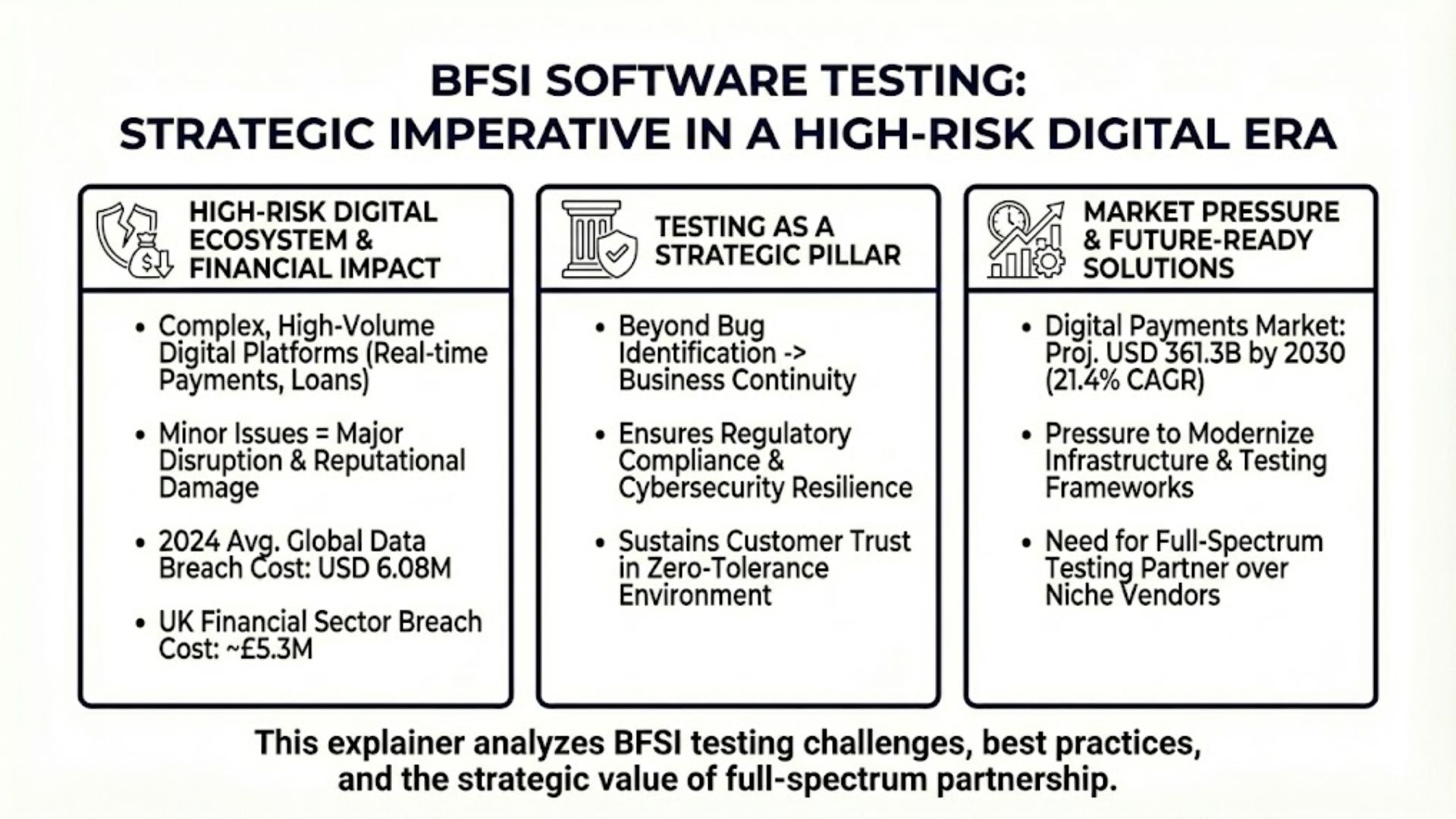

The rapid digital transformation of the Banking, Financial Services, and Insurance (BFSI) sector has created an increasingly complex and high-risk technology ecosystem. Today, millions of users access digital banking platforms simultaneously to transfer funds, check balances, apply for loans, and complete real-time payments. In such a high-volume environment, even a minor performance issue or a small security vulnerability can trigger significant operational disruption, financial loss, and reputational damage.

Recent 2024 industry reports reveal that the average cost of a data breach in the global financial services sector reached USD 6.08 million, significantly higher than the cross-industry average. In the UK market alone, financial institutions faced breach costs of approximately £5.3 million, compared to £3.4 million in non-financial industries. These figures underscore the elevated cybersecurity and compliance risks inherent in BFSI systems.

As a result, software testing for BFSI is no longer limited to identifying bugs before release. It has become a strategic pillar for ensuring business continuity, regulatory compliance, cybersecurity resilience, and sustained customer trust in a zero-tolerance environment. With the global digital payments market projected to reach USD 361.3 billion by 2030, growing at a 21.4% CAGR from 2025, financial institutions face mounting pressure to modernize both their banking infrastructure and their testing frameworks.

This Technology Explainer provides a comprehensive analysis of the technical challenges in BFSI testing, outlines best-practice testing methodologies, and explains why partnering with a full-spectrum software testing provider offers a more scalable and future-ready solution than relying solely on niche testing vendors in today’s digital-first financial landscape.

