TL;DR

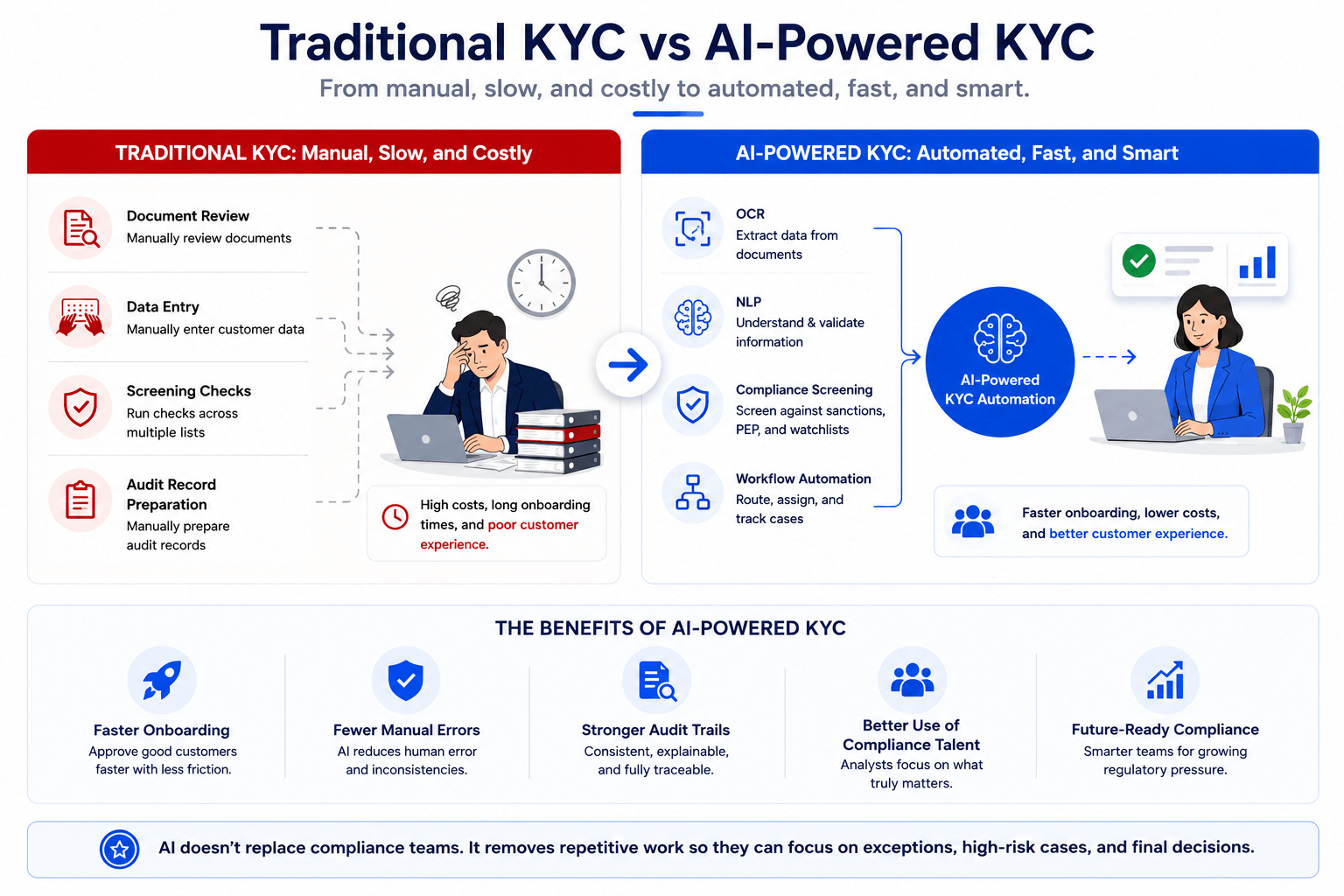

- Traditional KYC is slow because teams must manually review documents, enter data, run screening checks, and prepare audit records. This creates high costs, long onboarding timelines, and poor customer experience.

- AI-powered KYC automation speeds up the process by using OCR, NLP, workflow automation, and compliance screening to extract, validate, screen, and route customer information with less manual effort.

- The best model is not full replacement, but human-in-the-loop automation. AI handles repetitive work, while compliance teams focus on exceptions, high-risk cases, and final decisions.

- SmartDev’s NORA helps financial institutions build faster, more auditable KYC workflows by automating document review, risk assessment, screening, case routing, and audit trail generation.

