TL;DR

- AI vendors are now enterprise third-party risks. Under MAS expectations, organizations stay accountable for vendor data handling, automated decisions, and critical processes.

- Traditional due diligence is no longer enough. Enterprises must assess AI-specific risks like transparency, governance, data usage, and human oversight.

- Auditors now expect AI governance evidence. This includes AI use, data protection, model governance, resilience, and supply chain risk.

- Governed AI workflows build trust. Audit trails, explainable outputs, human oversight, and compliance-ready evidence help enterprises adopt AI confidently.

Introduction

During audits, organizations must demonstrate not only the value of their AI solutions but also how they govern, secure, and oversee them. In the sections that follow, we examine why AI vendors are regarded as third-party risks under MAS expectations, outline the key areas auditors focus on, and discuss how organizations can develop AI strategies that strengthen regulatory confidence.

Why MAS treats AI Vendor as Third-Party Risk

The Monetary Authority of Singapore (MAS) is Singapore’s central bank and financial regulator, responsible for overseeing banks, insurers, capital markets, and other financial institutions. MAS guidelines apply broadly to regulated financial institutions operating in Singapore, including banks, payment service providers, asset managers, and fintech companies. A key expectation under MAS regulations is that these institutions must manage risks arising from outsourcing and third-party service providers – commonly referred to as third-party risk.

Third-party risk refers to the potential impact that external vendor or service providers can have on an organization’s operations, data security, compliance, and overall risk profile. When a financial institution relies on a vendor to perform critical functions or handle sensitive information, it remains accountable for any risks or failures that arise from that relationship.

As AI becomes increasingly embedded in enterprise software and managed services, these expectations naturally extend to AI vendors. Unlike traditional software, AI-powered solutions often process sensitive data, generate business recommendations, or automate decisions that were previously performed by employees. Many third-party vendors have also embedded AI capabilities into their products or internal service delivery without customers fully understanding when, where, or how AI is being used. This lack of visibility creates new risks around data governance, security, explainability, and regulatory compliance.

Traditional vendordue diligence is no longer sufficient. Reports such as SOC 2 or standard security questionnaires can demonstrate that a vendor has baseline security controls, but they rarely explain how AI models are used, what data they process, whether customer data is used for model training, or what safeguards exist to prevent inaccurate or unauthorized AI outputs. As a result, organizations must expand their third-party risk management programs to include AI-specific assessments, contractual disclosure requirements, and ongoing monitoring of AI use throughout the vendor relationship.

From an MAS perspective, the key concern is not simply whether an organization uses AI, but whether it understands and governs the risks that third-party AI vendors introduce. When an AI vendor influences critical operations or accesses regulated information, the organization must treat that vendor as part of its overall risk posture and evaluate it with the same rigor as any other critical service provider.