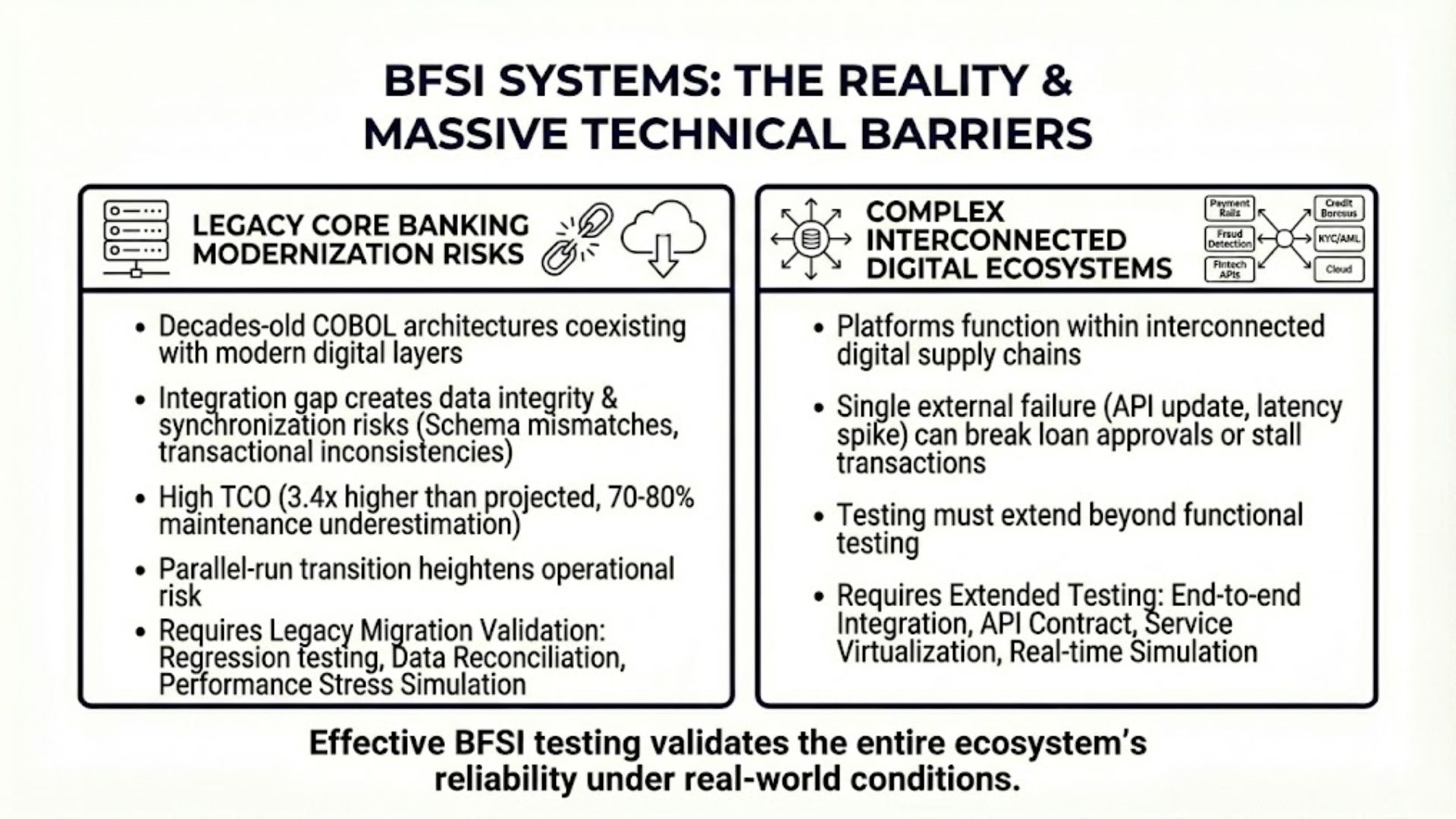

The Reality and Massive Technical Barriers in BFSI Systems

Software testing for BFSI operates in one of the most demanding technology environments in the world. Unlike consumer applications, BFSI platforms must balance real-time performance, extreme data sensitivity, regulatory scrutiny, and uninterrupted availability. This combination creates deep technical barriers that require testing strategies with wide system coverage, rigorous risk modeling, and continuous validation across the entire digital ecosystem.

Legacy Core Banking Modernization Risks

One of the most persistent challenges in software testing for BFSI is the coexistence of legacy core systems and modern digital layers. Many global banks still run mission-critical core banking platforms built on COBOL-based architectures developed decades ago. While stable, these systems were not designed for today’s API-driven, cloud-native, microservices-based ecosystems.

The integration gap between monolithic legacy systems and decentralized cloud databases creates significant data integrity and synchronization risks. Schema mismatches, batch-processing delays, and transactional inconsistencies can cascade across digital channels.

Financial institutions frequently underestimate the real Total Cost of Ownership (TCO) of maintaining legacy infrastructure. Studies show that actual IT costs can be up to 3.4 times higher than projected, with organizations underestimating maintenance costs by 70–80%. Although modernization initiatives can reduce TCO by 38–52%, the parallel-run transition phase introduces heightened operational risk.

