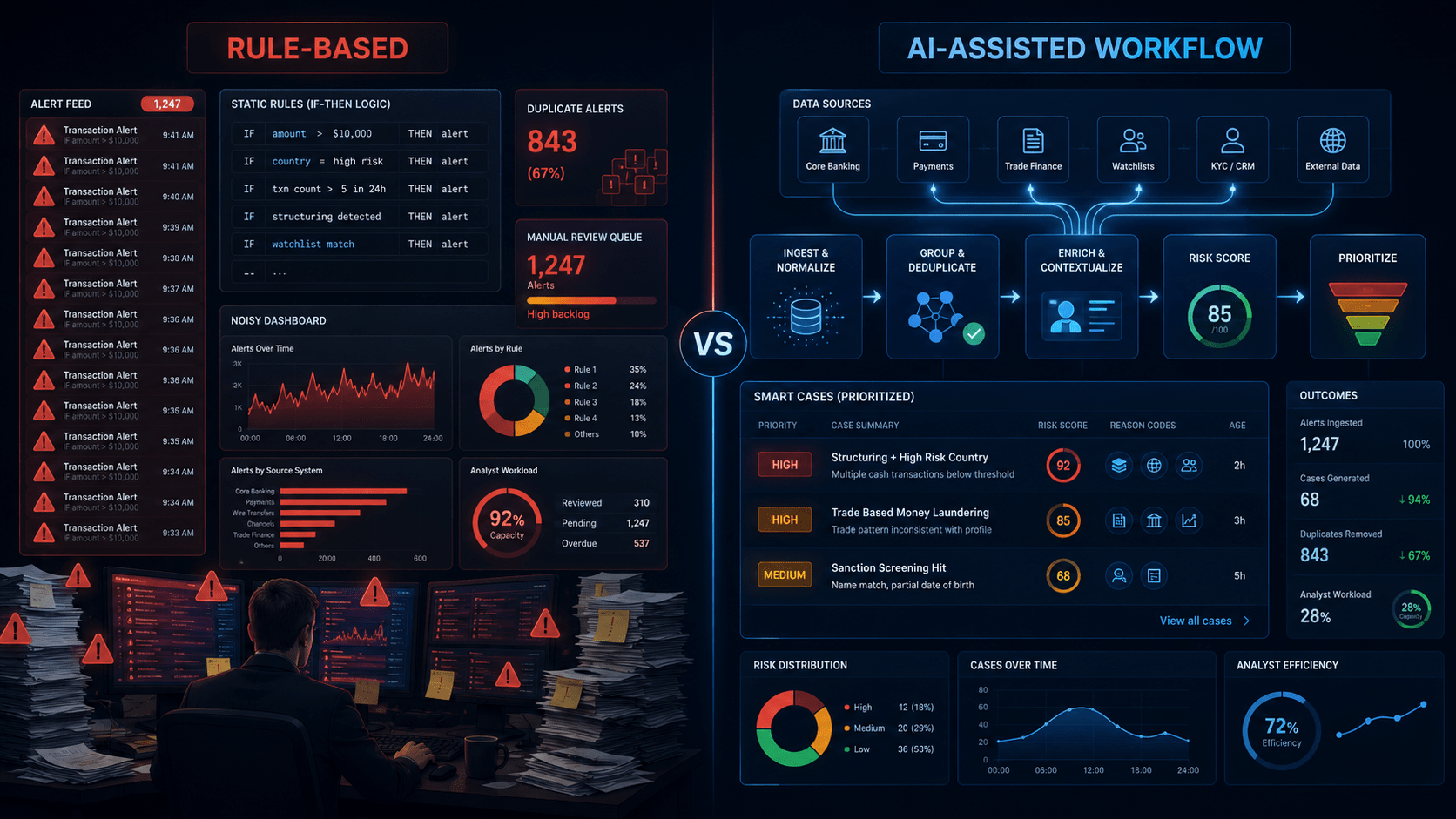

The Limitations of Rule-Based Monitoring

The problem begins when this cautious approach becomes operational noise. Traditional rule-based systems can identify that something is unusual, but they often struggle to understand whether that activity is unusual in a meaningful way. A transaction that looks suspicious for one customer may be perfectly normal for another, depending on their profile, business model, transaction history, geography, and relationship network.