Introduction

The average bank spends $1,500 to $3,000 to complete a single client’s KYC review. Automated systems can verify customer information in under 30 seconds. That gap explains why KYC document review has become one of the clearest use cases for AI workflow automation in financial services.

According to Fenergo, 54% of banks spend $1,500–$3,000 per manual KYC review, while 21% spend more than $3,000 per client. The cost is also commercial: Fenergo reports that 70% of financial firms lost clients because onboarding was too slow, up from 48% in 2023.

AI-powered KYC automation changes the equation by replacing manual document review, identity verification, sanctions screening, and risk routing with faster digital workflows. AU10TIX reports that automated KYC can reduce processing costs by up to 70% and cut verification time by 78%. Meanwhile, Mordor Intelligence projects the global KYC market to grow from USD 6.73 billion in 2025 to USD 16.31 billion by 2031.

This article explores how AI workflow automation processes KYC onboarding packs in minutes instead of days, and where financial organizations can gain the most in speed, cost efficiency, and compliance consistency.

The Growing KYC Bottleneck

Customer onboarding has evolved dramatically over the past decade. Customers now expect digital-first experiences and near-instant account opening. At the same time, regulators continue to expand compliance obligations around anti-money laundering (AML), sanctions screening, customer due diligence, and ongoing monitoring.

These competing pressures create a difficult challenge for compliance teams.

A typical onboarding package may include:

- Passports or government-issued IDs

- Proof of address documents

- Bank statements

- Corporate registration certificates

- Beneficial ownership documentation

- Tax records

- Source of funds information

Each document must be reviewed, validated, and compared against information provided elsewhere in the application. Analysts must then conduct multiple screening checks before determining whether the customer presents an acceptable level of risk.

The result is a workflow that is highly repetitive, labor-intensive, and difficult to scale.

When onboarding volumes increase, organizations often respond by hiring additional compliance analysts. While this may temporarily relieve pressure, it does not address the underlying inefficiencies. Costs continue to rise, onboarding delays increase, and customer experience suffers.

A report from McKinsey notes that financial institutions can spend significant operational resources on onboarding and compliance activities, making automation a strategic priority for improving efficiency and customer experience.

Organizations looking to reduce these bottlenecks often implement AML workflow automation and adopt a risk-based customer due diligence framework to focus resources on higher-risk cases.

What Is KYC Document Review Automation?

KYC document review automation refers to the use of artificial intelligence and workflow orchestration technologies to automate the collection, extraction, validation, screening, and routing of customer onboarding documents. Rather than relying on analysts to perform every step manually, AI-powered systems can process large portions of the workflow automatically.

The technology stack typically combines:

Intelligent Document Processing (IDP)

AI models automatically classify incoming documents and identify relevant information. Learn more about how intelligent document processing for banking helps financial institutions automate document-heavy workflows.

Optical Character Recognition (OCR)

OCR converts scanned documents and images into machine-readable text. In KYC workflows, this is essential because many onboarding files still arrive as passport scans, ID card photos, bank statement PDFs, utility bills, or corporate certificates. Without OCR, analysts must read these documents manually and re-enter customer information into internal systems.

With OCR, key information such as names, dates of birth, addresses, document numbers, expiry dates, company registration numbers, and tax identifiers can be captured automatically. This reduces the time spent on manual data entry and lowers the risk of typing errors, especially when teams handle high onboarding volumes. More advanced OCR systems can also process low-quality scans, rotated images, handwritten fields, and multi-language documents, making them particularly valuable for financial institutions operating across different markets.

However, OCR alone is not enough. It can read text, but it does not always understand what that text means. That is why OCR is usually combined with AI models and natural language processing to classify fields, interpret context, and validate information across documents.

Natural Language Processing (NLP)

NLP enables systems to understand and interpret information contained within documents. While OCR extracts the text, NLP helps determine what that text represents and how it should be used in the KYC process.

For example, NLP can help identify whether a phrase refers to a residential address, a company name, a beneficial owner, a source of funds statement, or a risk-related disclosure. In corporate onboarding, this is especially important because relevant information may be buried inside long documents such as business registration files, ownership structures, board resolutions, or shareholder declarations.

NLP also supports consistency checks across the onboarding pack. It can compare names, addresses, entity details, and ownership information across multiple documents and flag mismatches for review. For compliance teams, this means less time spent searching through files and more time spent assessing actual risk.

In more advanced workflows, NLP can also support adverse media screening, case narrative generation, and internal policy search. This allows analysts to retrieve relevant information faster, draft review notes more consistently, and make decisions based on a clearer view of the customer profile.