Without comprehensive regression testing, data reconciliation validation, and performance stress simulation, modernization efforts can unintentionally disrupt payment processing, ledger accuracy, or reconciliation workflows. This is precisely why software testing for BFSI systems must include legacy migration validation frameworks, not just application-level testing.

Complex Interconnected Digital Ecosystems

Modern banking and insurance platforms do not operate in isolation. They function within highly interconnected digital supply chains that include:

- Payment rails

- Credit bureaus

- Fraud detection engines

- KYC/AML systems

- Third-party fintech APIs

- Cloud infrastructure providers

A single API version update from a credit scoring partner can break automated loan approvals. A latency spike in a payment gateway can stall thousands of transactions.

Effective software testing for BFSI must therefore extend beyond functional testing into:

- End-to-end integration testing

- API contract testing

- Service virtualization

- Real-time transaction simulation

- Production-like environment replication

Testing must validate not only whether each component works independently, but whether the entire ecosystem performs reliably under real-world traffic volumes and failure scenarios.

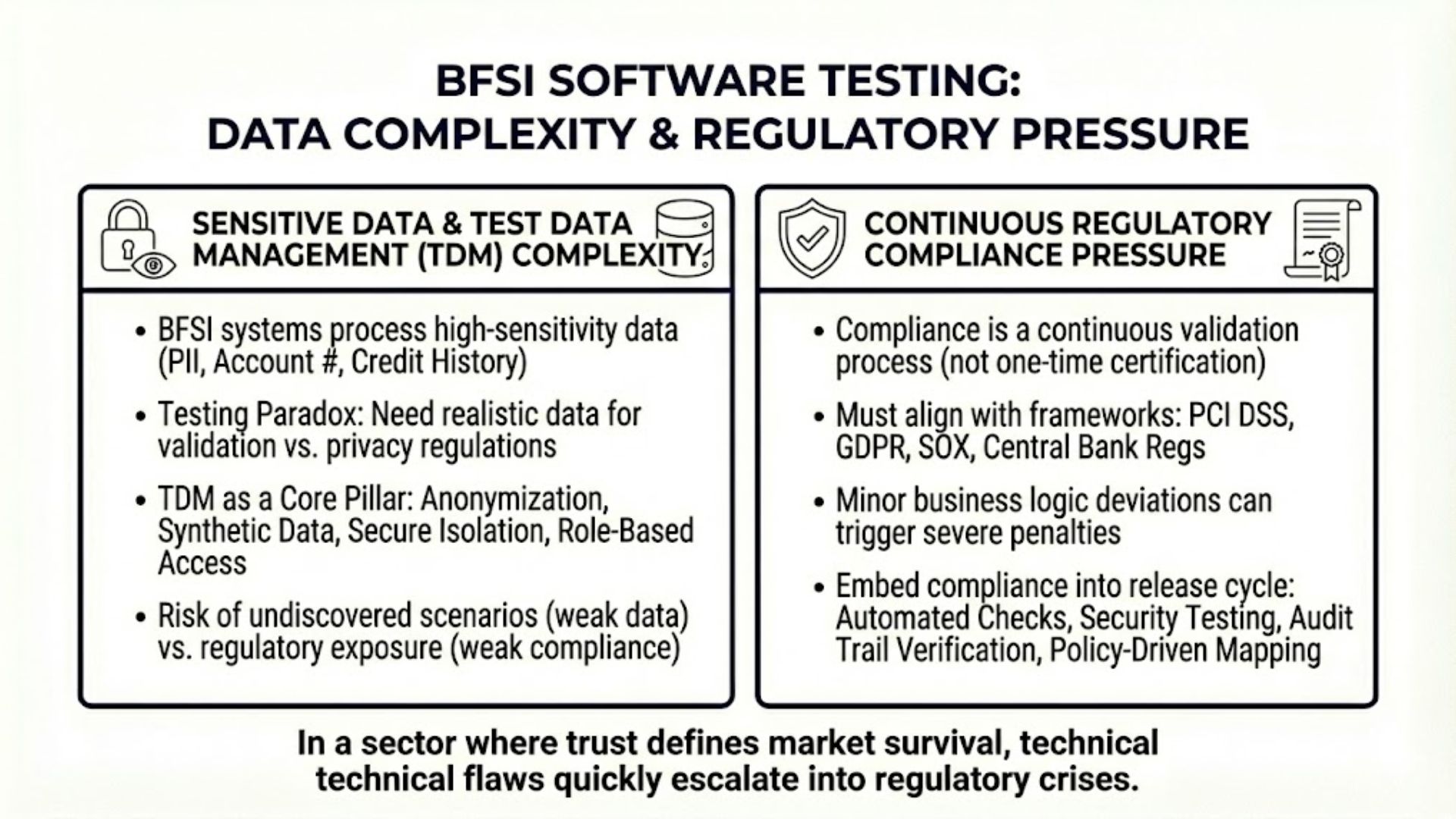

Sensitive Data and Test Data Management Complexity

BFSI systems process highly sensitive information including:

- Personally identifiable information (PII)

- Account numbers and transaction histories

- Investment portfolios

- Insurance contracts

- Credit histories

Testing in such environments presents a paradox: realistic data is needed for accurate validation, yet privacy regulations prohibit direct exposure of production data.

