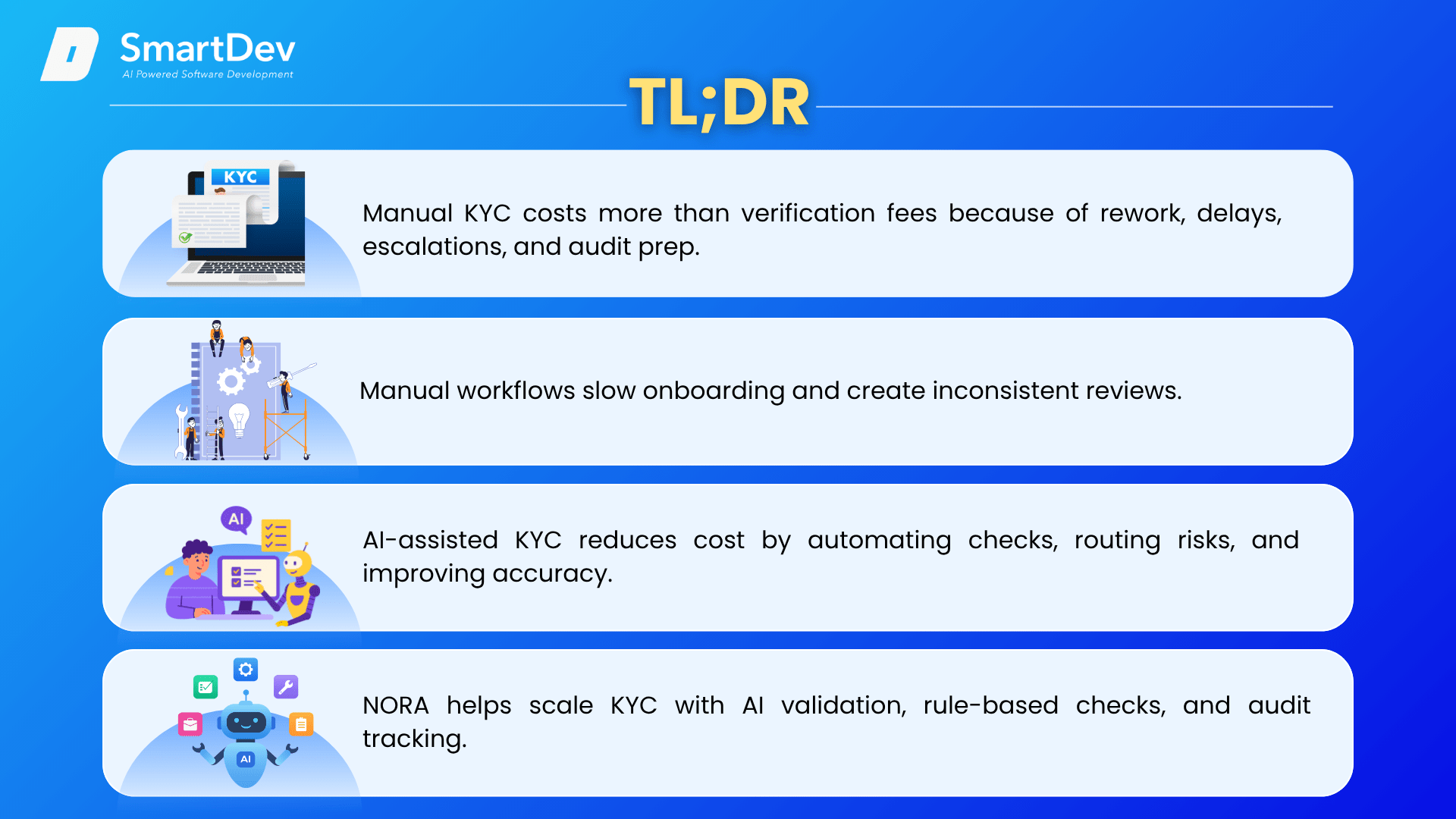

TL;DR

- Manual KYC costs more than verification fees because of rework, delays, escalations, and audit prep.