Why Compliance Teams Are Drowning in False Positives

Financial Activity Has Become More Complex

The main reason compliance teams are drowning is that financial activity has become much more complex, while many monitoring systems still rely on static rules. Customers now use digital wallets, instant payments, embedded finance platforms, international transfers, online marketplaces, gig economy income streams, and multi-account financial ecosystems. A behavior that looked unusual ten years ago may now be completely normal. For example, a small business owner may receive multiple payments from different accounts in one day. A freelancer may receive cross-border payments from clients in several countries. A digital bank customer may move funds quickly across apps. Without context, these activities can trigger alerts even when there is no real risk.

Legacy Rules Are Too Rigid for Modern Risk

Legacy systems often depend on fixed rules such as transaction thresholds, high-risk jurisdictions, sudden changes in activity, partial name matches, or multiple transfers within a specific time window. These rules are useful because they are easy to define and audit, but they are also blunt instruments. They do not always understand customer intent, business context, historical behavior, or relationships between entities. Deloitte has highlighted high false positive volumes as a major AML transaction monitoring challenge, noting that many generated alerts are closed as false positives, which wastes resources and increases operational costs. (Deloitte)

Fragmented Data Slows Every Investigation

The problem becomes worse when compliance data is fragmented. A single alert may require analysts to check customer profiles, KYC records, transaction history, sanctions results, previous cases, risk policies, internal notes, and external data sources. When these systems are disconnected, every investigation becomes a manual research task. Analysts spend too much time gathering information before they can make a decision. This is especially painful for financial institutions still working with older systems, which is why integration is such a critical part of AI integration with legacy systems in financial services.

Alert Fatigue Makes Real Risk Harder to Spot

Over time, this creates alert fatigue. When analysts review too many low-value alerts, they become desensitized to the warning signals. This can reduce investigation quality, slow response times, and make genuine risks harder to identify. Lucinity has described alert fatigue as a major AML challenge, particularly when traditional monitoring systems produce high false positive rates and depend heavily on manual processes. (Lucinity) In practice, this means compliance teams are not failing because they are slow. They are struggling because their tools keep asking them to investigate too many weak signals without enough context.

The Business Cost of False Positives

False Positives Increase Operational Costs

False positives are often treated as a compliance operations issue, but their impact reaches far beyond the compliance department. Every false positive requires analyst time, case review, documentation, and sometimes escalation. As alert volumes grow, organizations may respond by hiring more compliance staff, but headcount alone does not solve the root problem. If the system keeps generating low-quality alerts, the company simply becomes better staffed at doing inefficient work. That is not transformation. That is expensive maintenance.

False Positives Create Friction for Legitimate Customers

False positives also damage customer experience. A legitimate customer may experience delayed onboarding, repeated document requests, paused transactions, additional reviews, or unnecessary friction during account opening. For fintech companies, digital banks, insurers, lending platforms, and payment providers, these delays can directly affect conversion, retention, and revenue. In financial services, trust depends on both security and speed. Customers expect protection, but they also expect smooth digital experiences. This is why AI-enabled compliance should be seen as part of a broader AI in BFSI transformation, not just a back-office efficiency project.

False Positives Make Real Risks Harder to See

The most serious cost, however, is risk visibility. When teams are overwhelmed by low-value alerts, true suspicious activity can be hidden inside a large backlog. More alerts do not automatically mean better compliance. In some cases, more alerts simply mean more noise. This is why compliance leaders are shifting the conversation from alert volume to alert quality. The goal is not to generate as many alerts as possible. The goal is to identify the right cases faster, with enough context for analysts to make defensible decisions.

Why More Rules Are No Longer Enough

Threshold Tuning Only Solves the Surface Problem

When false positives increase, many organizations try to fix the problem by tuning thresholds or adding more rules. This can help in the short term, but it rarely solves deeper issues. If a threshold is too strict, the system creates too many false positives. If it is too loose, the organization may miss the real risk. Adding more rules can also create complexity, overlap, and maintenance burden. The compliance team may end up managing a large rule of library that becomes harder to interpret, test, and improve.