Workflow Automation

Automation platforms coordinate tasks, trigger compliance checks, route exceptions, and maintain audit trails. Instead of relying on analysts to manually move files from one stage to another, automation platforms trigger the next action based on predefined rules, risk scores, document status, or screening results.

For example, once a customer uploads documents, the workflow can automatically trigger OCR extraction, send extracted data for validation, initiate sanctions and PEP screening, calculate a preliminary risk score, and route the case to the right reviewer. Low-risk cases may move toward approval faster, while high-risk cases can be escalated to senior compliance officers or enhanced due diligence teams.

This matters because many KYC delays are not caused by one difficult task, but by handoffs between systems, teams, and approval layers. Workflow automation reduces these gaps by ensuring that cases do not sit idle in inboxes, shared folders, or manual queues.

It also improves auditability. Every action, decision, exception, reviewer comment, and approval can be recorded automatically. For regulated financial institutions, this creates a stronger audit trail and makes it easier to demonstrate that KYC checks followed a consistent, documented process.

Together, OCR, NLP, and workflow automation form the operational backbone of AI-powered KYC document review. OCR reads the documents, NLP understands the information, and workflow automation moves the case through the right compliance path with less manual effort.

At SmartDev, we built NORA, an AI adoption accelerator that helps financial institutions turn compliance automation from pilot ideas into production-ready workflows.

For KYC onboarding, NORA supports document ingestion, data extraction, customer validation, sanctions and PEP screening, risk assessment, case routing, and audit trail generation. Routine checks are automated, while compliance teams remain in control of complex decisions and final oversight.

By combining AI, workflow automation, and a human-in-the-loop approach, NORA helps banks, fintechs, and other regulated firms reduce manual workload, accelerate onboarding, and build more consistent, auditable compliance processes.

To explore more the power of NORA, click here

Compliance Screening Engines

These systems perform sanctions screening, PEP screening, adverse media checks, and AML risk assessments. Organizations increasingly rely on sanctions screening automation to accelerate compliance reviews.

Compliance screening engines are responsible for identifying potential regulatory, financial crime, and reputational risks associated with a customer before an account is approved. In traditional onboarding processes, analysts often perform these checks manually across multiple databases and systems, making screening one of the most time-consuming stages of KYC review.

Modern screening engines automate this process by comparing customer information against a wide range of risk data sources simultaneously. These typically include sanctions lists published by organizations such as OFAC, the United Nations, and the European Union; politically exposed person (PEP) databases; watchlists; adverse media sources; and internal risk databases maintained by the institution.

When a potential match is detected, the system automatically generates an alert and provides supporting information for review. More advanced platforms can use AI and fuzzy matching techniques to identify variations in names, spelling differences, aliases, and multilingual records that might be missed by simple exact-match searches. This helps reduce the risk of overlooking high-risk individuals while also lowering the number of false positives that compliance teams must investigate.

Compliance screening engines can also contribute to AML risk assessments by incorporating factors such as customer geography, industry sector, ownership structure, transaction profile, and screening results into a broader risk-scoring framework. Rather than treating every customer as equally risky, organizations can apply a risk-based approach that focuses compliance resources where they are needed most.

Together, intelligent document processing, OCR, NLP, workflow automation, and compliance screening engines create an end-to-end onboarding workflow that requires significantly less manual intervention. Documents can be collected, interpreted, validated, screened, risk-scored, and routed automatically, while compliance professionals remain focused on exceptions, investigations, and final decision-making. The result is a KYC process that is faster, more consistent, and better equipped to handle growing onboarding volumes without sacrificing regulatory oversight.