- Manual workflows slow onboarding and create inconsistent reviews.

- AI-assisted KYC reduces cost by automating checks, routing risks, and improving accuracy.

- NORA helps scale KYC with AI validation, rule-based checks, and audit tracking.

Intro: Manual KYC is more expensive than it looks

Manual KYC may seem simple – collect data, verify documents, run AML checks, and approve onboarding. In practice, it’s far more complex. Each case involves repeated reviews, data entry, exception handling, and audit tracking, where costs quickly add up.

In today’s digital-first financial world, KYC underpins secure onboarding across banking, fintech, and crypto. It helps verify identities, prevent fraud, and meet regulatory demands. According to the United Nations Office on Drugs and Crime (UNODC Global Study on Money Laundering), money laundering is estimated to account for 2 – 5% of global GDP, reaching up to $2 trillion annually.

As regulations tighten, manual KYC becomes costly – slower onboarding, heavier workloads, higher rework, and more customer drop-off. The issue isn’t KYC itself, but relying on manual processes for a system that now requires speed, accuracy, and scale. This article examines the hidden costs of manual KYC and how AI-assisted workflows can reduce friction while keeping human oversight intact.

What KYC actually involves

KYC Definition

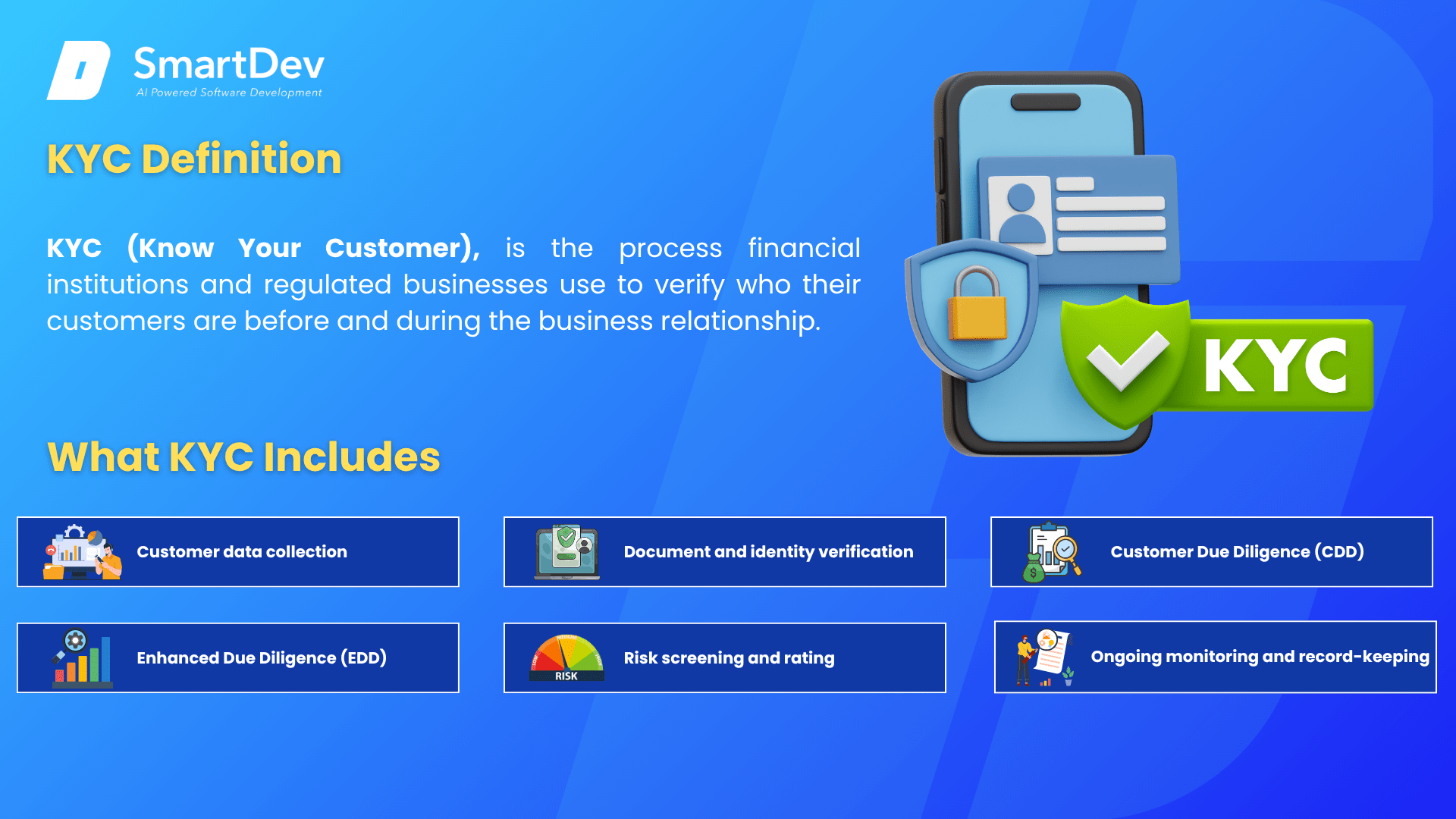

Know Your Customer, or KYC, is the process financial institutions and regulated businesses use to verify who their customers are before and during the business relationship. It is a core requirement in financial services and plays a central role in preventing fraud, money laundering, and other financial crimes.

At its core, KYC helps businesses verify that customers are who they claim to be, understand the nature of the customer relationship, and identify potential risks before allowing access to financial products or services. This includes checking identity documents, validating customer information, screening against sanctions and PEP lists, assessing money laundering or fraud risk, and keeping evidence of each decision.

Regulators around the world require KYC as part of broader Anti-Money Laundering (AML) compliance frameworks. The purpose is not only to approve legitimate customers, but also to prevent criminals, sanctioned individuals, shell entities, or high-risk actors from entering the financial system unnoticed. Strong KYC controls help businesses reduce exposure to financial crime, meet regulatory expectations, and maintain audit-ready records throughout the customer lifecycle.

What KYC Includes