Rules Are Reactive, While Financial Crime Keeps Evolving

Rules are also reactive. They are usually created after a known pattern has been identified. But financial crime tactics evolve quickly. Criminal networks adapt to their behavior, use new channels, exploit faster payment systems, and increasingly rely on digital tools. Reuters reported that Nasdaq Verafin and BioCatch partnered to combine transactional data with behavioral analytics to combat growing payment fraud risks, including scams and social engineering attacks that exploit rapid payment systems. (Reuters) This shows that financial crime detection is moving beyond simple transaction rules toward richer behavioral and contextual analysis.

Modern Compliance Needs More Than Static Rules

The Financial Action Task Force has also emphasized that new technologies, including AI, machine learning, and natural language processing, can help AML/CFT efforts by improving risk identification and supporting more effective analysis of complex data. (University of Strathclyde) This does not mean rules are obsolete. It means rules alone are not enough for modern compliance. Organizations need systems that can understand context, learn from historical decisions, connect data sources, and support analysts across the full investigation process.

What AI Actually Does About False Positives

AI Adds Context to Alerts

AI is useful in compliance because it can analyze more signals, compare more patterns, and support faster decision-making. But its value should not be exaggerated. AI does not make compliance risk disappear. It does not remove regulatory responsibility. It does not replace human judgment. What AI can do is help teams manage alerts with more context, better prioritization, and less manual effort.

A traditional rule may detect that a customer made a high-value transfer. AI can look at whether that transaction is unusual for this specific customer, whether it matches peer behavior, whether the customer profile explains the activity, whether similar patterns appeared in previous cases, and whether related accounts show additional risk signals. This matters because risk is not absolute. It depends on context. A transaction that is suspicious for one customer may be normal for another. By analyzing customer behavior, transaction history, KYC information, network relationships, and historical case outcomes, AI can help analysts move from “a rule was triggered” to “this case is meaningful because of these specific factors.”

AI Prioritizes the Alerts That Matter Most

AI helps prioritize alerts by risk. Not all alerts deserve the same level of attention. AI can classify cases into high-risk, medium-risk, low-risk, duplicate, or incomplete-information categories. This allows analysts to focus first on the cases most likely to require action. For financial institutions managing AML, fraud, and customer due diligence at scale, this prioritization can become a major productivity lever. It is also closely connected to broader AI use cases in banking, where operational efficiency, risk detection, and customer experience must improve together.

AI Reduces Manual Investigation Work

AI reduces manual research. Many compliance investigations begin with analysts opening several systems, reviewing long histories, checking documents, comparing case notes, and preparing summaries. AI can support this work by summarizing customer profiles, extracting relevant transaction history, finding related cases, highlighting unusual behavior, drafting investigation notes, and suggesting next steps. A University of Strathclyde paper on automation and AI in AML notes that NLP can help interpret content in context, which is critical because information that appears alarming in isolation may mean something different when viewed with the right surrounding details. (University of Strathclyde) This is where AI becomes practical: it gives analysts a clearer starting point instead of forcing them to assemble every case manually.

AI Learns from Historical Decisions

AI can learn from historical decisions. Compliance teams make thousands of decisions over time, and those decisions contain useful patterns. If analysts repeatedly close a certain type of alert as low-risk, AI can help identify that pattern. If another pattern often leads to escalation or suspicious activity reporting, AI can increase its priority. This creates a feedback loop where the system becomes better aligned with how the organization actually handles risk. McKinsey has also discussed how agentic AI can reshape financial crime operations by supporting end-to-end KYC and AML workflows, moving institutions from isolated manual tasks toward more automated and coordinated processes. (McKinsey & Company)

What AI Does Not Do in Compliance

AI Does Not Remove Accountability

AI can improve compliance operations, but it must be implemented carefully. In regulated industries, a powerful model is not enough. Organizations need explainability, governance, auditability, and human accountability. AI does not remove regulatory responsibility. Even if a system recommends closing or escalating a case, the organization remains accountable for the final decision.