This makes Test Data Management (TDM) a core pillar of software testing for BFSI. Organizations must implement:

- Data anonymization and masking techniques

- Synthetic data generation

- Secure test environment isolation

- Role-based access controls

If test data lacks realism, risk scenarios remain undiscovered. If compliance controls are weak, regulatory exposure increases. The margin for error is effectively zero.

Continuous Regulatory Compliance Pressure

Regulatory compliance is not a one-time certification exercise. It is a continuous validation process. BFSI software must align with frameworks such as:

- PCI DSS for payment security

- GDPR for data protection in Europe

- SOX for financial reporting controls

- Central bank and domestic supervisory authority regulations

A minor deviation in business logic, such as incorrect transaction logging, flawed audit trails, or improper consent handling can trigger severe penalties and reputational damage.

Therefore, software testing for BFSI must embed compliance validation into every release cycle, including:

- Automated compliance checks

- Security testing and vulnerability scanning

- Audit trail verification

- Policy-driven test case mapping

In a sector where trust defines market survival, technical flaws quickly escalate into regulatory crises.

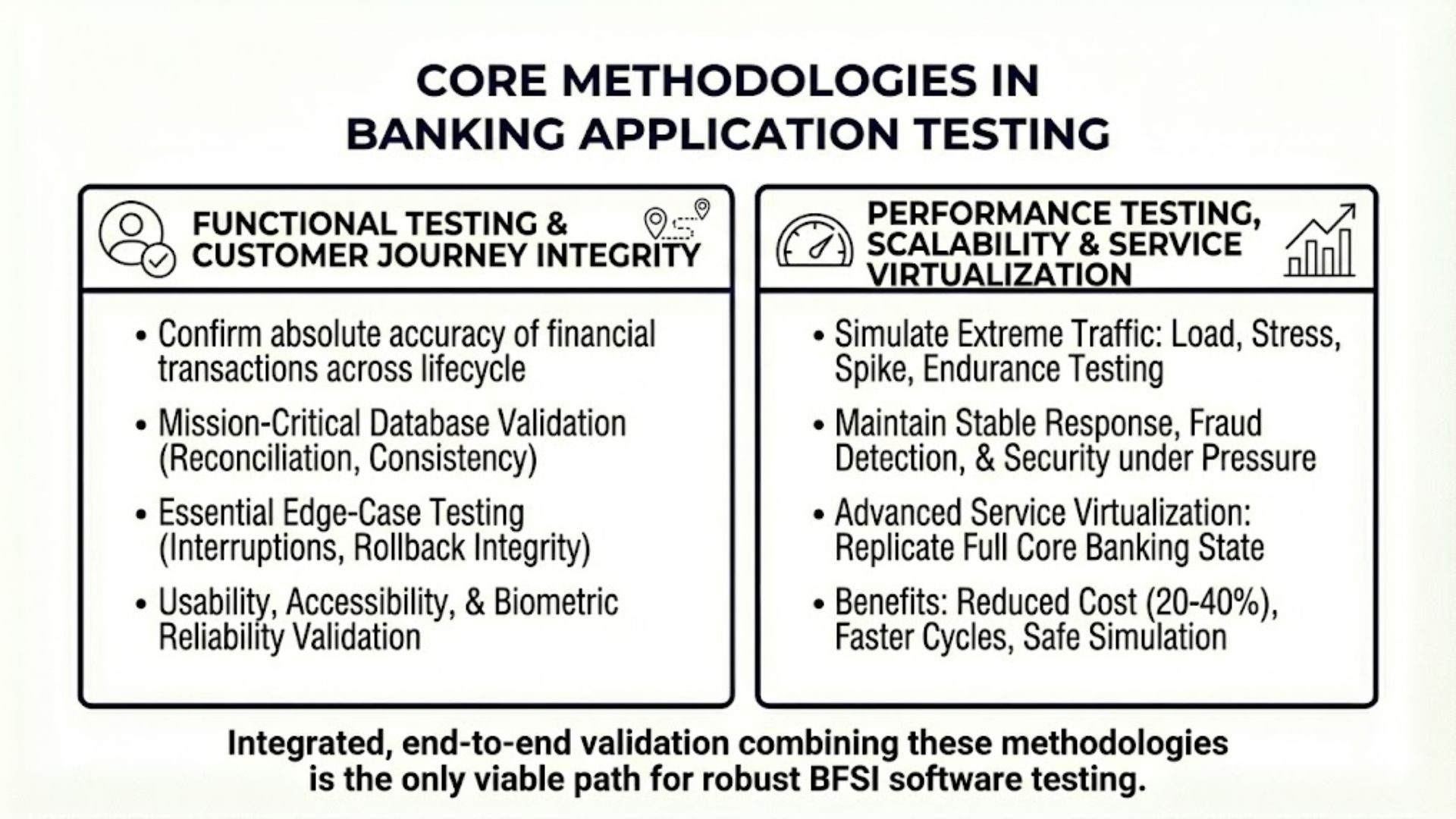

Core Methodologies in Banking Application Testing

To overcome the structural risks discussed earlier, a robust software testing for BFSI strategy must combine multiple specialized testing methodologies. These approaches span across user interfaces, middleware layers, core banking engines, APIs, databases, and regulatory logic. In highly regulated financial environments, fragmented testing is dangerous. Integrated, end-to-end validation is the only viable path.