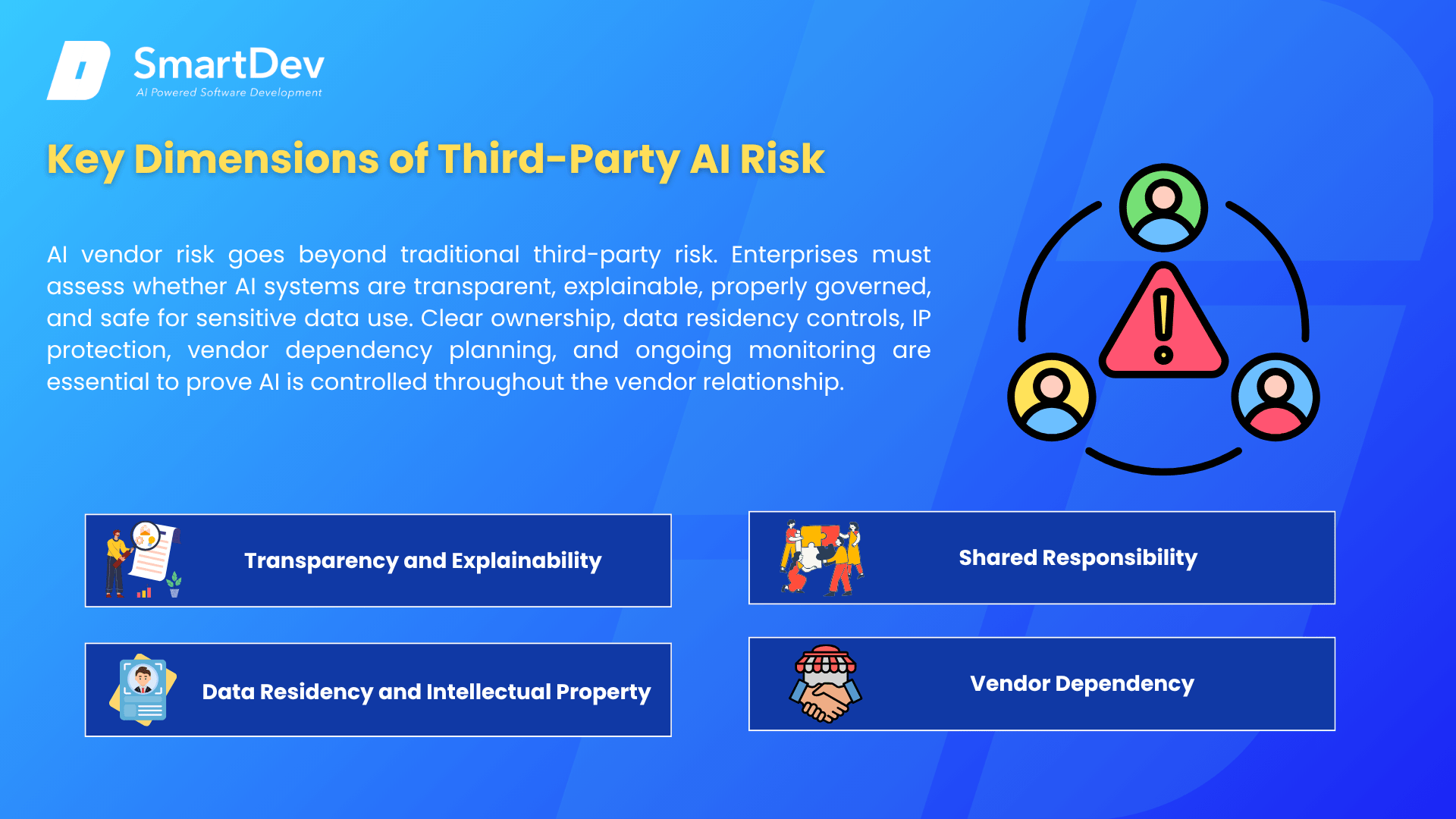

Key Dimensions of Third-Party AI Risk

Recognizing AI vendors as third-party risks is only the first step. Organizations must also understand what makes AI vendor risk fundamentally different from traditional third-party risk. Unlike conventional software, AI systems introduce additional challenges around transparency, accountability, and long-term governance that are not always captured through existing vendor assessments.

Transparency and Explainability

One of the biggest challenges is the “black box” nature of many AI models. Organizations can observe the outputs an AI system generates but often have little visibility into the underlying models, training data, or decision logic. This makes it difficult to independently assess whether AI-generated outcomes are accurate, unbiased, secure, and compliant with regulatory expectations. Without sufficient transparency, organizations may struggle to justify AI-assisted decisions during regulatory reviews or audits.

Shared Responsibility

Using a third-party AI service does not transfer accountability to the vendor. While providers are generally responsible for securing the underlying infrastructure and maintaining the AI platform, customers remain responsible for governing user access, protecting their own data, validating AI outputs, and ensuring that AI is used in accordance with regulatory requirements. Clearly defining these responsibilities helps prevent governance gaps.

Data Residency and Intellectual Property

Organizations should understand where their data is processed and stored, whether it crosses national borders, and how long it is retained. They should also clarify whether proprietary data can be used to train or improve the vendor’s AI models, and who owns any resulting models or generated insights. These considerations are increasingly important for both regulatory compliance and intellectual property protection.

Vendor Dependency

As AI becomes embedded in critical business processes, organizations can become highly dependent on a single vendor’s models, APIs, or workflows. This creates operational risk if service quality deteriorates, pricing changes unexpectedly, or the vendor experiences an outage. Evaluating exit strategies and portability should therefore form part of every AI vendor assessment.

Understanding these dimensions provides the foundation for effective third-party AI risk management. They also explain why auditors increasingly look beyond traditional security controls and ask more detailed questions about how AI is governed, monitored, and controlled throughout the vendor relationship.

Case study: When an AI vendor becomes a MAS Third-party risk

To illustrate how these risk dimensions manifest in practice, consider a typical scenario.