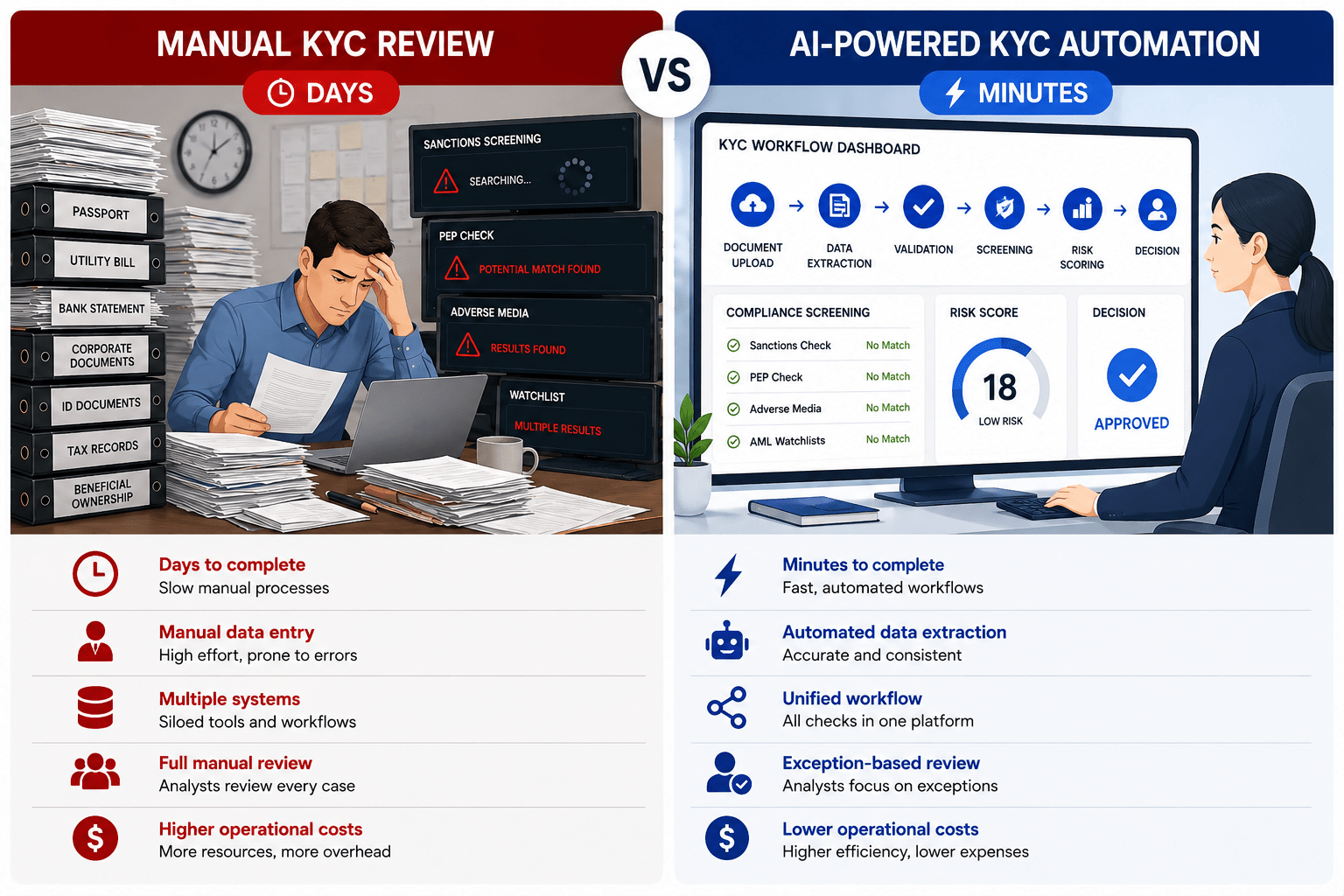

Why Traditional KYC Reviews Take Days

Before examining the automated workflow, it is important to understand why conventional KYC processes often become bottlenecks. Manual KYC is not slow because compliance teams lack efficiency. It is slow because the process depends on too many sequential, document-heavy, and human-led steps.