AI Does Not Fix Poor Data Quality Automatically

AI also does not automatically fix poor data quality. If customer records are incomplete, outdated, inconsistent, or spread across disconnected systems, AI output will be weaker. Strong data foundations are still necessary for any AI-enabled compliance workflow to work properly.

AI Should Not Operate as a Black Box

AI should not operate as a black box. Compliance teams need to understand why a case was prioritized, what data was used, what risk factors influenced the recommendation, and who made the final decision. The Bank for International Settlements has warned that limited explainability can contribute to model risk in financial services, especially when AI systems are used to support critical decisions. The Financial Stability Board has also highlighted risks related to model complexity, data quality, governance, and explainability as AI adoption grows in financial institutions. (IBM)

AI Should Support Human Judgment, Not Replace It

The right framing is simple: AI handles the noise, while humans handle accountability. In compliance, the best AI systems do not remove people from decision-making. They remove low-value work from people so analysts can focus on judgment, escalation, and defensible decisions. This is why AI in compliance must be designed around human-in-the-loop workflows, not full automation for every case.

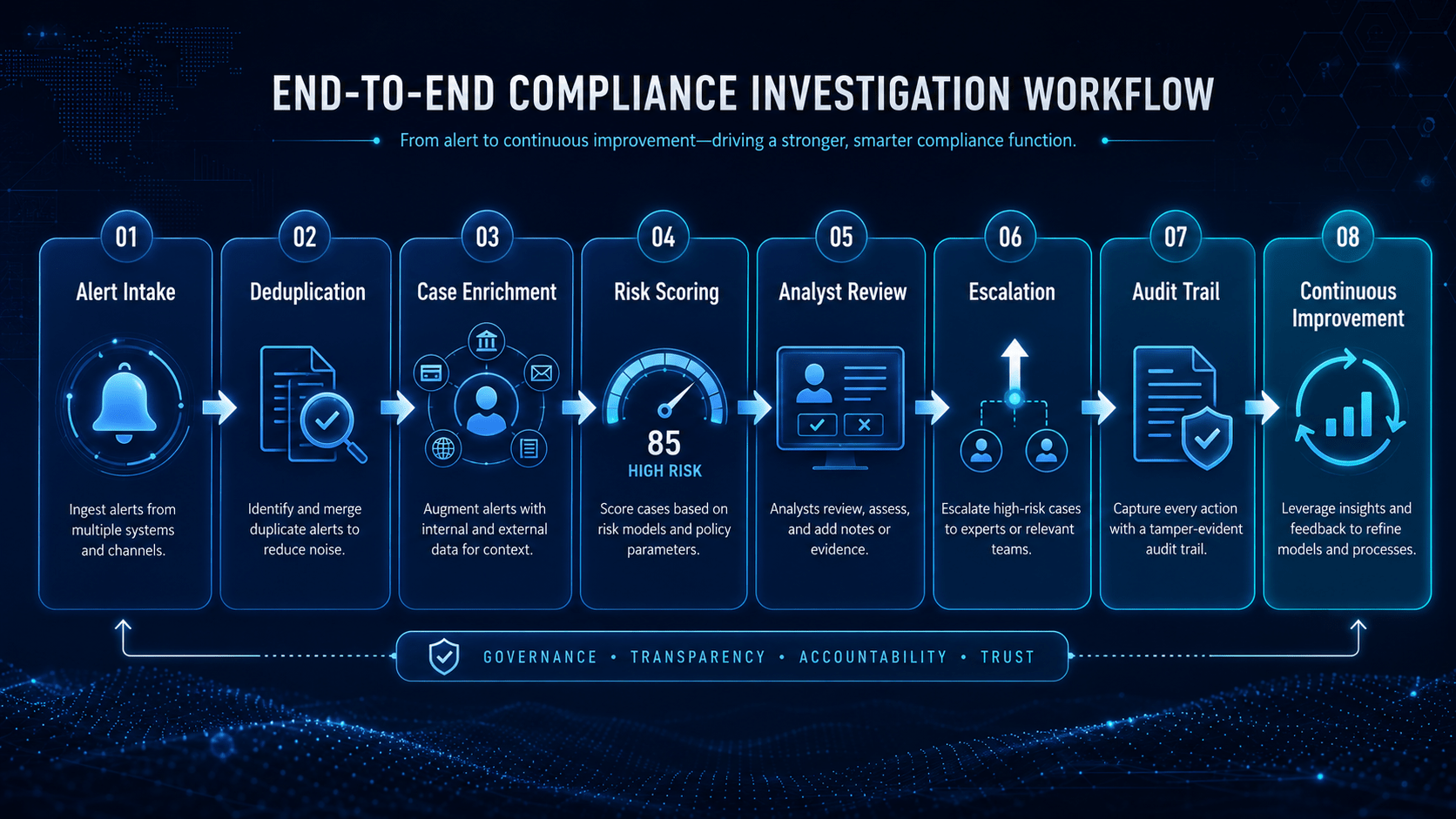

From Alert Reduction to Investigation Orchestration

False Positive Reduction Is Only Part of the Value

Many organizations think the main benefit of AI is false positive reduction. That is important, but it is only part of the story. The bigger opportunity is investigation orchestration. False positives are not just an alert problem because even after an alert is created, the team still needs to collect data, check customer history, review KYC documents, compare past cases, assess risk, write notes, escalate issues, prepare reports, and maintain audit evidence. If these steps remain fragmented, compliance teams will still struggle even if alert volumes decrease.