A Singapore-based fintech adopts an AI-powered compliance platform to accelerate its SOC 2 readiness. The platform automates the collection of evidence from cloud environments, reviews internal policies, summarizes security documentation, and generates draft compliance reports to support audit preparation.

While it may initially appear to be a standard SaaS application, the platform performs critical compliance functions and has access to regulated information. It processes security policies, employee records, cloud configurations, access logs, and other sensitive operational data. It also contributes to decisions that support regulatory reporting and audit readiness.

At this stage, the AI platform no longer functions as just another software tool – it becomes an integral part of the organization’s third-party risk landscape. Organizations must understand not only what the platform does, but also how it processes data, generates outputs, and supports business decisions. They need to know where data is stored, whether customer information trains AI models, how the platform validates AI-generated outputs, who can access sensitive information, and whether they can explain and justify AI-assisted decisions during regulatory reviews.

This scenario highlights why traditional vendor due diligence is no longer sufficient. Security certifications such as SOC 2 or ISO 27001 demonstrate that a vendor has implemented baseline security controls; however, they do not address AI-specific considerations such as transparency, governance, data usage, or human oversight. For MAS-regulated organizations, accountability ultimately rests with the financial institution – not the vendor – to demonstrate that these risks are properly understood and effectively managed.

This leads to the next critical question: What evidence will auditors expect to see?