KYC involves several key components that together form a comprehensive due diligence process. It begins with collecting customer data such as name, date of birth, address, nationality, company details, beneficial ownership information, and supporting documents. These documents may include passports, national IDs, proof of address, business registration certificates, or corporate ownership records. The information is then checked for accuracy, consistency, and authenticity.

The process also includes identity verification, where businesses validate documents and confirm customer identities through manual or automated checks. Customer due diligence (CDD) follows, helping businesses assess the nature of the relationship and determine each customer’s risk level. For higher-risk individuals or entities, businesses may apply enhanced due diligence (EDD) to investigate background, source of funds, ownership structure, and business activities in greater detail.

In addition, KYC requires screening customers against sanctions lists, politically exposed person (PEP) databases, adverse media sources, and other risk indicators. Based on these checks, customers are assigned risk levels, which determine the level of scrutiny and monitoring required. Ongoing monitoring is another critical component, as businesses must continuously review customer activity to detect unusual or suspicious behavior, update customer information when necessary, and ensure that risk profiles remain accurate over time. Record-keeping is equally essential, requiring institutions to maintain detailed documentation of all KYC checks, decisions, and updates for regulatory audits and internal accountability.

Over time, KYC has evolved from a largely manual compliance requirement into a more digital and data-driven process. Advances in automation, data integration, and verification technologies have made it possible to streamline many of these steps, reduce human error, and improve efficiency. However, despite these technological improvements, the core purpose of KYC remains unchanged: enabling businesses to confidently verify customer identities, assess and manage risk, and maintain compliance throughout the entire lifecycle of the customer relationship.

How Manual KYC Works in Operations

Manual KYC verification relies heavily on human reviewers to validate customer identities, assess submitted documents, and decide whether a customer can be approved. While the process may appear straightforward at a high level, it often becomes slow and inconsistent in real operations because each case depends on reviewer judgment, internal procedures, and multiple handoffs between teams.