Functional Testing and Customer Journey Integrity

In software testing for BFSI, functional validation extends far beyond verifying screen-level interactions. It requires confirming the absolute accuracy of every financial transaction across the entire customer lifecycle — from login authentication and account overview to fund transfers, loan applications, and bill payments.

Every transaction must be:

- Recorded accurately in backend databases

- Reconciled correctly between debit and credit accounts

- Free from duplication or orphan records

- Stored in correct formats with validated constraints

Database validation becomes mission-critical. QA teams must rigorously test:

- Primary key and foreign key constraints

- Unique indexes and ledger balances

- Null rejection rules in mandatory fields

- Data consistency across distributed systems

Even a minor discrepancy can result in financial imbalance, regulatory violations, or reputational damage.

Edge-case testing is equally essential. BFSI applications must be validated against:

- Network interruptions mid-transaction

- High latency environments

- Database timeouts

- Partial transaction failures requiring rollback

Atomicity and rollback integrity must be verified to ensure no “half-completed” financial operations occur.

In 2024–2025, usability testing has also become central to software testing for BFSI, especially for mobile banking. Financial institutions must validate responsive design, accessibility compliance, biometric login reliability, and cross-device consistency. Customer trust depends on seamless experience as much as transactional accuracy.

Performance Testing, Scalability, and Service Virtualization

Financial platforms routinely face extreme traffic spikes — salary disbursement days, end-of-quarter closing cycles, flash sales, or Black Friday events.

Effective software testing for BFSI must include:

- Load testing to simulate expected peak usage

- Stress testing beyond projected capacity

- Spike testing for sudden transaction bursts

- Endurance testing for prolonged high activity

The system must maintain:

- Stable response times

- Fraud detection accuracy

- Authentication reliability

- Transaction consistency under pressure

A common risk under load is silent degradation — where fraud detection algorithms slow down or security controls weaken. Testing must verify that security layers remain intact even during peak volumes.

To conduct such testing without risking production systems, Service Virtualization has become a standard methodology. Unlike basic API mocking, advanced virtualization tools replicate the full behavioral state of core banking systems, including account balances and regulatory logic.

Benefits include:

- Reduced infrastructure cost (often 20–40%)

- Parallel development across teams

- Safe simulation of expensive core banking dependencies

- Faster integration testing cycles

For large banks modernizing legacy systems, service virtualization is no longer optional — it is foundational.

API and Payment Gateway Testing: Validating Business Logic

Open Banking ecosystems rely heavily on APIs. However, in software testing for BFSI, validating HTTP status codes is insufficient. The true risk lies in business logic vulnerabilities.

Testing must simulate real attack vectors and transactional manipulation attempts.

Critical API testing scenarios include:

- Intercepting a $1.00 transaction and modifying it to $0.01 to validate server-side validation

- Attempting to bypass authentication flows by directly calling payment endpoints

- Simulating race conditions by sending simultaneous transactions within milliseconds

- Verifying row-level locking to prevent double-spending or duplicate deductions

Automated tools are effective for coverage, but specialized manual testing remains essential for detecting business logic flaws.

Payment gateway testing must validate full transaction lifecycles:

- Successful payments

- Failed transactions (invalid card, insufficient funds)

- Pending or delayed settlement states

- Reversals and chargebacks

Without comprehensive API validation, financial institutions risk fraud exposure and regulatory non-compliance.

Data Migration and ETL Testing in Banking Modernization

Digital transformation initiatives often involve migrating massive volumes of financial data from legacy systems to cloud-based architectures. This is one of the highest-risk phases in banking modernization.

Poorly executed migrations have led to multi-million-dollar losses due to:

- Incomplete dependency mapping

- Big-bang migration strategies

- Unvalidated data transformations

- Ledger mismatches

A mature software testing for BFSI framework must incorporate structured Data Migration and ETL testing.

Migration Models

Phased Migration

Data and modules are migrated step-by-step, reducing business disruption but requiring complex synchronization management.

Parallel (Pilot) Migration

Legacy and new systems run simultaneously for validation. This minimizes risk but increases operational cost temporarily.

ETL Testing Roadmap

A structured approach includes:

1. Planning and Data Mapping

- Conduct pre-migration data audits

- Create detailed field-level mapping documents

- Define transformation logic

- Standardize data models to prevent schema drift

2. Extract Validation

- Confirm all required records are extracted

- Detect missing or duplicate data

3. Transform Validation

- Verify business rules and calculations

- Validate currency conversions and rounding logic

- Ensure proper format changes and data cleansing

4. Load Validation

- Confirm accurate insertion into target systems

- Validate referential integrity and ledger balances

5. Automated Reconciliation and Rollback Readiness

- Run reconciliation scripts comparing financial metrics

- Verify no discrepancies in balances or transaction histories

- Maintain a tested rollback plan for emergency recovery

In banking environments, reconciliation is non-negotiable. Financial accuracy must be provable.

Ready to modernize your BFSI systems and accelerate digital transformation?

SmartDev helps banks, insurers, and fintech companies build secure, scalable platforms powered by cloud, AI, and automation.

Turn strategy into production-ready solutions with a trusted BFSI technology partner.