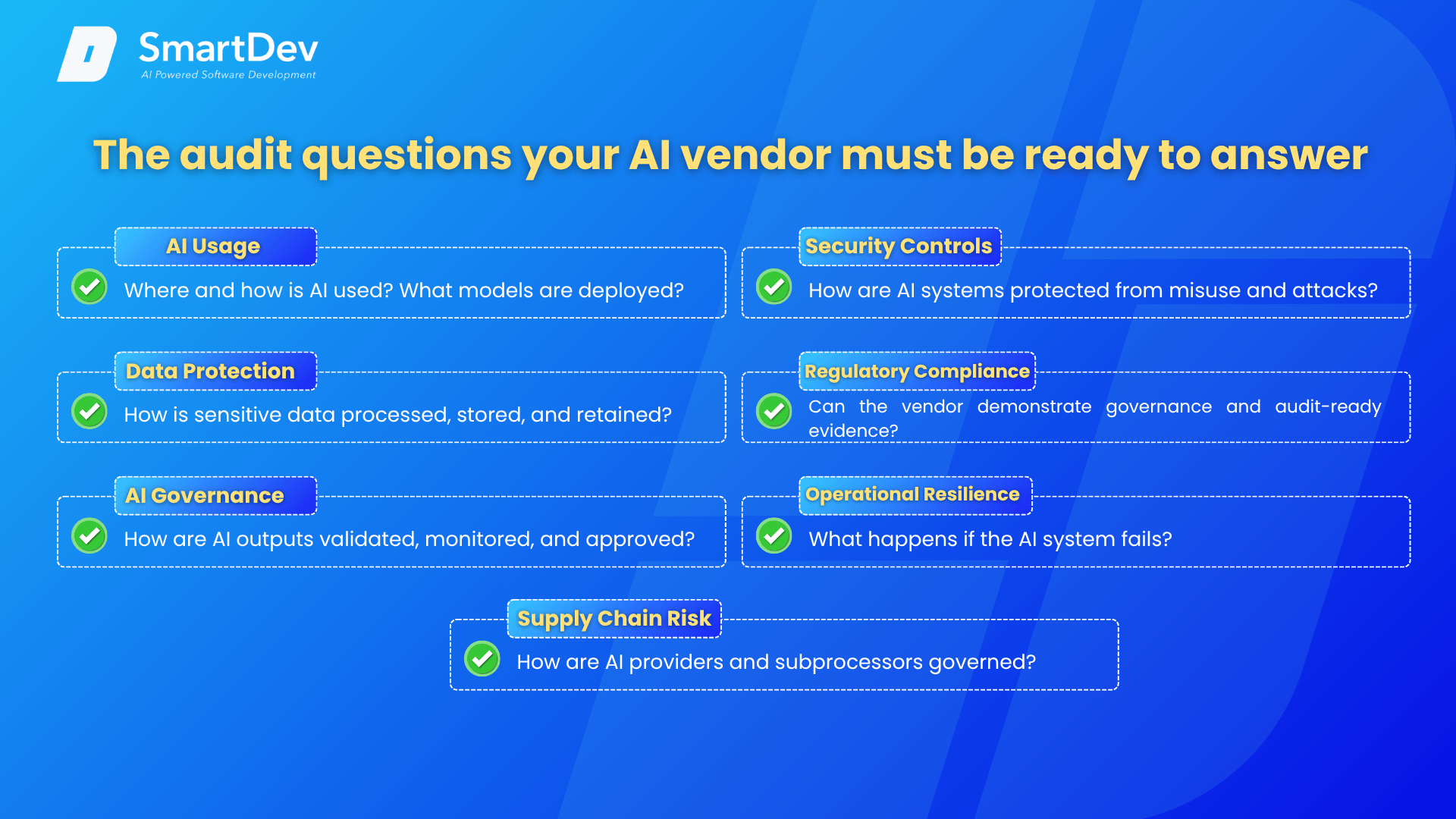

The audit questions your AI vendor must be ready to answer

Understanding the risks is only half the challenge. During audits, regulators expect organizations to demonstrate proper due diligence before deploying AI in critical business processes. Rather than asking whether AI is used, auditors increasingly focus on how organizations govern, monitor, and control AI throughout the vendor relationship.

Below are the key areas auditors are most likely to examine, along with examples of the specific questions that typically fall under each theme.

How Is AI Being Used?

Before diving into specific questions, auditors first need to understand why AI usage matters in the context of risk and compliance. The role AI plays within a vendor’s service directly influences the level of oversight required. For example, AI used in internal automation carries a very different risk profile compared to AI that makes customer-facing decisions or supports regulated processes. Without a clear understanding of how AI is embedded in the service, auditors cannot accurately assess exposure, control requirements, or potential impact on business outcomes.

Common questions in this area include:

- Does your organization use AI or machine learning to deliver any part of the service?

- Which systems or business functions rely on AI?

- What types of AI models are deployed (e.g., generative AI, predictive analytics, NLP)?

- Is AI customer-facing or used only internally?

- Are there plans to introduce new AI capabilities in the near future?

How Is Organizational Data Protected?

Data protection is a central concern because AI systems often rely on large volumes of sensitive information. Auditors need to understand how data flows through the AI lifecycle, including collection, processing, storage, and potential sharing with third parties. This is critical for ensuring compliance with privacy regulations, contractual obligations, and data residency requirements. If data handling practices are unclear or poorly controlled, organizations risk regulatory violations and loss of customer trust.

Typical questions include:

- What types of data are processed by the AI system?

- Will customer or proprietary data be used to train or improve AI models?

- Where is data stored and processed?

- Is data shared with external AI providers such as OpenAI or Anthropic?

- What retention and deletion policies are in place?

Can the AI System Be Trusted?

Auditors do not assume AI outputs are reliable. They assess whether organizations ensure accuracy, fairness, and explainability. Trust is critical in regulated environments where decisions must be defensible. Without validation and oversight, AI can create bias, errors, compliance risks, and reputational damage.

Auditors often ask:

- Can you explain how AI-generated decisions or recommendations are produced?

- How are AI models tested for accuracy, bias, and fairness before deployment?

- How is model performance monitored over time?

- What controls exist to validate AI outputs before they influence decisions?

- Are there documented processes for reviewing and approving AI outputs?

Are Security Controls Sufficient?

AI systems introduce new technical risks that extend beyond traditional cybersecurity concerns. Auditors need to understand whether appropriate safeguards are in place to protect AI systems from misuse, manipulation, or unauthorized access. This includes both standard security practices and controls specific to AI-related threats. Strong security measures demonstrate that the organization can protect sensitive data and maintain system integrity throughout the AI lifecycle.

Questions in this area may include:

- How is access to AI systems controlled (e.g., role-based access, MFA)?

- Are prompts, inputs, and outputs encrypted?

- How do you protect against AI-specific threats such as prompt injection or data poisoning?

- Is AI activity continuously monitored for anomalies or misuse?

- What logging and alerting mechanisms are in place?

Can the Vendor Demonstrate Regulatory Compliance?

As AI regulations evolve, auditors expect vendors to prove alignment with recognized frameworks. Policies alone are not enough. Vendors must show that AI systems operate transparently, traceably, and accountably. Organizations must defend their AI use during audits and regulatory reviews.