The process typically begins when customers submit personal information along with identity documents such as passports, national IDs, driver’s licenses, proof of address, or corporate records for business accounts. Compliance teams then review these submissions to confirm that customers have provided complete, legible, and valid information.

After customers submit the documents, analysts compare the customer-provided details with the documents, checking names, dates of birth, addresses, document numbers, expiry dates, and visible security features. They also follow internal guidelines to assess authenticity and determine whether the information aligns with the customer profile.

Issues often appear when information is unclear, inconsistent, or incomplete. Blurry images, expired IDs, mismatched details, or missing documents can trigger additional follow-ups, requiring teams to contact customers, request updated information, and reopen the case once new documents arrive. This extends the review cycle and increases pressure on compliance teams.

Manual KYC also introduces variation in decision-making. Similar cases may be handled differently depending on the reviewer’s experience, interpretation of internal rules, or level of risk sensitivity. This makes it harder for organizations to maintain consistent compliance standards across teams, locations, or shifts.

The process ends with approval, rejection, or escalation. Low-risk cases may move forward quickly, while unclear or high-risk cases are sent to senior compliance staff for further review. Teams must also record decisions, store evidence, and maintain an audit trail, which becomes harder when information is spread across emails, folders, spreadsheets, and internal systems.

The challenge is not that compliance teams lack expertise. The challenge is that traditional KYC processes place too much operational responsibility on people, making the process harder to scale as onboarding volume grows.