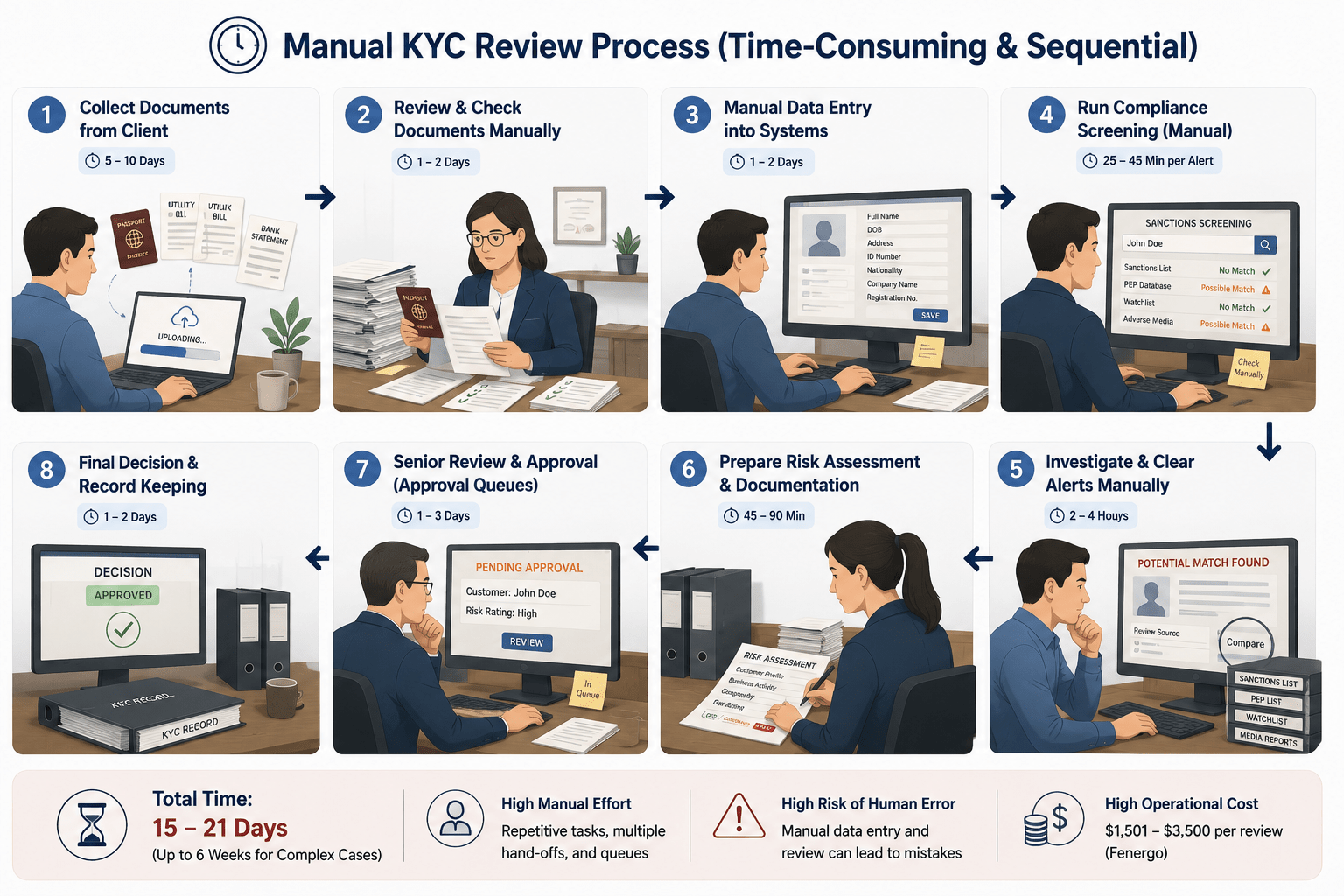

The scale of the delay is significant. According to Fenergo, 40% of banks take 31 to 60 days to complete a KYC review for a single corporate client. One fifth take up to 150 days, while 8% take up to 210 days. Wecan Group also notes that manual KYC onboarding typically takes 15 to 21 days for standard clients and up to 6 weeks for complex corporate structures.

Large Volumes of Documentation

Even straightforward customer applications may require multiple supporting documents, including passports, proof of address, bank statements, corporate registration documents, tax records, and beneficial ownership information. For corporate onboarding, the process becomes even more complex because one client may involve several legal entities, directors, authorized signatories, and ultimate beneficial owners across multiple jurisdictions.

Wecan Group estimates that document collection alone can take 5 to 10 days in a manual onboarding process, especially when clients submit incomplete files, wrong formats, or documents that require repeated follow-ups.

Repetitive Data Entry

Analysts frequently copy information from documents into internal systems. Names, addresses, identification numbers, registration details, and ownership information must often be entered manually into core banking systems, compliance platforms, and document management tools.

This creates two problems: it slows the process down and increases the risk of human error. Fenergo found that 90% of surveyed banks said their existing KYC process, with its potential for human error, affects their ability to make better risk decisions.

Multiple Compliance Checks

Customer information must be screened against numerous data sources, including global sanctions lists, PEP databases, watchlists, adverse media sources, and internal risk databases.

In manual workflows, these checks often happen across separate systems. Analysts must switch between tools, search names manually, review possible matches, and clear false positives. Wecan Group estimates that sanctions and PEP screening can take 25 to 45 minutes per alert, while UBO identification for corporate clients can take 2 to 4 hours.

Audit Documentation Requirements

Every onboarding decision must be documented and retained for future regulatory review. Analysts need to capture evidence, record findings, justify decisions, prepare risk assessments, and maintain detailed audit trails.

This administrative burden adds even more time. Wecan Group estimates that manual risk assessment drafting can take 45 to 90 minutes, while senior compliance officer validation may add another 1 to 3 days because files often sit in approval queues.

While these activities are essential for compliance, they make traditional KYC expensive and difficult to scale. Fenergo reports that two thirds of surveyed banks spend between $1,501 and $3,500 to complete a single KYC review. For institutions onboarding thousands of clients each year, this can quickly turn into millions of dollars in operational cost.