AI Workflow Automation Connects the Full Investigation Process

This is where AI workflow automation becomes more valuable than isolated AI scoring. A standalone model may help rank alerts, but it does not automatically fix the process around those alerts. A real compliance workflow needs to connect systems, data, decisions, people, and documentation. It needs to help analysts understand what happened, why it matters, what evidence is available, what action is recommended, and how the final decision is recorded. This is closely linked to SmartDev’s perspective on what AI solution brings the best ROI to enterprises: AI creates stronger business value when it is connected to real operational workflows rather than deployed as a disconnected experiment.

An AI-Powered Compliance Workflow Gives Teams a Better Operating Model

An AI-powered compliance workflow usually starts with alert intake from transaction monitoring, AML screening, fraud detection, sanctions screening, or KYC tools. The system then groups duplicate or related alerts, enriches the case with customer and transaction context, scores the case based on risk indicators, generates a summary for the analyst, supports human review, and records the decision with an audit trail. This is not about replacing compliance teams. It is about giving them a better operating model.

The Workflow Around the Model Matters Just as Much as the Model

SmartDev has discussed this workflow-first mindset in our article on why enterprise AI projects fail. Many AI initiatives fail because they focus too much on the model and not enough on how work actually moves across departments, systems, and decisions. Compliance is a perfect example. The model matters, but the workflow around the model matters just as much.