The Real Cost of KYC Compliance

Direct Verification Costs in KYC

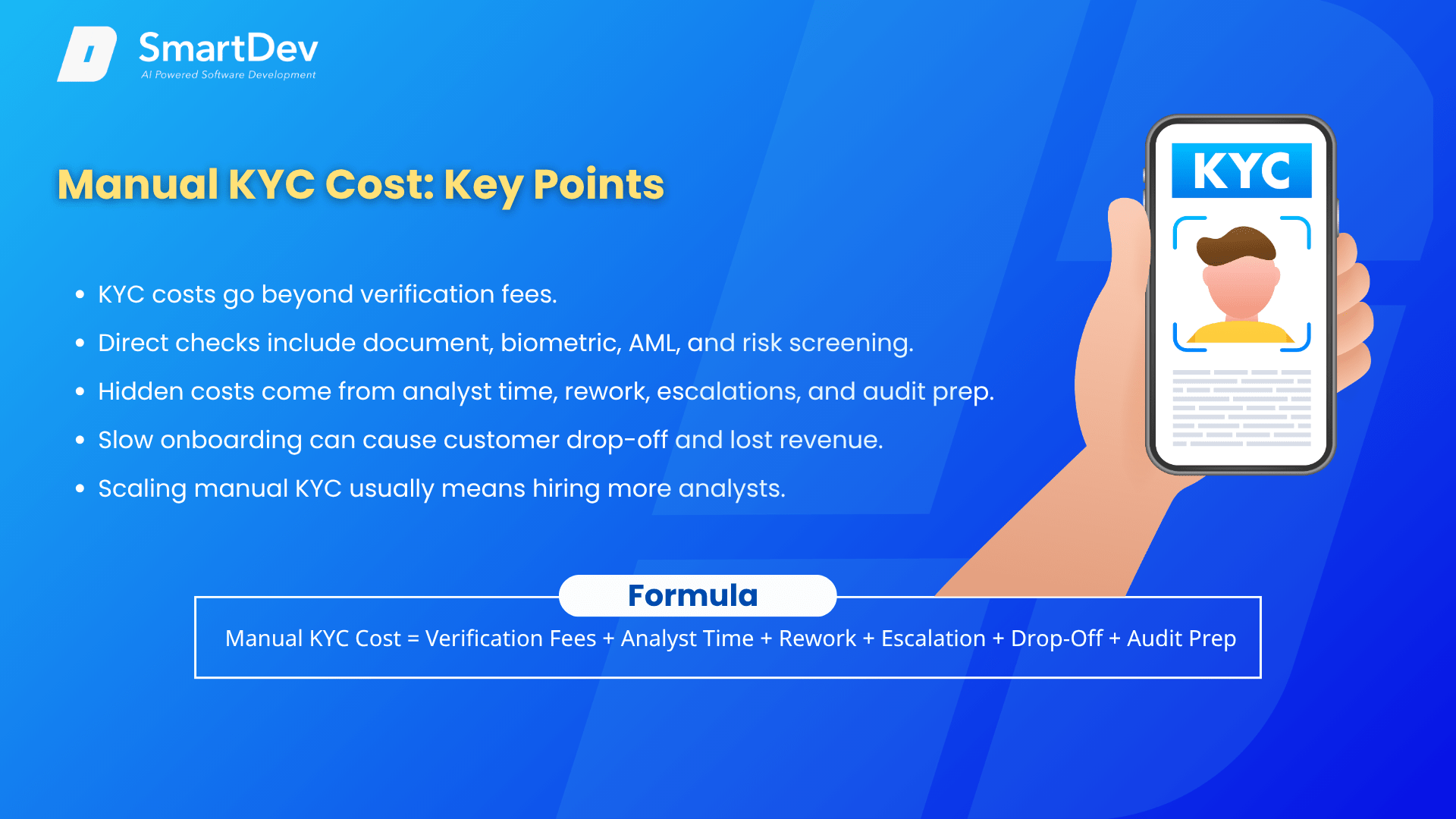

Understanding the cost of KYC compliance starts with understanding what each verification actually requires. A complete KYC process is not a single check. It often includes document verification, biometric matching, AML screening, risk scoring, manual review, exception handling, and record-keeping. Each step adds cost, especially when businesses process high onboarding volumes or rely heavily on manual operations.

Document verification is one of the most common cost drivers. It involves checking whether an identity document is authentic, extracting key data, validating document details, and cross-referencing information against other sources. This may include passports, national IDs, driver’s licenses, tax documents, employment records, proof of address, or corporate documents. Market pricing for ID document verification can vary widely depending on document type, geography, provider, and volume, but public pricing examples often place these checks in the range of around $0.10 to $1.50 per verification.

Biometric checks add another layer of cost. In many digital KYC workflows, customers are asked to submit a selfie or live video so facial recognition software can compare the person with the image on the submitted identity document. These checks help detect impersonation, spoofing, and stolen document use. Depending on the level of verification required, biometric liveness and face match checks may cost from a few cents to a few dollars per session, with lower rates usually available for higher-volume use cases.

These direct verification fees are easy to identify, but they only show one part of the total KYC cost. A business may pay separately for document checks, biometric verification, AML screening, database checks, and risk scoring. Once these costs are multiplied across thousands of onboarding cases, even small per-check fees can become a significant recurring expense.

More importantly, verification fees do not capture the operational cost around the process. If a document fails validation, if customer details do not match, or if a biometric check produces a low-confidence result, the case often moves into manual review. That means additional analyst time, customer follow-up, escalation, and audit documentation. In practice, the real cost of KYC is not only what businesses pay per check. It is also the time and labor required to resolve everything that happens after the check.

Hidden Operational Costs of Manual KYC

Beyond direct verification fees, KYC compliance involves operational costs that are often harder to measure but more damaging over time. These include analyst time, data entry, customer follow-ups, escalations, audit preparation, and delays in onboarding. While per-check pricing is easy to calculate, the work required to resolve exceptions usually has a much larger impact on the total cost per approved customer.

Analyst time is usually the most visible cost. Teams spend hours reviewing documents, checking customer details, running screenings, communicating with customers, and preparing cases for approval. However, this visible labor cost is only one part of the equation.

The larger cost appears when cases cannot be completed the first time. Incomplete submissions, mismatched names, expired documents, missing ownership records, unclear customer information, or failed biometric checks often require additional review. Each unresolved issue adds more communication, more waiting time, and more validation work before the case can move forward.