To address these challenges, many institutions are investing in financial crime prevention initiatives and deploying advanced AI document processing solutions. By automating document collection, data extraction, compliance screening, risk assessment, and audit trail generation, financial organizations can reduce onboarding from weeks to hours while allowing analysts to focus on higher-risk cases.

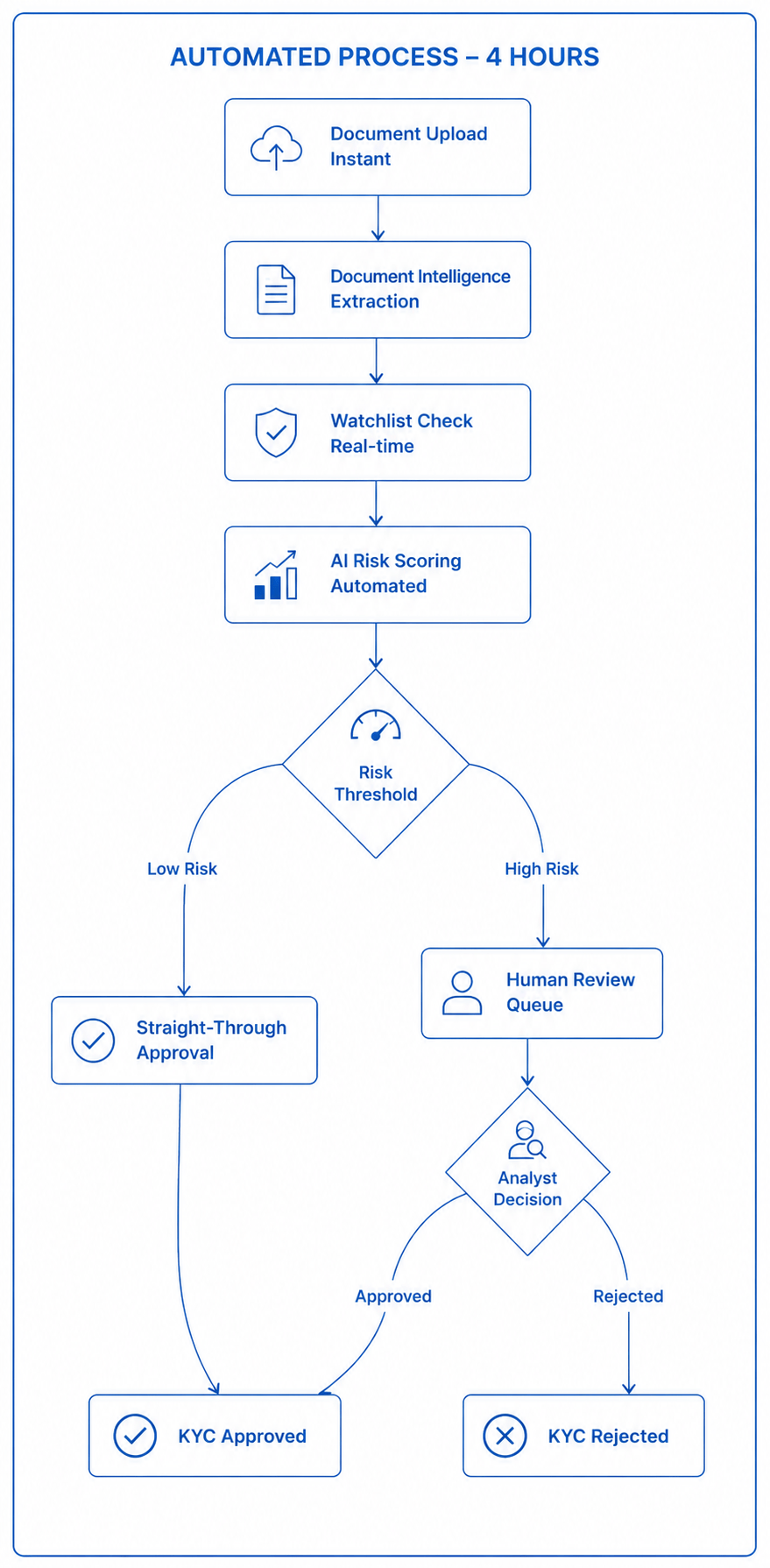

How AI Workflow Automation Processes KYC Packs in Minutes

Modern AI-powered onboarding workflows automate many of the most time-consuming activities traditionally performed by compliance teams. Instead of moving each file through a slow, sequential review process, AI allows document classification, data extraction, compliance screening, risk scoring, and case routing to happen almost instantly or in parallel. This is why automated KYC workflows can reduce onboarding from days to minutes for many standard applications. For example, Lorikeet notes that fintech teams using KYC automation have seen verification time drop from 18+ minutes to under 30 seconds, while Moxo reports that AI-powered eKYC processes can complete identity verification in around 35 seconds using biometric matching and real-time database screening.