Talk to a BFSI ExpertSecurity Standards Framework and Regulatory Compliance

Security testing is not just an add-on feature but a vital protective shield for any software testing for bfsi project. Financial systems are always the top targets for large-scale cyberattacks. Compliance is a prerequisite and non-negotiable. The security testing strategy must closely adhere to the strictest international and regional standards.

Payment Card Industry Data Security Standard (PCI DSS)

PCI DSS version 4.0.1 is the mandatory global security standard for any organization that processes, stores, or transmits payment card data. Failure to meet these requirements can lead to severe sanctions, fines, and revocation of card processing rights. To pass PCI DSS certification audits, the bank’s testing system must review and verify 12 strictly structured core requirements.

The table below illustrates the mapping between core PCI DSS requirements and corresponding security testing activities:

| PCI DSS Requirement Group | System Requirement Details | Testing and Compliance Review Activities |

| Secure Network Construction |

1. Install and maintain firewall configurations.

2. Remove vendor-supplied default passwords and security parameters. |

Scan network configurations to evaluate firewall rules; test Cardholder Data Environment (CDE) isolation via Network Segmentation tests; assess password strength against NIST standards. |

| Protect Cardholder Data |

3. Protect stored cardholder data (PAN).

4. Encrypt data transmission across open public networks. |

Verify the application of strong encryption algorithms (like AES-256 or RSA) and data masking techniques. Test transmission encryption protocols like TLS and prevent downgrading to vulnerable older SSL versions. |

| Vulnerability Management |

5. Regularly update anti-virus software and malware protection.

6. Develop and maintain secure systems/applications. |

Assess the system patching process; perform Static Application Security Testing (SAST) to detect and remediate software vulnerabilities during the development lifecycle; check secure application configurations. |

| Access Control Measures |

7. Restrict access to card data based on the “Need to know” principle.

8. Assign Unique IDs for access.

9. Strictly control physical access. |

Evaluate authorization logic; review user permissions based on the least privilege principle; test Multi-Factor Authentication (MFA) flows for all access to the CDE. |

| Network Monitoring and Testing |

10. Track and log all access to network resources.

11. Regularly test security systems and processes. |

Verify the integrity of audit logs; perform quarterly vulnerability scans; execute periodic annual Penetration Testing and segmentation testing every 6 months. |

| Maintain Information Security Policy | 12. Maintain an information security policy for all personnel and contractors. |

Review policy documents, assess the effectiveness of vendor management processes and Incident Response plans. |

Continuity in executing quarterly vulnerability scans and penetration testing is the backbone for maintaining compliance status between annual certification audits.

International Standards and Regulations in Vietnam (GDPR, SOX, SBV)

In regulated markets, software testing for BFSI must align closely with legal frameworks. Compliance is not a final step — it must be built into the testing lifecycle.

Under the General Data Protection Regulation (GDPR), systems must support the Right to Erasure, proper consent logging, and secure personal data processing. Testing must verify that data deletion requests fully remove information across all connected systems.

The Payment Services Directive 2 (PSD2) requires strict validation of Strong Customer Authentication (SCA). Testing must ensure multi-factor authentication, biometric flows, OTP verification, and fallback APIs operate reliably under failure conditions.

In the United States, the Sarbanes-Oxley Act (SOX) focuses on financial reporting integrity. Systems must be tested for tamper-proof audit trails, role-based access control, and transparent report generation that cannot be manipulated.

In Vietnam, regulations issued by the State Bank of Vietnam — particularly Circular 50/2024/TT-NHNN and Circular 77/2025/TT-NHNN — require risk-based transaction classification. High-risk transactions (Types C and D) must enforce biometric or digital signature authentication.

Testing must also verify non-repudiation logs, secure online banking operations, and proper data retention periods according to regulatory timelines.

Across all jurisdictions, software testing for BFSI must integrate automated compliance checks into every release. In financial services, regulatory alignment directly protects trust, stability, and long-term competitiveness.

Building Testing Capabilities via Maturity Models (TMMi & ISTQB)

To ensure the performance and quality of financial systems remain at their peak, standardizing QA teams’ workflows through renowned competency frameworks like the TMMi (Test Maturity Model integration) and the ISTQB (International Software Testing Qualifications Board) certification standard is a strategic, long-term move.

System Standardization with the TMMi Model

TMMi provides a staged architecture helping organizations improve their testing processes from a chaotic, undefined state (Level 1) to continuous optimization (Level 5). At Level 1, testing is often viewed as part of debugging, performed ad hoc after coding is completed, resulting in products being released without clear risk visibility. As an organization gradually upgrades its processes, defect detection efficiency and cost optimization increase exponentially.

Empirical data from TMMi applications across financial institutions including banks, clearing centers, insurance, and stock exchanges show the most common maturity levels are Level 3 (Defined) and Level 4 (Measured). The detailed breakdown below illustrates capability shifts as organizations ascend TMMi levels in BFSI software testing:

| TMMi Maturity Level | Identifying Characteristics | Test Case Reuse Rate | Defect Containment Efficiency | ROI and Benefits Recorded from Automation |

| Level 2 (Managed) | Basic testing methods are established, planned, and controlled for individual projects. Dedicated test environments exist. | 20% – 30% | 60% – 70% |

No notable ROI data recorded from large-scale automation. |

| Level 3 (Defined) | Organization-wide process standardization. Testing is deeply integrated into the SDLC from early stages. Periodic non-functional testing execution. | 40% – 60% | 75% – 85% |

Automation ROI: 150% – 200%.