Escalations also increase cost. High-risk or ambiguous cases often require senior compliance review, especially when enhanced due diligence is needed. If these cases are not routed clearly, they can sit unresolved across inboxes, shared folders, spreadsheets, or internal tools, slowing down decision-making and increasing workload for both junior and senior reviewers.

| A simple way to understand the full cost structure is: |

| Manual KYC Cost = Verification Fees + Analyst Time + Exception Handling + Escalation + Customer Drop-Off + Audit Preparation |

This formula shows why focusing only on verification fees can be misleading. The true cost often comes from what happens after a check fails, when teams must investigate, communicate, document, and decide what to do next.

The impact also extends beyond compliance operations. Slow onboarding can lead customers to abandon the process before verification is complete. For banks, fintechs, crypto platforms, and other regulated businesses, this means KYC delays can reduce conversion rates, postpone revenue, and weaken the customer experience from the first interaction.

Audit preparation adds another layer of cost. If documents, approvals, screening results, and review notes are stored across disconnected systems, compliance teams must spend extra time reconstructing case history during audits. Instead of focusing on current risk, they are forced to piece together evidence after the fact.

Finally, manual KYC creates a scaling problem. As customer volume grows, businesses often need more analysts to handle more cases, follow-ups, escalations, and documentation. This makes growth expensive because operational capacity increases mainly through headcount rather than process efficiency.

How NORA can help KYC process to improve its efficiency

AI-assisted workflow automation helps reduce these costs by taking over the repeatable parts of KYC validation. It can extract document data, check completeness, detect inconsistencies, classify case status, route exceptions, and maintain audit records while keeping compliance professionals responsible for final decisions. This is where NORA supports KYC operations: by making validation more structured, consistent, and cost-efficient without removing human oversight.

AI Impact on KYC

AI improves KYC by reducing both the time and cost required to complete each validation case. Instead of requiring analysts to manually review every document from the beginning, AI can extract key information from customer IDs, proof of address, business registration documents, ownership records, and other supporting files. This reduces manual data entry, lowers the risk of human error, and allows analysts to spend less time on basic field checking.

AI also helps reduce rework, one of the biggest hidden costs in manual KYC. It can detect missing information, expired documents, inconsistent names, unclear images, mismatched customer details, or incomplete records before the case reaches final review. By identifying these issues earlier, teams avoid repeated review cycles, unnecessary customer follow-ups, and duplicated analyst effort.

Another major impact is faster and more cost-effective risk triage. AI can help classify customers based on document quality, risk indicators, screening results, and internal business rules. Teams can move low-risk cases through the workflow faster, while NORA routes high-risk or unclear cases to the right compliance reviewer. This reduces bottlenecks, prevents senior teams from being overloaded with routine cases, and helps organizations use compliance expertise where it creates the most value.

AI also improves consistency across the KYC process. In manual workflows, similar cases may be assessed differently depending on the reviewer, team, location, or shift. AI-assisted workflows apply standardized checks and rules across cases, reducing decision variation and improving validation quality at scale. This consistency helps lower compliance risk and reduces the cost of correcting errors later.

Audit readiness is another area where AI creates financial value. When every action, document update, exception, escalation, and approval is logged automatically, compliance teams spend less time preparing audit evidence manually. Instead of searching across emails, spreadsheets, shared folders, and disconnected systems, teams can access a clearer record of what happened, who reviewed it, and why a decision was made.

The strongest use of AI in KYC is not full automation. It is human-in-the-loop automation. AI handles repetitive checks, workflow coordination, and early validation, while compliance professionals remain responsible for judgment, approvals, and high-risk decisions. This model improves efficiency while helping control cost, risk, and operational complexity.

NORA Application in the KYC Process

NORA streamlines the most cost-intensive parts of KYC validation, including document processing, rule validation, exception management, review routing, and audit tracking. Rather than replacing existing systems, it works as an intelligent layer on top of CRM platforms, onboarding portals, or internal workflows.

Once documents are submitted, NORA preprocesses them by extracting, cleaning, and structuring data, often using OCR for scanned files. This prepares the information for faster validation and reduces the time teams spend reading documents, copying details, and checking basic fields.

NORA’s validation process combines AI analysis with rule-based compliance checks. The AI engine reviews document completeness and identifies potential issues, while the rule engine applies regulatory and internal requirements in a standardized way. This improves accuracy and reduces inconsistent validation outcomes.