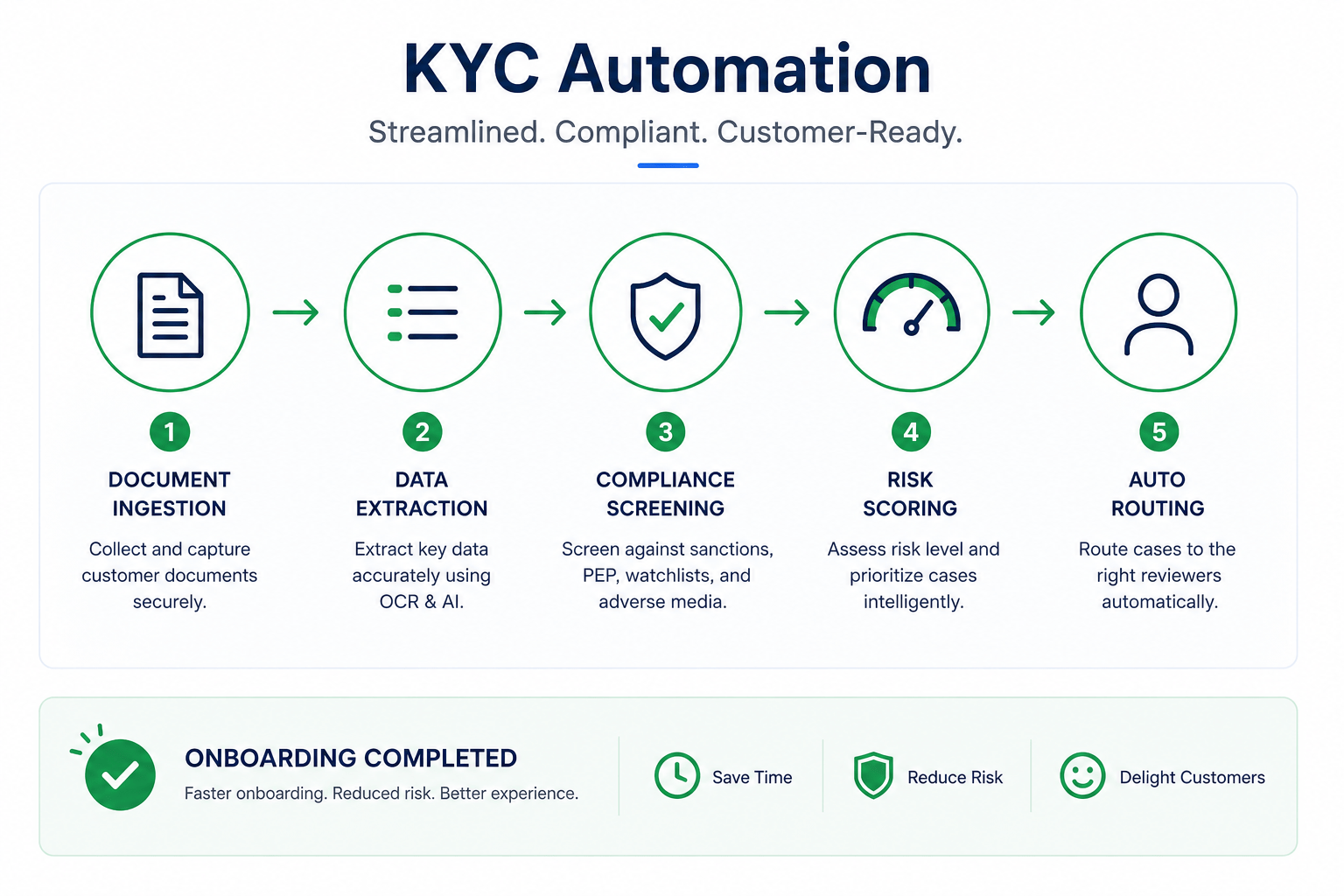

Step 1: Document Ingestion and Classification

The process begins when customers upload onboarding documents through a portal, mobile application, email channel, or CRM-integrated onboarding system. AI immediately analyzes incoming files and automatically classifies them by document type.

For example, the system can distinguish between passports, driver’s licenses, utility bills, bank statements, and corporate registration certificates. Instead of requiring analysts to open each file, check what it is, rename it, and move it into the right folder, AI can organize and route documents within seconds. This removes one of the first manual bottlenecks in KYC onboarding.