Auditors may ask:

- Do you align with frameworks such as ISO/IEC 42001, NIST AI RMF, or the EU AI Act?

- Can you provide documentation of AI governance policies and risk assessments?

- Are AI decisions logged and auditable?

- Can outputs be traced back to supporting data and logic?

- What evidence can you provide to demonstrate compliance?

What Happens If the AI System Fails?

Operational resilience is a critical component of vendor risk management. Auditors need assurance that business continuity is not compromised by reliance on AI systems. This includes understanding how failures are handled, how quickly systems can recover, and whether alternative processes exist. Without proper contingency planning, AI failures could disrupt operations or lead to incorrect outcomes with significant consequences.

Typical questions include:

- What uptime commitments or SLAs are in place for AI services?

- Are manual fallback procedures available if AI fails?

- How are incorrect AI outputs detected and corrected?

- How are incidents involving AI communicated to customers?

- What incident response processes exist for AI-related failures?

How Is Risk Managed Across the Vendor Ecosystem?

AI services often rely on third-party providers, including cloud platforms and foundation model vendors. Auditors must assess risk across the entire supply chain, not only the primary vendor. External dependencies can create new vulnerabilities, compliance challenges, and operational risks that require active management.

Auditors commonly ask:

- Which external AI providers or subprocessors support your platform?

- Have those providers undergone security and compliance assessments?

- Are sub processors contractually governed?

- What contingency plans exist if a critical provider fails or changes service?

- How do you monitor and manage risks across your AI supply chain?

Collectively, these considerations demonstrate that AI vendor governance extends far beyond traditional security reviews. Organizations must be able to show that they understand how AI is used, how risks are controlled, and how regulatory expectations can be met throughout the vendor relationship.

How AI Vendors Can Turn Compliance Scrutiny into a Trust Advantage

As AI adoption continues to accelerate – and as more organizations explore strategies for scaling AI adoption across the enterprise – regulatory scrutiny will only become more rigorous. For AI vendors, this represents more than a compliance challenge – it is an opportunity to differentiate. Vendors that can proactively demonstrate strong governance, transparency, and security will inspire greater confidence among customers, auditors, and regulators alike.

Rather than treating vendor due diligence as a hurdle to overcome, AI providers should view it as a trust-building exercise, especially as enterprises move from pilot projects to full-scale AI adoption. Customers are no longer evaluating AI vendors solely on model performance or automation capabilities. They increasingly want evidence that AI systems are secure, explainable, auditable, and designed to support regulatory obligations. Vendors that can answer these questions clearly and provide supporting documentation will reduce procurement friction, shorten security reviews, and strengthen long-term partnerships – key factors in accelerating enterprise AI adoption.

This shift also changes what it means to build enterprise-ready AI. Beyond delivering intelligent automation, vendors should be able to provide clear audit trails, transparent governance processes, robust security controls, human oversight mechanisms, and comprehensive documentation that enables customers to demonstrate compliance with confidence. These capabilities are becoming essential as organizations look to operationalize AI adoption in regulated environments.

This is the philosophy behind NORA. Rather than functioning as a standalone AI assistant, NORA is designed to help organizations automate complex compliance workflows while maintaining enterprise-grade governance. It combines AI-powered document processing with structured human oversight, producing audit-ready outputs that are traceable, explainable, and supported by evidence – making it easier for organizations to scale AI adoption responsibly.

NORA also addresses many of the questions auditors increasingly ask during third-party assessments. Organizations can demonstrate how AI-generated outputs are validated, maintain clear decision trails, manage sensitive documents within secure enterprise infrastructure, and retain the visibility required for regulatory reviews. By embedding governance directly into AI-enabled workflows, NORA enables organizations to adopt AI without compromising compliance or control, supporting a more sustainable and compliant approach to AI adoption.

The future of enterprise AI will depend on governance, not just automation. As AI vendors become part of third-party risk profiles, trust becomes a competitive advantage. Organizations navigating AI adoption must choose vendors that prioritize transparency, accountability, and governance. This will be critical to scaling AI responsibly and achieving long-term success.

Conclusion

Build an audit-ready AI vendor governance process

NORA helps compliance and risk teams turn AI-assisted workflows into traceable, reviewable, evidence-backed outputs. Instead of managing AI governance through spreadsheets and fragmented documents, teams can maintain clear review trails, structured oversight, and audit-ready evidence.