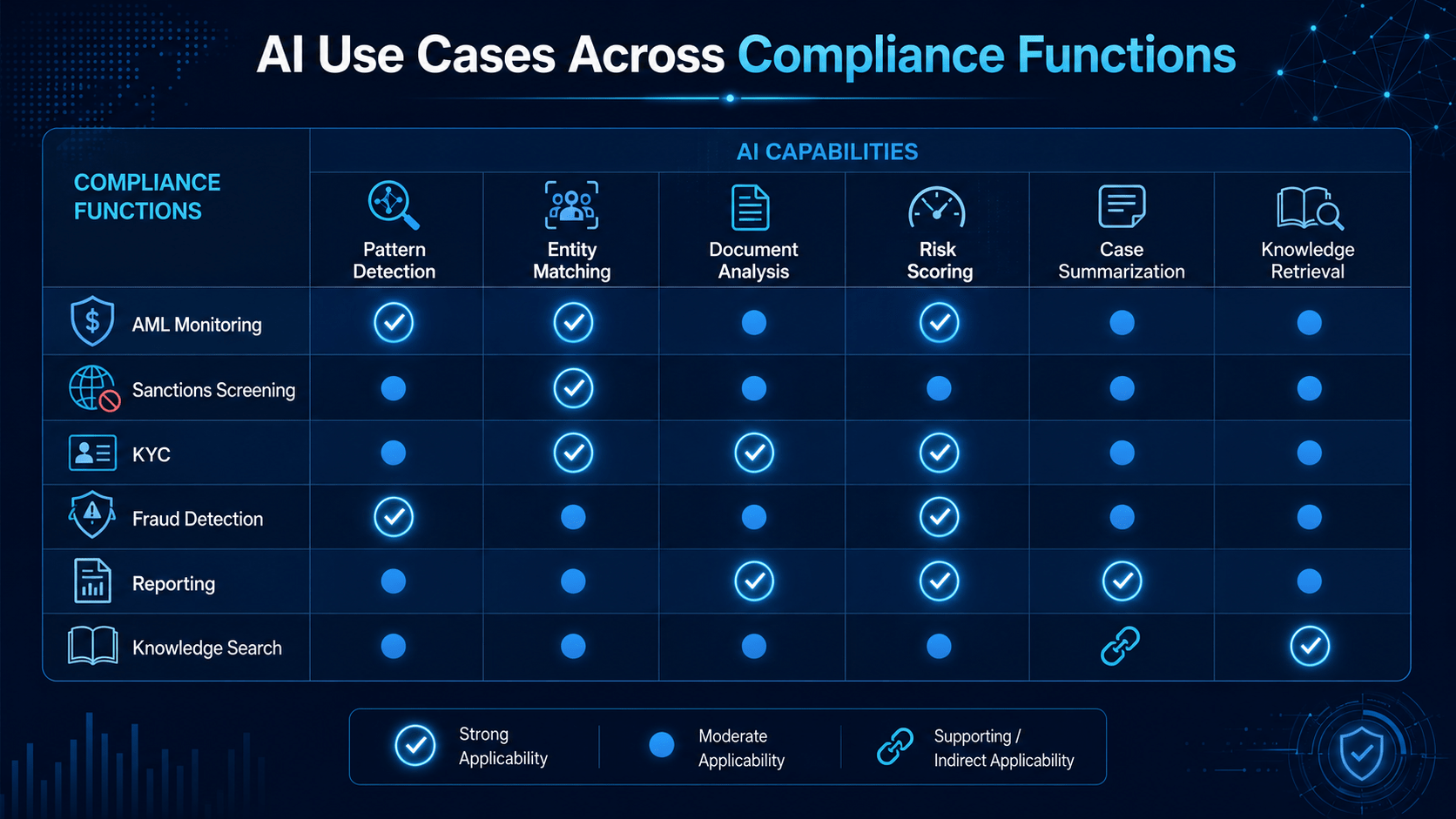

Key Use Cases of AI in Compliance

AI Supports High-Value Compliance Functions

AI can support compliance teams across several high-value use cases. In AML transaction monitoring, AI can help identify suspicious patterns, prioritize high-risk activity, and reduce unnecessary reviews. In sanctions and watchlist screening, AI can help reduce false matches by analyzing name variations, entity relationships, geography, and supporting context. In KYC and customer due diligence, AI can validate documents, detect inconsistencies, summarize customer profiles, and support risk scoring. In fraud detection, AI can identify abnormal behavior across transactions, devices, accounts, and customer networks. This is especially relevant to fintech companies, where fraud prevention, onboarding speed, and customer experience are deeply connected. SmartDev has explored these trends further in our article on AI use cases in fintech.

AI Helps Analysts Find and Use Compliance Knowledge Faster

AI can also support regulatory reporting and compliance knowledge search. Analysts often need to draft case narratives, prepare internal reports, locate policy documents, compare previous decisions, and retrieve regulatory guidance. AI assistants can reduce the time spent searching through documents and help teams access institutional knowledge faster. For large financial organizations, this can be a major advantage because compliance knowledge is often spread across documents, systems, teams, and geographies.

AI Use Cases Need the Right Technical Architecture

However, these use cases only create value when implemented with the right architecture. AI must integrate with existing tools, follow clear governance rules, and support human review. That is why AI-powered software development is essential. Compliance automation is not just about choosing a model. It is about building reliable, secure, explainable, and integrated software around that model.

How to Implement AI in Compliance Without Creating New Risk

Start with a Focused Workflow

AI in compliance should start with a focused workflow, not a vague transformation project. Good starting points include AML alert triage, KYC document review, sanctions false match review, fraud case summarization, or compliance knowledge search. These workflows are high-volume, measurable, and painful enough to justify automation. Starting narrow also makes it easier to define success metrics, manage governance, and prove value before scaling.