Step 2: Intelligent Data Extraction

Once documents are classified, OCR and AI models extract relevant information from each file. The system can automatically capture full name, date of birth, residential address, national identification number, business registration number, and company ownership details.

This is where automation creates a major time saving. According to IBM, intelligent document processing uses AI, OCR, and machine learning to extract, classify, and validate data from business documents, reducing the need for manual data entry. In KYC workflows, this means information that previously required analysts to read and transcribe manually can be captured in seconds and pushed directly into onboarding or compliance systems.

Step 3: Automated Validation and Consistency Checks

After extraction, AI compares information across the onboarding pack. It checks whether names match across submitted documents, addresses are consistent, identification numbers correspond correctly, and corporate information aligns with available records.

Any discrepancy is flagged for review. Instead of examining every document line by line, analysts only need to investigate exceptions. Infrrd notes that automated KYC verification allows customers to upload documents while AI reads and validates them in seconds, shortening onboarding from days to minutes.

Step 4: Automated Compliance Screening

The workflow then initiates compliance checks against multiple risk databases simultaneously. Screening may include sanctions screening, politically exposed person screening, adverse media screening, watchlist screening, and internal risk database checks.

This is significantly faster than manual screening because the system does not need to search each source one by one. AI-powered workflows can run checks in parallel and return consolidated results almost immediately. Moxo notes that AI-powered document processing can verify identity documents, cross-reference sanctions lists, and conduct background checks in seconds.

Step 5: Risk Scoring and Decision Support

Once screening results are available, AI models evaluate customer risk based on predefined criteria. These may include geographic location, industry sector, customer type, screening outcomes, document anomalies, and historical risk indicators.

Customers are then categorized according to risk level. Low-risk cases can be routed toward approval quickly, while medium- and high-risk cases are escalated to compliance specialists for enhanced review. Intellectyx reports that AI-powered KYC can reduce customer verification from 3–10 business days to under 5 minutes for many applicants, mainly because routine decisions no longer wait in manual review queues.

Step 6: Human-in-the-Loop Review

AI does not remove compliance professionals from the process. It changes where their time is spent. Instead of reviewing every onboarding pack manually, analysts focus on cases that actually require judgment, such as potential sanctions matches, suspicious document inconsistencies, high-risk customers, or escalated exceptions.

This exception-based model helps compliance teams process more cases without lowering control standards. V7 Labs describes AI KYC document verification as a way to reduce onboarding time from days to minutes while maintaining thorough verification standards and generating audit-ready documentation. In practice, this means automation handles the repetitive work, while humans remain responsible for complex decisions, risk interpretation, and final oversight.

Real case studies in the world: Citigroup Uses AI to Accelerate Client Onboarding and Compliance Reviews

Citigroup has deployed AI-driven document processing as part of its broader effort to modernize client onboarding and regulatory compliance operations. One of the key bottlenecks in onboarding was the manual review of customer documents before accounts could be opened. By introducing AI to automate document processing and data extraction workflows, the bank significantly reduced the time required for these reviews. According to Citigroup’s Head of Technology, the system cut document review time from more than one hour to approximately 15 minutes for onboarding activities within its services division. The initiative demonstrates how AI workflow automation can streamline compliance-heavy processes by reducing manual document handling, accelerating customer onboarding, and allowing teams to focus on higher-value compliance tasks rather than repetitive administrative reviews.

Transform KYC Reviews with NORA

As customer onboarding volumes grow and compliance requirements become increasingly complex, financial institutions can no longer rely on manual KYC processes to keep pace. The future of compliance lies in intelligent workflows that automate repetitive tasks while allowing analysts to focus on higher-value decisions.

NORA helps financial organizations streamline KYC document reviews through AI-powered workflow automation. From document ingestion and data extraction to sanctions screening, risk scoring, and audit trail generation, NORA automates the most time-consuming parts of the onboarding process while maintaining human oversight where it matters most.

By reducing manual reviews, accelerating customer onboarding, and improving compliance consistency, NORA enables banks, fintechs, payment providers, and insurance companies to process onboarding packs in minutes rather than days. Whether your goal is to reduce operational costs, improve customer experience, or scale compliance operations without expanding headcount, NORA provides a practical path toward faster, smarter, and more efficient KYC workflows.

Ready to see how AI-powered compliance automation can transform your onboarding process? Discover how NORA can help your team review more cases, faster, with less manual effort and greater confidence. Discover more about NORA in Finance and Compliance in here