After processing, NORA classifies documents as valid, invalid, or requiring review. It highlights specific issues so administrators can focus directly on the parts that need attention. NORA automatically routes low-confidence, incomplete, or high-risk cases to human reviewers, ensuring oversight while preventing routine cases from consuming unnecessary analyst time.

Overall, NORA helps businesses reduce KYC cost by shortening review cycles, improving first-time validation quality, reducing unnecessary escalations, strengthening audit readiness, and enabling teams to process higher volumes without increasing headcount at the same pace.

By standardizing validation logic and automating repeatable work, NORA allows compliance teams to focus on risk assessment, exception handling, and regulatory decision-making. The result is a faster, more scalable, and more cost-efficient KYC operation.

Manual KYC vs AI-Assisted KYC

We can handle KYC verification in several ways, from traditional manual review to AI-driven verification and API-based identity checks. Each method plays a role in preventing fraud and supporting compliance, but the difference lies in speed, scalability, accuracy, and operational cost.

Traditional KYC relies on human reviewers to collect documents, inspect identity information, validate authenticity, and make approval decisions based on internal guidelines. This approach gives compliance teams direct control over the process, but it is also time-consuming and vulnerable to human error. As onboarding volumes grow, manual review often creates bottlenecks, inconsistent decisions, and higher operational costs.

AI-assisted KYC changes the workflow by using technologies such as machine learning, biometric recognition, automated document extraction, and risk-based analysis. Instead of requiring analysts to manually review every detail from the start, AI can extract information, compare customer data, detect inconsistencies, support facial matching, flag suspicious patterns, and prioritize cases based on risk. This reduces repetitive manual work while helping teams make faster and more consistent decisions.

KYC API verification adds another layer by integrating automated checks directly into existing platforms and onboarding systems. APIs can support real-time identity verification, cross-reference customer data across multiple sources, and scale efficiently when transaction or onboarding volumes increase. For businesses handling large numbers of customers, this makes KYC faster, more connected, and easier to manage within the broader compliance workflow.

However, the strongest KYC model is not purely manual or fully automated. The most effective approach combines traditional compliance oversight, AI-powered verification, and API-based integration. AI and APIs handle repetitive checks, data extraction, biometric comparison, and risk signals, while human reviewers remain responsible for judgment, exception handling, and high-risk decisions.