Keep Humans in the Loop

Human-in-the-loop design is also essential. High-risk cases should remain under human review, and escalation rules must be clearly defined. Every AI-supported decision should show which data sources were used, which risk factors influenced the recommendation, why the case was prioritized, what evidence was reviewed, who made the final decision, and what action was taken. IBM’s 2025 Cost of a Data Breach report also emphasizes the risks of rapid AI adoption without proper security and governance, which reinforces the need for controlled implementation rather than uncontrolled AI experimentation. (IBM)

Integrate AI with Existing Compliance Systems

Integration is another critical requirement. AI must connect with the systems compliance teams already use, including core banking platforms, CRMs, case management tools, KYC platforms, data warehouses, reporting systems, and internal knowledge bases. Without integration, AI becomes just another dashboard. With integration, AI becomes part of the operating workflow. This is why SmartDev often recommends a practical roadmap approach, as discussed in our guide on choosing the right workflow automation approach.

Monitor and Improve the Workflow Over Time

Finally, AI workflows must be monitored and improved over time. Customer behavior changes. Fraud patterns evolve. Regulations shift. Products expand. Data quality improves or deteriorates. A workflow that works today may need refinement tomorrow. This is why managed AI operations are more valuable than one-time implementation. Organizations need continuous optimization, not just initial deployment.

Where NORA Comes In: From Alert Overload to AI-Powered Compliance Workflows

Compliance Teams Need Workflow Orchestration, Not Another Isolated Tool

The compliance challenge is rarely caused by one missing tool. More often, the problem is that alerts, data, decisions, and documentation are scattered across too many systems. Analysts have to move between platforms, collect information manually, interpret risk signals, write summaries, escalate cases, and record decisions. This creates friction at every step. NORA is designed to address this type of operational challenge.