Finance Industry Benefits: Release cycles reduced from 3 months to under 1 month; test execution time cut from 19 to 5 weeks; early defect detection rate increased by 25%. |

| Level 4 (Measured) | Managing the test process via quantitative metrics. Advanced product risk assessment and forecasting based on historical data. | 60% – 80% | 85% – 95% |

Automation ROI: 200% – 300%.

Finance Industry Benefits: Defect leakage to production decreased by over 50% in 3 years; pre-go-live defect detection rate exceeds 99%. |

| Level 5 (Optimization) | Optimized state. Continuous improvement based on metrics and integration of smart automation tools to prevent defects at the root. | > 80% | > 95% |

Finance Industry Benefits: Production defect detection rate maintains an excellent 98.73%, systems can self-assess and improve continuously. |

The above data strongly reaffirms that, within the BFSI environment, investing in mature testing processes directly correlates with reducing costs incurred from security flaws or system downtimes.

Professional Foundation with ISTQB Standards

Accompanying TMMi at the organizational level is the ISTQB certification system at the individual expert level. For testing professionals in the banking sector, the Foundation Level (CTFL v4.0) syllabus provides a common language and core methodologies regarding black-box, white-box techniques, and risk-based testing.

At more advanced levels, the Security Test Engineer certification equips professionals with skills to design and execute security tests, while supporting the integration of test results into an Information Security Management System (ISMS) for proactive risk management. The Test Automation Engineering (CTAL-TAE) certification shapes strategies for optimizing automation investments, designing test framework architectures to maximize coverage and achieve the highest ROI regardless of whether the organization uses Agile, DevOps, or Waterfall development methods.

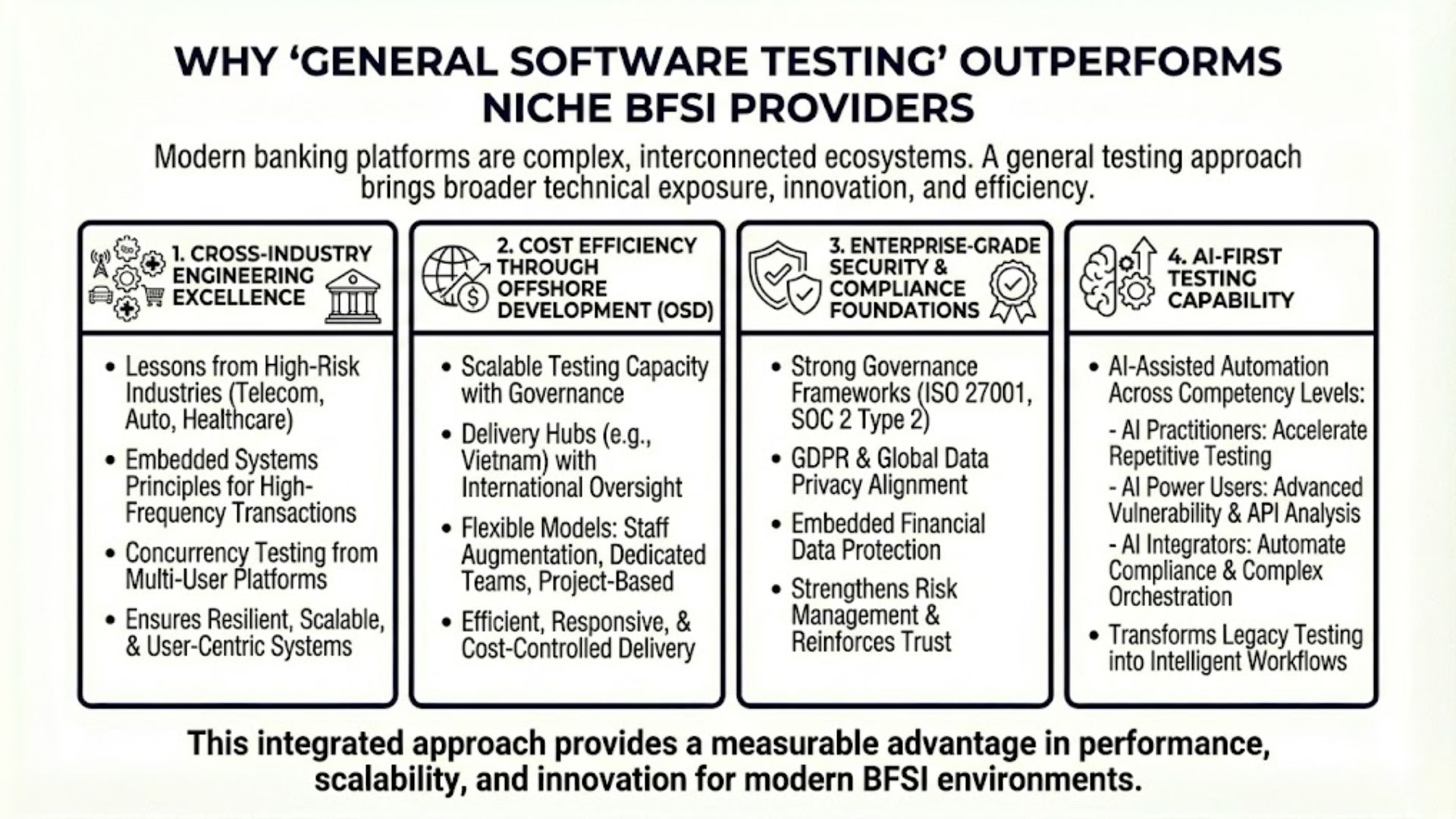

Why “General Software Testing” Outperforms Niche BFSI Providers: The SmartDev Advantage

When selecting a partner for software testing for BFSI, many banks instinctively choose niche providers that focus exclusively on financial systems. While this ensures regulatory familiarity, it often creates a strategic blind spot: limited cross-industry innovation and siloed thinking.