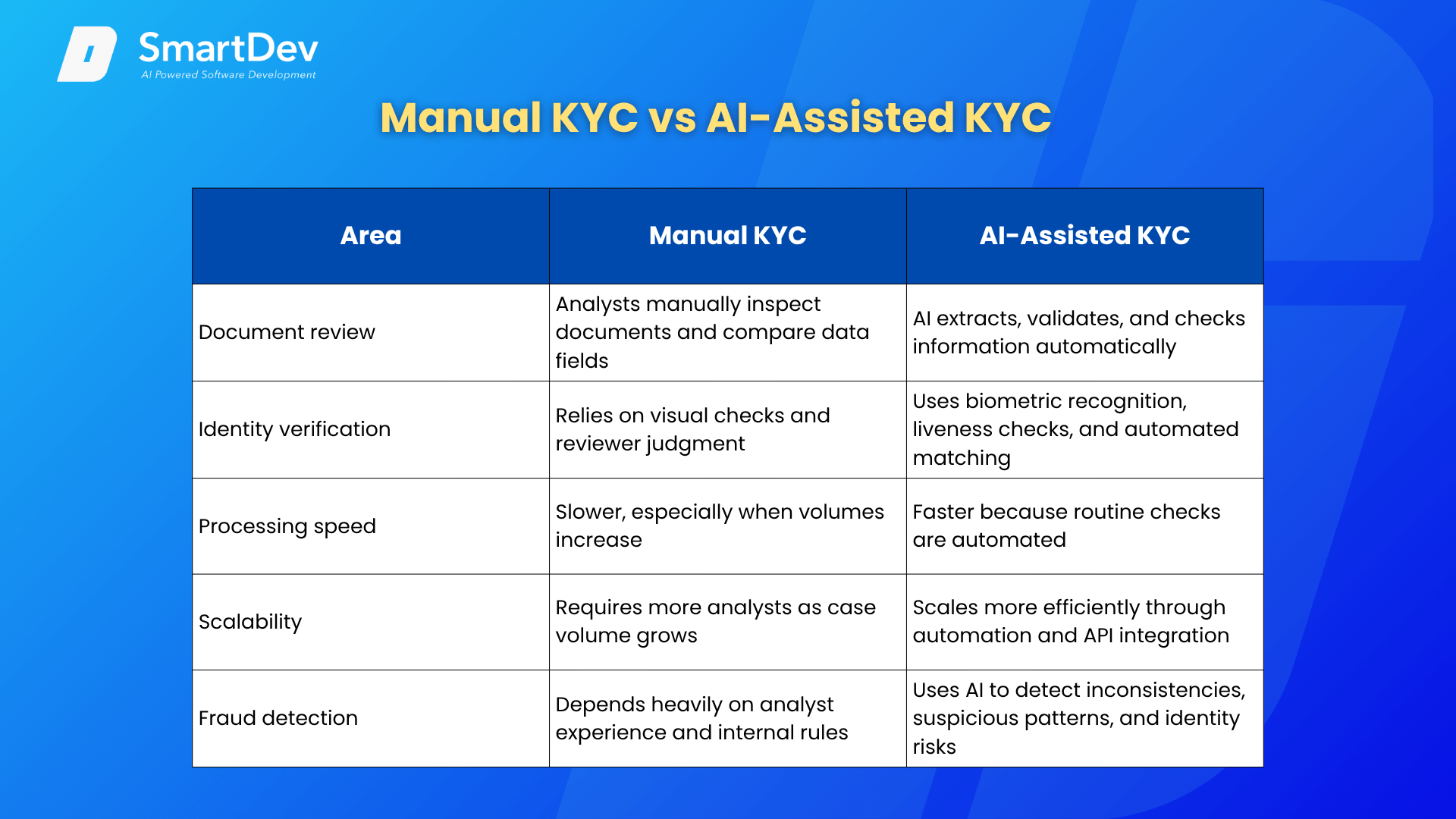

| Area | Manual KYC | AI-Assisted KYC |

| Document review | Analysts manually inspect documents and compare data fields | AI extracts, validates, and checks information automatically |

| Identity verification | Relies on visual checks and reviewer judgment | Uses biometric recognition, liveness checks, and automated matching |

| Processing speed | Slower, especially when volumes increase | Faster because routine checks are automated |

| Scalability | Requires more analysts as case volume grows | Scales more efficiently through automation and API integration |

| Fraud detection | Depends heavily on analyst experience and internal rules | Uses AI to detect inconsistencies, suspicious patterns, and identity risks |

The real value of AI-assisted KYC is not replacing compliance teams. It is helping them focus on the cases that actually require human judgment. Low-risk and routine checks can move faster, while complex or suspicious cases receive more attention from experienced reviewers. This creates a better balance between compliance control, customer experience, and operational efficiency.

Conclusion

Manual KYC may seem manageable at low volumes, but costs rise quickly as onboarding scales. Beyond verification fees, the real burden comes from analyst time, repeated reviews, delays, customer drop-off, and the need to grow teams.

For regulated businesses, this directly impacts onboarding speed, compliance quality, and revenue generation. The issue isn’t KYC itself, but relying on manual workflows that are not designed to scale efficiently.

AI-assisted KYC helps reduce these costs by automating repetitive tasks and minimizing human error. It also improves consistency and gives teams better visibility, while still allowing human oversight where it matters most.

NORA brings this into a structured workflow with document extraction, AI analysis, validation rules, and audit tracking. This enables businesses to scale compliance operations more efficiently without compromising control or accuracy.

See how NORA can help your team reduce manual KYC workload, route exceptions faster, and maintain a clearer audit trail