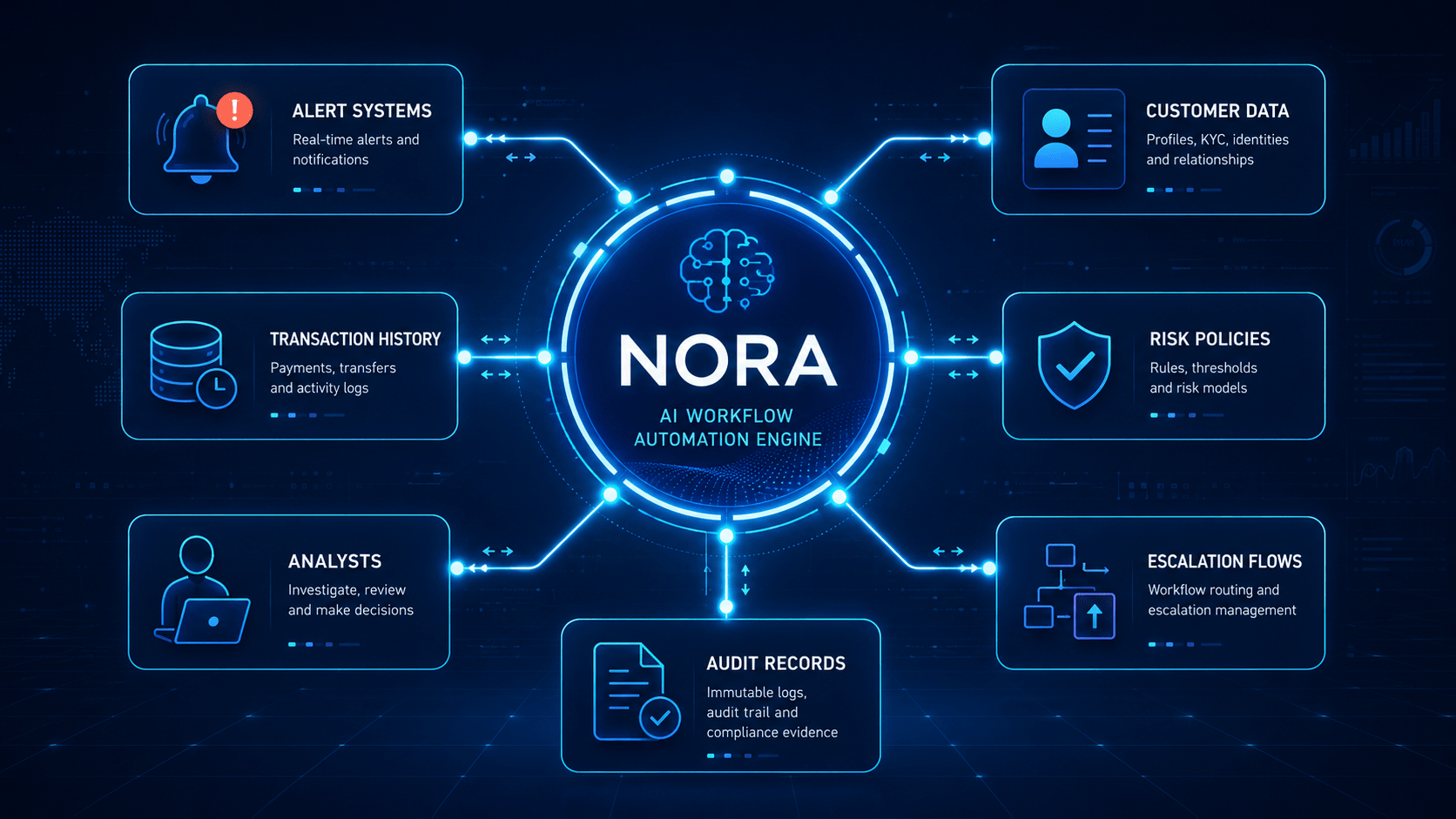

NORA Connects AI Capabilities with Real Compliance Workflows

NORA is SmartDev’s AI Workflow Automation Engine. It helps businesses connect AI capabilities into real operational workflows, so teams can automate repetitive work, improve decision-making, and keep humans in control where accountability matters. For compliance teams, NORA can support alert triage and prioritization by classifying cases based on risk level, urgency, and required action. It can also support case enrichment by pulling relevant data from internal systems, including customer profiles, transaction history, KYC information, previous cases, and internal policies.

NORA Helps Analysts Move from Fragmented Review to Guided Investigation

NORA can also generate investigation summaries, helping analysts understand what happened, why the alert was triggered, what looks normal, what looks unusual, and what information may still be missing. More importantly, NORA can help orchestrate the workflow around the investigation, connecting steps such as alert intake, enrichment, review, escalation, approval, documentation, and reporting. This makes NORA different from a standalone AI tool. It is not about adding another dashboard. It is about helping compliance teams move from fragmented investigation to AI-powered workflow execution.

NORA Keeps Human Accountability at the Center

For compliance use cases, human-in-the-loop control is central. NORA can be designed so analysts and compliance officers remain responsible for final decisions, while AI supports them with context, summaries, recommendations, and documentation. NORA can also help capture decision logic, supporting evidence, reviewer actions, and final outcomes for audit readiness. Over time, these workflows can be refined to reduce repetitive manual work and improve operational efficiency. This aligns with SmartDev’s broader experience in AI transformation roadmaps for financial institutions AI transformation roadmaps for financial institutions and AI in finance functions.

Conclusion: AI Will Not Eliminate Compliance Work. It Will Change What Compliance Teams Spend Time On

Compliance teams are not drowning because they lack effort. They are drowning because legacy systems generate too many alerts with too little context. False positives create real business costs by increasing manual work, slowing customer onboarding, creating analyst fatigue, and making real risks harder to identify. AI can help, but only when implemented correctly.

The real value of AI in compliance is not simply fewer alerts. The value is better context, smarter prioritization, faster investigation, stronger documentation, and clearer human decision-making. That is why the future of compliance is not just alert automation. It is investigation orchestration.

With NORA, SmartDev helps organizations move from alert overload to AI-powered workflows that are faster, more scalable, and easier to control.

Ready to reduce compliance noise and build smarter AI-powered workflows? Explore how SmartDev’s NORA can help your team move from fragmented investigations to faster, more defensible decisions. Find more about NORA’s capability in financial compliance in here