Modern banking platforms are no longer isolated ledger systems. They function as super-app ecosystems integrating payments, investments, e-commerce, identity verification, and third-party APIs. Solving performance, scalability, and security challenges in such environments requires broader technical exposure — not just financial domain knowledge.

1. Cross-Industry Engineering Excellence

A general testing partner brings lessons from high-risk industries such as telecommunications, automotive, healthcare, and large-scale consumer platforms.

For example, embedded systems testing in medical or telecom environments requires ultra-low latency, strict memory management, and fault tolerance. These same engineering principles strengthen high-frequency transaction systems and real-time payment architectures in banking.

Unlike traditional financial QA providers that adopt AI reactively, SmartDev integrates artificial intelligence at the core of its delivery methodology through its proprietary AI Delivery Blueprint. This structured framework embeds AI across every stage of the software development lifecycle (SDLC) and testing lifecycle (STLC).

SmartDev engineers are AI-ready from day one, supported by formal training programs such as the Coursera AI Learning Program. The result is a highly optimized AI-assisted QA pipeline that enhances both speed and quality.

Key capabilities include:

- Predictive Risk Scoring: AI analyzes historical defect patterns and code changes to automatically prioritize high-risk testing zones.

- Up to 50% reduction in manual QA workload across 300+ real-world projects.

- A structured 3-tier AI certification framework (AI Practitioners, AI Power Users, AI Integrators) to maximize productivity in automated script generation, self-healing UI testing, and compliance validation workflows.

For BFSI organizations, this means faster release cycles, reduced operational risk, and significantly improved time-to-market.

2. Cost Efficiency Through Offshore Software Development (OSD)

SmartDev’s QA excellence is validated by measurable results within the BFSI domain, particularly in insurance documentation systems and credit reporting platforms:

- 30.8% reduction in development time

- 1070% increase in pull request throughput

- Maintained high code quality rating (4.44/5)

These performance metrics demonstrate that comprehensive software testing in BFSI can simultaneously enhance compliance, productivity, and engineering efficiency.

The company’s innovation leadership has earned global recognition. SmartDev was named among the Top 100 Fastest-Growing Companies for 2025 by Clutch and received consecutive wins at the Sao Khuê Awards 2025 in categories including Outstanding Software Export Services and Outstanding AI Consulting Solution (for the VERA AI platform).

3. Enterprise-Grade Security and Compliance Foundations

One of the most powerful advantages of a general software testing partner is the ability to transfer optimization knowledge from other high-demand industries into financial systems.

SmartDev provides a comprehensive end-to-end testing suite, including:

- Automation Testing

- Manual Testing (UX/UI-focused validation)

- Performance & Load Testing

- Embedded Software Testing

- Security & DevSecOps integration

By applying real-time processing principles from medical embedded systems and concurrent load-testing strategies from ride-hailing platforms, SmartDev enhances ultra-low latency payment systems, digital wallets, and P2P transaction frameworks.

This cross-industry approach ensures that BFSI platforms are not only compliant and mathematically accurate but also deliver consumer-grade digital experiences—something purely niche financial QA vendors often struggle to achieve.

4. Enterprise-Grade Security via a Scalable Offshore Model (OSD)

Addressing the global DevSecOps talent shortage requires scalability without compromising data security or regulatory compliance. SmartDev operates a secure Offshore Software Development (OSD) model, combining engineering hubs in Vietnam (Hanoi and Da Nang) with global management presence in Switzerland, Singapore, the UK, and the US.

Flexible engagement models include:

- Staff Augmentation

- Dedicated Teams

- Project-Based Delivery

- Agile, Waterfall, or Hybrid methodologies

Security remains paramount. Backed by Swiss governance standards, SmartDev maintains:

- ISO 27001 certification

- SOC 2 Type 2 compliance

- Full adherence to GDPR and CCPA regulations

Strategic leadership from experienced executives ensures every QA initiative aligns with international financial compliance standards and enterprise-level governance expectations.

Conclusion

Software testing in the Banking, Financial Services, and Insurance sector has moved far beyond basic QA. Today, software testing for BFSI spans PCI DSS security validation, GDPR compliance checks, API virtualization, performance stress simulation, and legacy system reconciliation — all within highly regulated, high-risk environments.

As digital payments and Open Banking expand, cybersecurity threats and system complexity increase just as rapidly. Traditional, niche-focused testing approaches are no longer sufficient.

A General Software Testing partner with cross-industry expertise, offshore scalability, and an AI-First mindset enables financial institutions to modernize faster, strengthen compliance, and release secure products with greater efficiency. In short, a well-structured software testing for BFSI strategy is now a competitive advantage, not just a quality requirement.